Bank Server Downtime: Impact on Your Online Transactions

Learn how bank server downtime affects online transactions, failed payments, customer trust, cybersecurity, and banking resilience in 2026.

Table of Contents

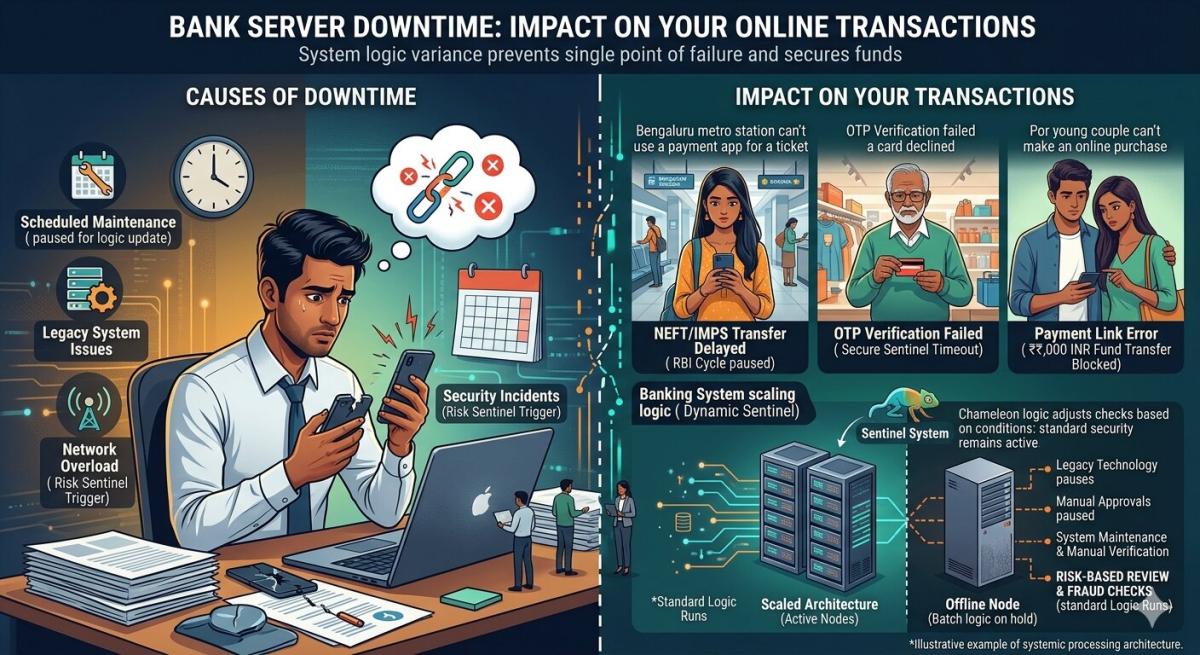

Imagine standing at the checkout, card in hand, only to be told the transaction can’t go through because “the bank’s servers are down.” It’s a scenario many of us have faced, a momentary annoyance that quickly escalates into real frustration. This immediate, palpable bank server downtime impact on online transactions is just the tip of the iceberg. As someone who’s navigated the digital financial landscape for years, I’ve seen firsthand how these outages ripple far beyond a single failed payment, affecting businesses, individual consumers, and the very trust underpinning our digital economy. The complexity of modern banking infrastructure means even brief disruptions can have significant, far-reaching consequences that demand our attention and understanding.

Immediate Financial Losses for Businesses

When bank servers falter, businesses face an immediate and quantifiable hit to their revenue. Every minute of downtime translates directly into lost sales, failed transactions, and frustrated customers abandoning their carts. E-commerce platforms, reliant on seamless payment processing, are particularly vulnerable. A major outage during peak shopping hours, like a holiday sale, can wipe out millions in potential income, a setback that small and medium-sized enterprises might struggle to recover from. This isn’t just about the money lost during the actual downtime; it includes the opportunity cost of customers who simply won’t return.

Beyond sales, operational costs can also surge. Businesses might incur charges for failed transactions or be forced to implement manual processing workarounds, which are both inefficient and prone to error. The ripple effect can extend to inventory management, logistics, and even employee productivity as staff are diverted to deal with the fallout. For many companies, especially those with tight margins, repeated or prolonged bank server issues can threaten their very solvency, making proactive mitigation strategies absolutely essential for financial stability.

Eroding Customer Trust and Loyalty

Nothing sours a customer experience faster than a failed payment or an inaccessible account. When individuals can’t complete transactions, check balances, or pay bills due to bank server downtime, their trust in their financial institution erodes rapidly. This isn’t just an inconvenience; it can create genuine anxiety, especially if the outage occurs during a critical financial moment. Customers expect reliability and seamless access in today’s digital age, and any deviation from this standard can lead them to seek alternatives, damaging brand loyalty and increasing churn rates.

