Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

Arjun Sharma

Content Lead – Banking & Payments

12 min read

Table of Contents

- Why Senior Citizens Prefer Fixed Deposits

- Senior Citizen FD Interest Rates in 2026 (Overview)

- Private and Mid-Sized Banks

- Top Large Banks Offering Senior Citizen FD Rates

- Which Banks Offer the Highest FD Rates in 2026?

- How to Choose the Right FD?

- Short-Term vs Long-Term FD Rates

- Tips to Maximise Your FD Returns

- Final Thoughts

- FAQs

When it comes to generating wealth or making investments after retirement, Fixed Deposits (FDs) are the top option for senior citizens. They want stability and predictability and don't usually prefer to take risks with their money. Fixed deposits are simple, stable, and predictable, making them the most preferred investment option among seniors.

In 2026, banks are offering highly competitive FD rates for senior citizens. So, now is the right time to get high returns on your deposits without risking your hard-earned money. But how do you choose the right fixed deposit? This guide will discuss everything you need to know about senior citizen FD rates in 2026.

Why Senior Citizens Prefer Fixed Deposits

Fixed deposits are certain; they do not fluctuate like stocks and bonds. You know exactly how much you will earn from your fixed deposits after a certain period of time.

Here are some of the reasons why fixed deposits are a favourite among seniors:

- Fixed and certain income: Once you have fixed your FD Rates, they remain fixed for the entire tenure.

- No market risks: Your fixed deposits will not be affected by market risks.

- Additional interest for seniors: Most banks offer an additional 0.25%-0.75% interest for seniors.

- Flexible tenure: You can choose from anything between a few months and several years.

- Easy to understand: No complex words used and no complex strategies involved. Simply put in your money, wait, and earn.

Another important factor is that you can choose how you want your interest to be paid out. If you want a regular income, you can choose from monthly and quarterly payouts. If you don't want that, you can choose a cumulative fixed deposit and enjoy compounded interest. So, fixed deposits are not only safe; they are also very convenient.

Senior Citizen FD Interest Rates in 2026 (Overview)

For 2026, banks, especially private and mid-sized banks, are offering attractive FD Rates for deposits. These interest rates vary according to tenure and bank.

Here are some of the FD rates of banks in 2026:

Private and Mid-Sized Banks

These banks will give you a slightly higher return on your fixed deposits:

|

Bank Name |

Senior Citizen FD Interest Rates (2026) |

|

IDFC First Bank |

Up to 7.25% (up to 5 years), 7.00% (above 5 years) |

|

Up to 8.00% |

|

|

Up to 7.50% |

|

|

Up to 10.51% |

|

|

Up to 7.10% |

|

|

Up to 7.71% |

|

|

Up to 6.25% |

|

|

Around 6.65% - 7.05% |

|

|

Up to 6% |

|

|

Up to 7.00% |

|

|

Up to 7.50% |

As you can see from the above list, some of these banks are offering interest rates of more than 8%. That is quite high for a low-risk investment. However, it is always important to balance high returns with safety.

Top Large Banks Offering Senior Citizen FD Rates

If you want to invest in large, established banks, they too offer attractive options.

Here is a comparison of the FD rates offered by the top banks:

- SBI: They offer up to 7.50% for long-term deposits. For 1-5 years, the FD rates are around 7.50%.

- HDFC Bank: They offer up to 7.90% for mid-term fixed deposits. For long-term deposits, the FD rates are 7.50%.

- Canara Bank: They offer up to 7.90% for 1-5 years. For long-term deposits, the FD rates are 7.20%.

- Punjab National Bank (PNB): They offer up to 7.50% for mid-term deposits.

- HSBC Bank: They offer lower FD rates compared to the others. The FD rates go up to 7.50%.

These banks may not offer the highest FD rates. However, the sense of security you get by banking with these banks is unmatched.

Which Banks Offer the Highest FD Rates in 2026?

Here are the banks offering the highest FD rates based on the data currently available.

Repco Bank - Up to 8.25%

Repco Bank is currently offering the highest FD rates. If you are looking for the highest FD rates, you should consider Repco Bank.

Yes Bank - Up to 8.00%

Yes Bank is currently offering the second-highest FD rates. You can opt for Yes Bank if you want to balance returns with stability.

DCB Bank - Up to 7.90%

DCB Bank is currently offering the third-highest FD rates. DCB Bank FDs are a viable option for growing your wealth and achieving predictable returns.

HDFC Bank & Canara Bank - Up to 7.90%

These banks also offer good FD rates. You can invest in them if you want reliability and returns.

IndusInd Bank - Up to 7.75%

IndusInd Bank offers a good middle option with decent FD rates and presence.

How to Choose the Right FD?

