Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

Arjun Sharma

Content Lead – Banking & Payments

11 min read

Table of Contents

- What is Sukanya Samriddhi Yojana?

- Who is Eligible for Sukanya Samriddhi Yojana?

- SSY Interest Rate in 2026

- SSY Calculator – Estimate Your Returns

- Tax Benefits of SSY (Section 80C Explained)

- SSY vs Fixed Deposit vs PPF – Which is Better?

- How to Open SSY Account (Step-by-Step)

- Documents Required for SSY Account

- Common Mistakes to Avoid in SSY

- Conclusion

- FAQs

In cities where costs rise faster than salaries but still many parents often rely on basic options like savings accounts or fixed deposits (FDs) that do not always keep up with long-term needs. This is where the Sukanya Samriddhi Yojana (SSY) scheme becomes relevant because it is not just another savings scheme but a government-backed plan designed specifically for a girl child’s future.

In this guide, we will learn what exactly is this Sukanya Samriddhi Yojana (SSY), how this scheme works, what rules you need to follow and under the scheme how returns are calculated.

What is Sukanya Samriddhi Yojana?

Sukanya Samriddhi Yojana is a long-term savings scheme which has been introduced by the Government of India for encouraging parents to build a dedicated financial corpus for their daughter. At its core, SSY is a deposit-based account that can be opened in the name of a girl child before she turns 10.

The account is usually managed by the parent or legal guardian, who contributes a fixed amount every year within a defined range and with time this invested money earns compounded interest, which grows the total amount significantly by the time the account matures.

Who is Eligible for Sukanya Samriddhi Yojana?

This scheme has very specific rules around who can invest and how many accounts are allowed for ensuring that the benefits are focused on supporting the financial future of the girl child:

- Girl child age limit: First thing SSY account can be opened only in the name of a girl child who is below 10 years of age at the time of opening the account. In case this age limit is crossed then unfortunately you cannot create a new SSY account.

- Who can open the account: Initially this account must be opened and managed by a parent or a legal guardian on behalf of the girl child. Here the child becomes the beneficiary and responsibilities of deposits and compliance will lie with the guardian until she becomes an adult.

- Number of accounts allowed per family: For fair usage and prevention of misuse under this scheme, one family can only open a maximum 2 SSY accounts for two girl children.

- Special case for twins or triplets: In case if a family has twin or triplet girl children then here is an exception which means more than two accounts can be opened, provided valid medical documentation is submitted.

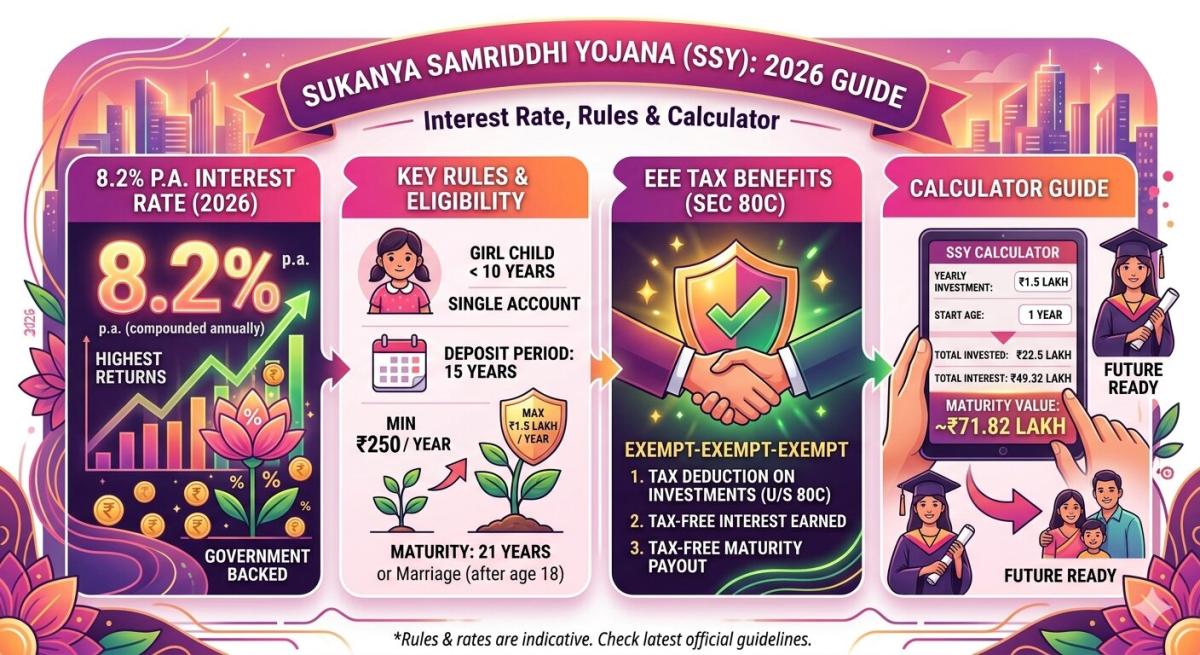

SSY Interest Rate in 2026

At present i.e 4th Qtr of FY25-26, the SSY interest rate is 8.2% per annum and it is revised quarterly by the Government of India to remain competitive among small savings schemes while offering stable returns for long term investors.