The impact on reputation can be long-lasting and difficult to repair. Social media amplifies customer frustration, turning isolated incidents into public relations crises. Negative sentiment spreads quickly, influencing potential new customers and making it harder for banks to attract and retain users. Building trust takes years, but a single, poorly handled outage can shatter it in moments. Banks must not only work diligently to prevent downtime but also communicate transparently and effectively when it does occur to minimize reputational damage.

Operational and Regulatory Headaches

Bank server downtime isn’t just a customer-facing issue; it creates significant internal operational challenges. IT teams are plunged into crisis mode, working under immense pressure to identify and resolve the root cause, often around the clock. This diverts critical resources from other strategic projects and can lead to burnout. Furthermore, the post-mortem analysis required to understand the failure and implement preventative measures is a time-consuming and complex process, pulling staff away from their regular duties and impacting overall productivity across departments.

Compliance and Reporting Obligations

Beyond the immediate scramble, financial institutions face stringent regulatory requirements regarding system availability and resilience. Regulators like the Financial Conduct Authority (FCA) or the Federal Reserve demand robust operational frameworks and prompt reporting of significant incidents. Failure to meet these obligations can result in hefty fines, increased scrutiny, and mandatory remediation plans. The pressure to maintain high uptime isn’t merely about good customer service; it’s a fundamental compliance issue that, if mishandled, can lead to severe legal and financial penalties, impacting the bank’s standing within the industry and its ability to operate effectively in 2026 and beyond.

Systemic Risk and Interconnectedness

Modern financial systems are incredibly interconnected, a complex web of banks, payment processors, and financial technology companies. A major server outage at one large institution can therefore trigger a cascade of problems across the entire ecosystem. Imagine a key clearing house experiencing downtime; this could halt transactions for multiple banks relying on its services, creating a widespread bottleneck. This systemic risk is a constant concern for regulators and industry players alike, highlighting the critical need for resilient infrastructure and robust contingency plans across the board. Everyone is, to some extent, linked.

The reliance on third-party service providers further complicates matters. Many banks outsource aspects of their IT infrastructure or utilize external payment gateways. If one of these critical vendors experiences an outage, it can directly impact the bank’s ability to process transactions, even if its own internal systems are fully functional. This emphasizes the importance of rigorous vendor due diligence and diversified partnerships to mitigate single points of failure. The fragility of this interconnectedness means that prevention and rapid recovery are paramount for collective financial stability.

Mitigation Strategies and Future Resilience

To combat the pervasive threat of bank server downtime, financial institutions are investing heavily in advanced mitigation strategies. This includes robust disaster recovery plans, geographically dispersed data centers, and the implementation of redundant systems that can seamlessly take over in case of a primary failure. Cloud-based infrastructure is also gaining traction, offering greater scalability and resilience compared to traditional on-premise solutions. Proactive monitoring tools and AI-driven predictive analytics are increasingly used to detect potential issues before they escalate into full-blown outages, allowing for preemptive intervention.

Looking ahead to 2026, the focus is increasingly on cyber resilience and real-time incident response capabilities. With the growing sophistication of cyber threats, banks must not only protect against technical failures but also malicious attacks designed to disrupt services. Regular stress testing, scenario planning, and continuous staff training are vital components of a comprehensive resilience strategy. Building an organizational culture that prioritizes uptime and swift recovery is perhaps the most crucial element in ensuring the stability and trustworthiness of our online financial transactions. For deeper insights into operational resilience, the Financial Stability Board offers excellent resources on their website fsb.org.

Key Takeaways

- Direct Revenue Loss & Operational Strain: Downtime immediately translates to lost sales for businesses and increased operational costs due to manual workarounds and resource diversion.

- Erosion of Customer Trust: Failed transactions severely damage customer confidence and loyalty, leading to potential churn and widespread negative reputational impact through social media.

- Regulatory & Systemic Risk: Banks face fines and scrutiny for non-compliance with operational resilience regulations, and outages can trigger cascading failures across interconnected financial systems.

- Proactive Mitigation is Crucial: Investing in redundant infrastructure, cloud solutions, AI monitoring, and comprehensive cyber resilience strategies are essential for preventing and rapidly recovering from server downtime.

Frequently Asked Questions

How often do bank server downtimes occur?

While major, widespread outages are relatively infrequent, smaller, localized disruptions can happen more often. These might affect specific services or regions. Banks continuously monitor their systems, but the complexity of modern IT infrastructure means occasional glitches are almost inevitable, though usually resolved quickly.

