CIBIL Score Explained: What It Is, How It Is Calculated, and How to Improve It

Learn how Credit Information Bureau (India) Limited scores impact your loans. Discover how CIBIL is calculated, why it matters, and tips to improve your credit.

Arjun Sharma

Content Lead – Banking & Payments

14 min read

Table of Contents

- What Is a CIBIL Score?

- Why Your CIBIL Score Is Important

- What Is Considered a Good CIBIL Score?

- How to Check Your CIBIL Score for Free?

- How Is Your CIBIL Score Calculated?

- How CIBIL Score Affects Interest Rate

- Common Mistakes That Can Lower Your CIBIL Score

- Practical Ways to Improve Your CIBIL Score

- How Long Does It Take to Improve Your CIBIL Score?

- Conclusion

- FAQs

If you have ever applied for a loan or a credit card, you have likely heard of the CIBIL score. It is one of the most important factors lenders use to determine your eligibility for home loans, personal loans, or even a simple credit card application.

But what exactly is a CIBIL score? Managed by the Credit Information Bureau (India) Limited (CIBIL), this score represents your entire credit history. It shows how responsible you have been with your debt repayments. This blog discusses everything you need to know about CIBIL scores, why they matter, how they are calculated, and how to improve them for better loan prospects.

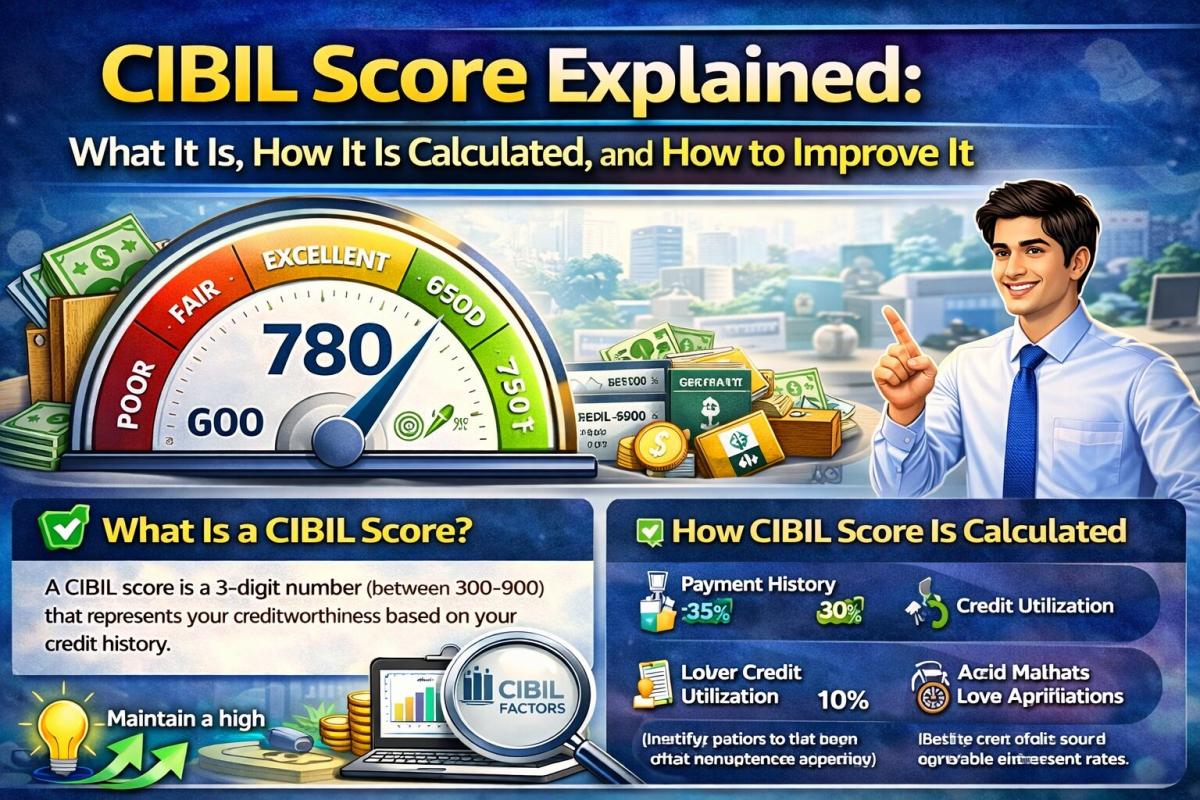

What Is a CIBIL Score?