Snapshot of historical Interest Rates under SSY:

|

Period |

RATE OF INTEREST (%) |

|

01.04.2020 TO 31.03.2023 |

7.6 |

|

01.04.2023 TO 31.12.2023 |

8.0 |

|

01.01.2024 TO 31.03.2026 |

8.2 |

SSY Calculator – Estimate Your Returns

To use an SSY calculator effectively, you only need a few basic inputs and once you enter these details it will estimate your total investment, interest earned, and maturity value:

- Yearly investment amount: Decide how much you actually plan to invest every year within the allowed range of ₹250 to ₹1.5 lakh based on your budget and tax planning so that it fits comfortably into your overall financial strategy.

- Investment duration: Although the contribution period is limited to 15 years the calculator considers the full maturity period of 21 years which helps in estimating the complete growth of your investment including the compounding phase.

- Interest rate: Use the latest SSY interest rate for 2026 and ensure the calculator is applying the correct rate so that your estimated returns are as accurate and realistic as possible.

For example below are three common investment levels and how they will grow over time, assuming an average interest rate of around 8.2% p.a.

|

Yearly Investment |

Total Invested (15 yrs) |

Estimated Maturity Value (21 yrs) |

|

₹25,000 |

₹3,75,000 |

₹10–12 lakh |

|

₹50,000 |

₹7,50,000 |

₹20–25 lakh |

|

₹1,50,000 |

₹22,50,000 |

₹55–65 lakh |

These examples are not exact guarantees because interest rates do change over time but with this example we can ascertain what disciplined investing in SSY can achieve.

Tax Benefits of SSY (Section 80C Explained)

One thing to note is that SSY is one of the few investment options in India that offers complete tax efficiency across all stages of investment because as per Section 80C of the Income Tax Act, the amount you invest in an SSY account is eligible for deduction up to ₹1.5 lakh in a financial year.

This means if you are already planning to save taxes through instruments like PPF or life insurance, SSY can be included as part of that overall limit.

Another point is that SSY stands out also because of its EEE status i.e. Exempt, Exempt, Exempt which means your investment, the interest earned on investment, and the final amount you will receive at maturity all 3 are tax-free.

SSY vs Fixed Deposit vs PPF – Which is Better?

Now which option is actually better out of SSY, Fixed Deposits (FD) and Public Provident Fund (PPF) will basically depend on your financial goals, risk tolerance and time horizon.

Here is a side-by-side comparison:

|

Feature |

Sukanya Samriddhi Yojana (SSY) |

Fixed Deposit (FD) |

Public Provident Fund (PPF) |

|

Interest Rate |

Around 8% p.a. compounded annually |

Ranges between 5% to 7.5% |

Ranges around 7%–8% |

|

Lock-in Period |

Amount locked upto |

Under this lock-in is |

Amount locked upto |

|

Tax Benefits |

It provides Full EEE |

Only Interest received |

It also provides |

|

Target User |

It is only for Girl child-specific |

Can be used by |

More preferred by Long-term savers |

How to Open SSY Account (Step-by-Step)

Knowing these steps in advance can save time and avoid confusion especially in cases when we actually visit a bank or post office for the first time for these purposes:

Step-1: Choose where you want to open the account

First thing you can either open an SSY account at any authorised bank or nearby post office since most major banks across India provide this facility so it is at your choice choose the option that is most convenient, accessible and easy to manage based on your location.

Step-2: Fill out the application form

Fill up the SSY account opening application form given by the branch or downloaded online try to ensure appropriate info filling such as the name of the girl child, her date of birth and information of the guardian etc.

Step-3: Submit the required documents

When form filing is done then submit the application form along with supporting documents such as birth certificate of the girl child and identity and address proof of the parent or guardian. Try to carry also original documents so if verification is required at the branch they can be used.

Step-4: Make the initial deposit

Once documentation completes, thereafter, for activating the account there is a need to deposit at least ₹250 or any higher amount of your capability as long as it remains within the prescribed yearly investment limit of ₹1.5 lakh.

Step-5: Collect your passbook or account details

Once the entire process completes then you will receive your passbook or account confirmation that contains all transaction details and important information which must be stored safely for future tracking reference and account management purposes.

Documents Required for SSY Account

For avoiding delays or multiple visits to the bank or post office there need to be appropriate documentation work thus it is important to carry the correct commonly needed papers:

- Birth certificate of the girl child

- Identity proof of the parent or guardian such as Aadhaar card, PAN card, or voter ID

- Address proof of the parent or guardian (Aadhaar card, utility bills, or passport will work)

- Passport-sized photographs of the parent or guardian

In some cases like special situations of twins or triplets, additional medical certificates or any supporting documents may also be requested at the office that’s why it is viable to check with the bank or post office beforehand so that everything is ready in one visit.