What should I do if my bank’s servers are down?

First, check your bank’s official channels (website, social media) for updates. Avoid repeated transaction attempts, as this can sometimes exacerbate issues. If it’s a critical payment, consider alternative methods like cash or another bank account if available, or wait for the system to recover.

Are cyberattacks a common cause of bank server downtime?

Cyberattacks, particularly Distributed Denial of Service (DDoS) attacks, are a significant and growing threat that can cause downtime. Banks invest heavily in cybersecurity to mitigate these risks. However, hardware failures, software bugs, and human error also remain common culprits for service disruptions.

How can banks improve their server uptime and resilience?

Banks can enhance resilience through redundant infrastructure, cloud adoption, robust disaster recovery plans, and proactive monitoring. Investing in AI for predictive maintenance, conducting regular stress tests, and fostering a strong cybersecurity posture are also vital for maintaining high availability.

Conclusion

The bank server downtime impact on online transactions is a multifaceted challenge that extends far beyond a simple inconvenience. It’s a critical issue affecting business profitability, consumer trust, and the stability of the entire financial ecosystem. As our reliance on digital payments grows, particularly looking towards 2026, the imperative for banks to invest in robust, resilient, and secure infrastructure becomes non-negotiable. Only through continuous innovation, vigilance, and transparent communication can we ensure the seamless, trustworthy financial experiences that modern consumers and businesses rightly demand and deserve.