Before learning how to improve your CIBIL score, it is important to understand what it really represents. Once you know what your CIBIL score is and how it works, you will be able to understand a lot about your financial decisions and requirements.

A CIBIL score is a three-digit number ranging from 300 to 900. This score indicates how trustworthy you are when it comes to repaying borrowed money. A high score indicates a high creditworthiness.

A CIBIL score is assigned to you based on the data collected by TransUnion CIBIL, which is one of the top credit bureaus in the world. The credit bureau gathers financial data from banks, lenders, and financial organisations about your credit behaviour.

- A high CIBIL score indicates that you are very good at repaying your loans.

- A low CIBIL score reflects that you are not good with borrowing and are not responsible towards credit and repayments.

Each time you apply for a loan, your credit behaviour is reported to the credit bureau. On the basis of the data collected, the credit bureau calculates your CIBIL score and prepares your credit report.

Why Your CIBIL Score Is Important

Your CIBIL score plays a very important role in your financial life. It is the first thing lenders check when you apply for loans. It helps lenders understand how responsible you are with your money.

A high CIBIL score makes borrowing money easier for you. On the other hand, a low CIBIL score makes borrowing money difficult for you.

Here are some reasons why your CIBIL score is so important:

Faster Loan Approvals

One of the main benefits of a good CIBIL score is faster loan approval. This is because lenders prefer people who have a good track record of paying their debts on time.

When your CIBIL score is good, the bank will consider you a reliable borrower. This means the bank will process your loans much more quickly and easily, since it knows you will not default on payments.

In fact, in some cases, people with good CIBIL scores may even be offered pre-approved loans by the bank.

Lower Interest Rates

Your CIBIL score may not only affect whether or not you get a loan; it may also affect the interest rate that you have to pay.

If your CIBIL score is high, then you will be considered a low-risk borrower. This means that banks and financial institutions will offer you lower interest rates.

In fact, a lower interest rate can help you save a lot of money in the long run, especially in the case of large loans like a home or car loan.

Better Credit Cards

Most people do not know that their CIBIL score also affects the credit cards they're eligible for. Banks consider your credit score before approving your credit card. A high CIBIL score may help you get better credit cards that offer benefits like rewards points, travel benefits, and cashback.

If your CIBIL score is low, you may not qualify for credit cards or may get rejected.

Higher Loan Amounts

Another advantage of having a high CIBIL score is that you can qualify for much larger loan amounts.

Lenders are more comfortable providing higher loans to people with high CIBIL scores, as they have demonstrated good financial behaviour in the past.

If two people are applying for the same loan but have different CIBIL scores, the person with the higher CIBIL score will qualify for a higher loan amount.

Easier Approval for Future Credit

A good CIBIL score also helps get easier approval for future credit. Since lenders are aware of your good repayment behaviour, they may easily approve loans. This may help with urgent loan needs for important events in your life.

What Is Considered a Good CIBIL Score?

Not all CIBIL scores are considered good by lenders. There are some ranges that are considered excellent, and some ranges are considered poor.

These ranges are as follows:

750-900: Excellent

A CIBIL score within this range is considered excellent. Borrowers with such high CIBIL scores are approved for loans easily and also receive lower interest rates.

700-749: Good

A CIBIL score in this range is considered good and is acceptable to all lenders.

650-699: Fair

A CIBIL score within this range may qualify you for loans, but you won't get lower interest rates or a higher loan amount.

300-649: Low

If your CIBIL score falls in this range, you won't get approved for loans, and even if you get approved, you'll have to pay a much higher interest rate than normal. If your CIBIL score falls within this range, take steps to improve it, then apply for loans.

How to Check Your CIBIL Score for Free?

You can check your CIBIL score for free. As per the guidelines of the Reserve Bank of India, every individual can get one free credit report every year from all four credit bureaus in India.

These four credit bureaus are:

- TransUnion CIBIL

- Experian

- Equifax

- CRIF High Mark

Steps to check your CIBIL score online:

- Go to the official website of TransUnion CIBIL

- Click on “Get Free CIBIL Score”

- Enter your basic details (name, mobile number, PAN, etc.)

- Verify your identity using OTP

- Your CIBIL score and report will be shown on the screen

How Is Your CIBIL Score Calculated?