Common Mistakes to Avoid in SSY

Although this scheme is simple, some still make some avoidable mistakes which result in reduction of overall returns. Thus, by understanding and preparing against these mistakes will help in maximising the full benefits:

- Delaying the account opening: The most common mistake is that not opening the SSY accounts before the girl child turns 10 may delay the decision and lead to missing the opportunity entirely. That's why it is crucial to start early.

- Missing yearly contributions: Another mistake is that not depositing the minimum required amount in a financial year. Thus, due to this account becomes inactive and for reviving penalty needs to be paid. Along with penalty there is another impact also i.e. it disrupts consistency and adds unnecessary effort for maintaining the investment.

- Not utilising the full 80C limit: In cases where budget is not a problem and purpose of investing is also a savings in tax then not aligning SSY contributions with the ₹1.5 lakh limit of Section 80C of income tax act can result in missing of tax saving opportunity.

- Withdrawing too early without planning: Although partial withdrawal is allowed after the age of 18 but using the funds without a clear purpose weakens the long term compounding and thus resulted in significant reduction in the final corpus.

Conclusion

In the end it can be concluded that planning for a future of daughters is not about chasing the highest returns but about choosing a reliable and consistent strategy aligned with long term goals and Sukanya Samriddhi Yojana supports this by helping us to build a dedicated corpus without unnecessary risk. SSY is also considered more not just for its interest rate or tax benefits but for the discipline it creates through regular investing which allows compounding to work effectively while also requiring awareness of its limited liquidity.

That’s why for many families the scheme of SSY becomes a dependable part of financial planning and when started early it helps manage major future expenses while providing long term stability and peace of mind.

FAQs

1. Currently in 2026 what is the interest rate of the SSY scheme?

At present (i.e 4th Qtr. of FY25-26) the interest rate of SSY is around 8.2% actually this rate is revised quarterly by the Government of India based on economic conditions and small savings scheme benchmarks just for ensuring it remains competitive compared to other safe investment options available to investors.

2. Who can open a Sukanya Samriddhi Yojana account?

Accounts under the SSY scheme can be opened by only parent or legal guardian in the name of a girl child who is currently below 10 years of age and also note that maximum of two accounts are allowed per family with exceptions applicable in case of twin or triplet girl children.

3. What is the minimum and maximum investment under the scheme of SSY?

Under this scheme minimum investment amount starts at just ₹250 per financial year and the maximum is upto ₹1.5 lakh which has been decided considering taxation benefits of Section 80C of Income Tax Act.

4. Is it even possible that we can withdraw money from SSY before maturity?

Actually yes there is an option but it is just partial withdrawal which is also restrictive. It can be accessed only when the age of girl child turns 18 then upto 50% of the balance can be used for education purposes and for full withdrawal we have to wait till maturity or specific conditions like marriage after the age of 18.

5. What will happen if due to some reasons we missed a yearly deposit of SSY?

In case if yearly deposit is not made then the account becomes inactive and for reviving it we have to pay a small penalty along with the required minimum contribution.

6. Is it actually true that SSY is completely tax free?

Yes this is true that it is completely tax free because it comes under EEE category where the investment qualifies for deduction under Section 80C and both the interest earned and the maturity amount are fully exempt from the tax.

7. For how long do I need to invest in SSY?

The investing period usually starts from the date of opening the account and continues till 15 years and once this phase is crossed there is no need for any further contributions thereafter it continues to earn interest until the maturity period at 21 years.

8. Out of SSY, PPF & Fixed Deposit, which is a better option?

If focus is only to save money for a girl child for building corpus then only better option is scheme of SSY because it offers higher interest rates, tax free returns on the other hand PPF and fixed deposits provide more flexibility and can be used for broader financial planning needs.

Disclaimer: -

This article is for informational purposes only and does not constitute financial advice. Please consult a qualified financial advisor for personalised guidance.

Related Blogs

Published on Mar 27, 2026

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

Arjun Sharma

Content Lead – Banking & Payments

Published on Mar 02, 2026

Planning an FD? Don’t Miss These Top Questions About FD Calculators

Curious how FD calculators work? This guide answers the top questions to help you calculate returns, compare plans, and invest smarter in fixed deposits.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2026

PPF (Public Provident Fund) Calculator – Returns, Interest & Planning Guide

A PPF Calculator helps you estimate the maturity value and interest earned on your Public Provident Fund investment. By entering your contribution amount, tenure, and current interest rate, you can project long-term returns and plan your savings effectively.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2026

Recurring Deposit (RD) Calculator – Returns, Interest & Maturity Guide

An RD Calculator helps you estimate the maturity amount and interest earned on your Recurring Deposit investment. By entering your monthly deposit, tenure, and interest rate, you can project returns and plan your savings effectively.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Jun 02, 2025

Understanding PPF Withdrawals: How to Plan Your Partial Withdrawals

Learn the rules and strategies for partial PPF withdrawals to meet financial goals without compromising long-term savings.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