Related Blogs

Published on Apr 09, 2026

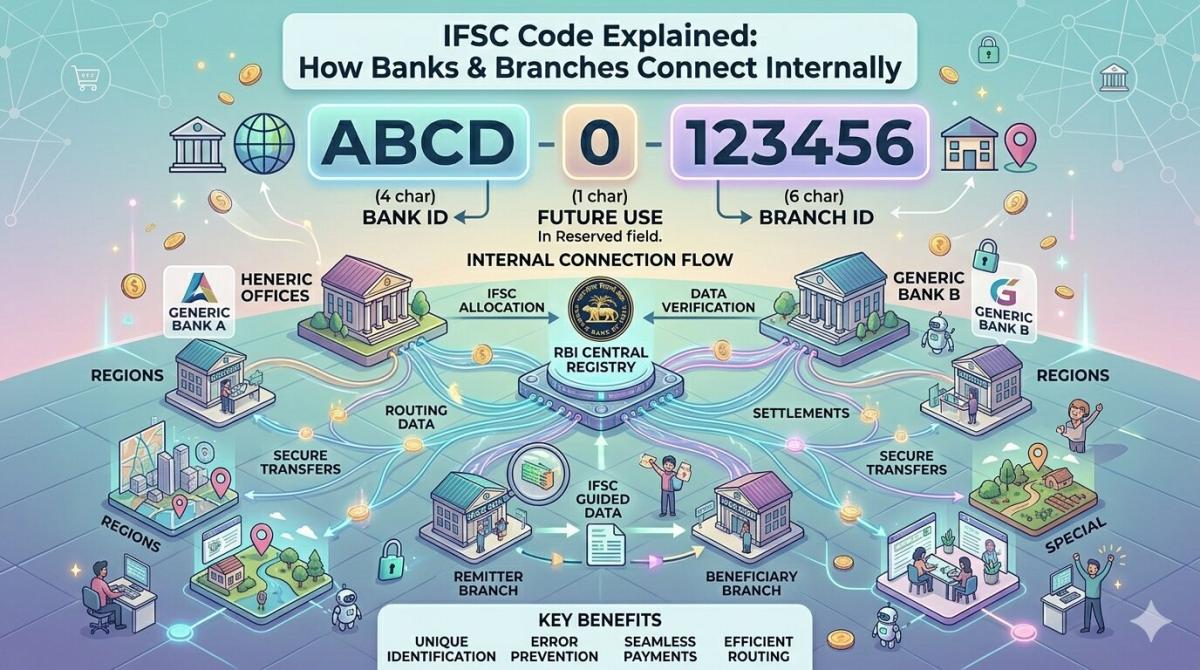

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

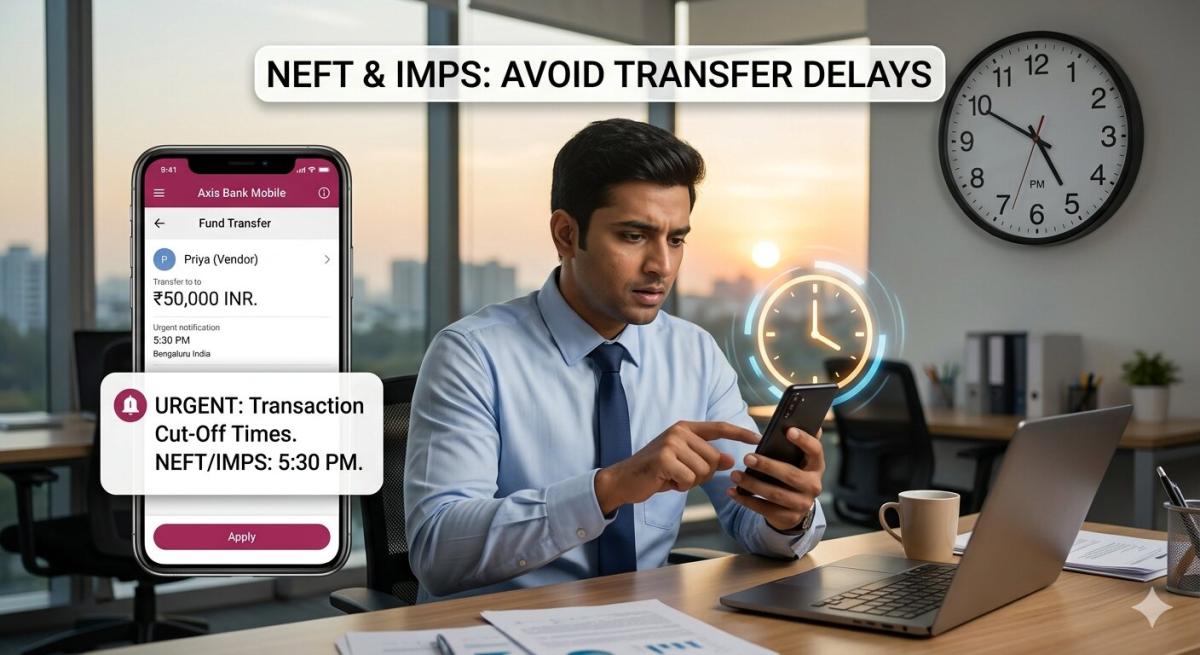

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

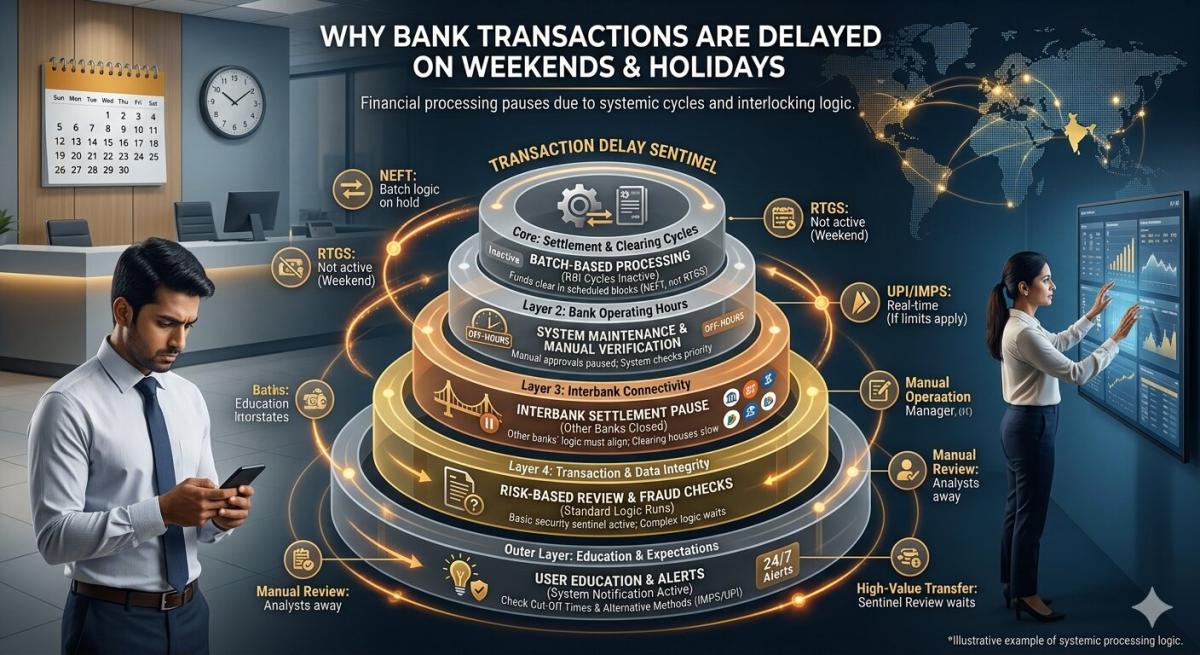

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