Your CIBIL score is calculated based on a lot of factors:

1. Payment History

The most important factor that determines a person's credit score is their payment history. It includes whether a person pays their loan Equated Monthly Instalments (EMIs) and credit card bills on time. If a person has a poor payment history, their credit score may fall significantly.

2. Credit Utilisation

Credit utilisation refers to the percentage of a person's credit limit that is being used. Using a large portion of their credit limit can adversely affect their credit score. Ideally, you should keep your credit utilisation below 30% to increase your CIBIL score.

3. Length of Credit History

A longer credit history is considered good for a person's credit score.

4. Credit Mix

Having a good credit mix of secured and unsecured credit can also positively affect a person's credit score. For example, having a home loan and a credit card can reflect a good credit score.

5. Credit Enquiries

Every time a person applies for a new credit card or loan, their credit score is checked. If a person has a large number of credit enquiries in a short period, it can negatively affect their credit score.

How CIBIL Score Affects Interest Rate

Here is a simple way to understand this with an example. Suppose two people apply for a ₹30 lakh home loan for 20 years. Person A has a CIBIL score of 750, while Person B has a score of 620. Because of the better score, Person A may get a lower interest rate of around 8.5%, while Person B may get a higher rate of around 10.5%. Due to this difference, Person A’s EMI will be around ₹26,000, while Person B will have to pay about ₹30,000 every month. This means Person B pays ₹4,000 more every month. Over 20 years, this adds up to lakhs of extra money paid as interest. You can use an EMI calculator to understand your monthly payment better.

Common Mistakes That Can Lower Your CIBIL Score

Sometimes, people unknowingly damage their credit score due to certain financial habits. Understanding these mistakes can help you avoid making them and hence protect your credit profile. Here are some of the most common mistakes:

1. Missing or Delaying Payments

Missing out on credit card payments or EMIs on a loan is one of the common mistakes that can bring down a person's CIBIL score.

Payment history is an important factor in deciding a person's credit score. A missed payment can affect a person's credit score, especially if it is a credit card payment.

If payments are missed frequently, it can result in a greater reduction in CIBIL scores. Therefore, it is always advisable to pay your bills before the due date.

2. Using Too Much of Your Credit Limit

High credit utilisation can reduce your credit score by quite a lot.

For example, if you have a credit card with a credit limit of ₹1,00,000, and you spend ₹90,000 on a regular basis, it is an indicator that you are heavily depending on credit, and your credit score will decrease.

Excessive use of credit can lead to a reduction in CIBIL scores, irrespective of timely payment of bills. Experts recommend that you use less than 30% of the available credit limit for a healthy CIBIL score.

3. Closing Old Credit Cards Too Quickly

A lot of borrowers think that closing unused credit cards can increase their CIBIL score. However, this is not true. Older credit cards also play a part in the length of your credit history. When closing them, your credit history may be shortened.

As the length of credit history is one of the factors that determine your CIBIL score, closing such accounts may result in a lower CIBIL score.

4. Settling Loans Instead of Repaying Them Fully

A lot of people go for loan settlements when they're not in a position to repay their loans. While this may provide you with temporary relief, your CIBIL score will take a massive hit.

When you settle your loan, your credit report shows "settled" instead of "closed," indicating that you were not able to repay your loan fully. This will reduce your credit report and will stay on your report for a long time, making lenders cautious while providing you with further loans.

5. Applying for Too Many Loans

Every time you apply for a loan or credit card, your credit report is checked by the bank or financial institution. These credit checks are called credit enquiries.

If you apply for many loans or credit cards, your credit enquiries increase, which may affect your CIBIL score. This is because your credit report shows that you're urgently in need of credit, which is not a good sign.

6. Ignoring Errors in Your Credit Report

Your CIBIL score may also suffer if there are incorrect details in your credit report. For example, you might have closed a loan, but your loan might show on your report as still active. Or, your report may show delayed payments, even if you made the payments on time.

If you do not correct these errors, your CIBIL score may suffer. Therefore, you have to take care of your credit report.

Practical Ways to Improve Your CIBIL Score

Now that you know how your CIBIL score is calculated and the mistakes that reduce your CIBIL score, you should also know about how you can improve it. Even if the process of improving your CIBIL score is simple, it will take time. Here are some practical ways to improve your CIBIL score:

1. Pay All Bills on Time

One of the best ways of improving your CIBIL score is by paying your EMI as well as credit card bills on time. Payment history plays a very important role in your CIBIL score calculation. If you are unable to remember the payment date, you can set reminders or set up auto-debit so that you never miss the payment.

2. Reduce Credit Card Balances

Your credit utilisation ratio plays a very important role in your CIBIL score. So, if your credit utilisation is more than 30%, reduce it. If you are unable to reduce the credit card balance entirely, you can try paying a part of the outstanding amount.

3. Keep Older Credit Accounts Active

The longer your credit history, the better your CIBIL score. So, if you have credit cards that you have had for a very long time, you may want to use these credit cards from time to time to improve your CIBIL score.

4. Avoid Frequent Credit Applications

Every time you apply for a loan or a credit card, lenders do a hard inquiry on your CIBIL score. Multiple hard inquiries within a short period of time will reduce your CIBIL score. So, don't apply for too many loans in a short period.

How Long Does It Take to Improve Your CIBIL Score?

Improving your CIBIL score is not instant. It takes time and discipline.

Here’s a realistic timeline:

- Within 1-3 months: Small improvement if you start paying bills on time.

- Within 6 months: Noticeable improvement if you reduce credit card usage and avoid missed payments.

- Within 12-18 months: Big improvement. Your score can move from low to good if you follow all rules.

- More than 18 months: You can reach an excellent score if you maintain good financial habits consistently.

Conclusion

Your CIBIL score is the most important parameter determining your loan and credit eligibility. Lenders always check your CIBIL score before approving you for credit cards or loans. Hence, you should make sure that your CIBIL score is high.

Always pay your EMIs and credit card dues on or before the due date, keep credit utilisation below 30%, and don't apply for multiple loans in a short period of time. Even if you have a poor CIBIL score, you can increase it. However, that will take time, and you'll have to be financially disciplined.

FAQs

1. Does checking my own CIBIL score reduce it?

No, checking your own CIBIL score is considered a soft enquiry and does not affect your score in any way.

2. Can someone have a CIBIL score without taking a loan or credit card?

No, you usually need some form of credit history, such as a loan or credit card, for a CIBIL score to be generated.

3. Can a guarantor's loan affect my CIBIL score?

Yes, if you act as a guarantor and the borrower fails to repay the loan, it can negatively impact your CIBIL score.

4. Does closing a loan improve my CIBIL score?

Closing a loan after making all payments on time can positively contribute to your CIBIL score over time.

5. How often does the CIBIL score get updated?

Your CIBIL score usually gets updated every month when lenders report your latest credit activity to the credit bureau.

6. Can using multiple credit cards affect my CIBIL score?

Having multiple credit cards does not harm your CIBIL score as long as you manage them responsibly and pay the bills on time.

7. What is the minimum CIBIL score required for a home loan?

Most banks prefer a CIBIL score of at least 700 or above for a home loan. However, for the best interest rates, a score of 750+ is ideal.

8. How long does a loan default stay on my CIBIL report?

A loan default can stay on your CIBIL report for up to 7 years. During this time, it can make it difficult to get loans or credit cards.

Disclaimer

This article is for informational purposes only and does not constitute financial advice. Please consult a qualified financial advisor for personalised guidance.

Related Blogs

Published on May 18, 2025

Tips on How to Calculate Monthly EMI for Any Loan

Struggling to understand your EMI amount? This blog covers all the necessary tips on how to calculate your monthly EMI to help you stay ahead of your finances.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 25, 2025

Monthly EMI Calculators: A Detailed Overview

Monthly EMI calculators allow you to get a pre-hand idea of the EMI you must pay monthly. In return, an EMI calculator per month helps manage monthly finances better.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2025

Buying a Car? Here's How to Use a Vehicle EMI Calculator the Smart Way

Plan your car or bike loan with ease. Learn how to use a vehicle EMI calculator, input values correctly, and get accurate monthly EMI instantly.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Feb 17, 2025

Master EMI Calculators: How to Estimate Your Monthly Payments with Ease

Learn how EMI calculators work to estimate monthly payments accurately. Explore EMI formulas, examples, and factors to make smart financial decisions.

Arjun Sharma

Content Lead – Banking & Payments

Published on Feb 10, 2025

Ultimate EMI Calculator Guide for India: Understand EMIs for Home, Car & Personal Loans

Use our EMI calculator guide to estimate your monthly loan payments for home, car, or personal loans in India. Plan better with accurate, fast results.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