You must consider not only the FD rates when choosing the right fixed deposit. It is the option that best suits you. A well-chosen FD option will give you the peace of mind you want. However, a wrongly chosen FD option will keep your money locked up in the wrong place. Here's how you can choose the right FD option for yourself:

1. Safety and Trust

Fixed deposits are considered safe investments. However, the trust levels associated with the banks are also an important factor. Large public-sector banks are generally considered the safest. However, when you are investing a large sum of your savings, it is better to be safe than sorry. Therefore, you may consider the FD rates offered by the smaller banks. However, you may consider splitting the investment. It is better to be safe than sorry.

2. Your Financial Goals

Before you start investing, you must know the reason behind your investment.

- Do you want to generate income every month to meet your expenses?

- Do you have a financial goal to be met?

- Do you have excess money to invest?

Your financial goals will help you choose the kind of FD you need.

For instance:

- If you want a regular income → opt for a monthly or quarterly payout from FDs

- If you require growth → opt for cumulative FDs where interest is compounded.

Once your goal is identified, it becomes easier to choose the right FD rates and tenure.

3. Select the Right Tenure Carefully

Your FD returns are heavily dependent on the tenure you select. It is often thought that the higher the tenure of the FD, the higher the FD Rates. However, this is not necessarily the case. In fact, banks offer the best FD Rates for medium-term deposits (1 to 5 years).

To select the right FD tenure for you, follow these simple steps:

- Short-term (less than 1 year): For emergency funds or short-term parking

- Medium-term (1–5 years): Best balance of returns and flexibility

- Long-term (above 5 years): For stability and long-term planning

You should compare FD Rates across various tenures before making your decision.

4. Consider the Liquidity and Withdrawal Options

Life is uncertain. You may need your FD money at short notice. Therefore, liquidity is an important factor when you select the FD option. Most FDs offer the option of premature withdrawal. However, you may have to pay a penalty, and the FD Rates may be lower.

You should ask yourself the following questions before you select the FD option:

- Will I need the money soon?

- Do I have alternative sources of cash?

If you are unsure of your requirements, you should avoid locking up your FD for the long term. You can keep a part of the FD amount for the short term.

5. Select the Right Interest Payout Option

You should compare FD Rates across various tenures before making your decision.

- Monthly payout: Suitable for paying monthly expenses

- Quarterly payout: Higher FD Rates than the monthly payout option

- Cumulative FD: Interest is compounded and added to the principal amount

If you are not looking for regular income from your FD investment, you should go for the cumulative FD option. It is the best option because you earn compound interest, and your FD Rates will effectively be higher.

Short-Term vs Long-Term FD Rates

Let's break it down simply so you can make a wise decision.

Short-term FDs (less than 1 year)

These are the best FDs for you if you:

- Want to park your money temporarily

- Expect an increase in interest rates

- However, the FD Rates are lower.

Medium Term FDs (1-5 years)

Most banks offer the best FD Rates for medium-term FDs.

You get:

- Higher FD Rates

- Reasonable flexibility

- More planning options

This is the best option for many senior citizens.

Long Term FDs (above 5 years)

These are the best FDs for you if you:

- Want long-term stability

- Do not require immediate access to your money

- However, the FD Rates are not higher than medium-term FDs.

Therefore, you must compare the FD Rates before you invest.

Tips to Maximise Your FD Returns

Here are some practical, easy-to-follow tips to help you make the most of your fixed deposits.

1. Use the FD Laddering Strategy

If you want to ensure your FD investments are well diversified and your portfolio well balanced, we suggest you use the FD Laddering strategy.

In this strategy, you simply invest your money in multiple fixed deposits of varying durations instead of one. For example:

- Invest in an FD of 1 year

- Invest in an FD of 2 years

- Invest in an FD of 3 years

- Invest in an FD of 5 years

By following this simple strategy, you can easily diversify your investments and earn the best returns out of your FD investments.

2. Take Advantage of Rate Changes

The rate offered by a bank on a fixed deposit always fluctuates. What you earn today may not be available 6 months or 1 year down the line. So, whenever you receive your FD returns, try to invest it in another bank’s FD offering a much higher rate of interest than normal.

3. Split Large Investments

One of the most common mistakes that an investor makes is investing a huge amount of money in a single FD. And one of the best pieces of advice given by investment gurus is: “Never put all your eggs in one basket.” This simply means you should always try to invest your money in multiple FDs. And try to invest your money in multiple FDs of varying durations. By simply following this simple practice, you can easily minimize the risk associated with your investments.

4. Utilise Monthly Income Schemes

If you are an investor who wants to receive a monthly income for your expenses through your FD, then you can consider monthly income schemes. This way, you are guaranteed to receive a monthly income. Thus, at last, you are going to be able to enjoy a regular and consistent income.

Final Thoughts

FDs have always been the most-preferred investments for senior citizens to secure a fixed and guaranteed income during their retirement. Moreover, the best part is that the banks are offering the most competitive and best FD rates in 2026.

Repco Bank and Yes Bank are offering the highest FD rates. Thus, senior citizens can consider investing in these two banks to grow their investments safely and securely. However, before you start investing your hard-earned money in any type of FD, make sure you do your research and give more preference to safety and balance.

FAQs

1. Can senior citizens open an FD jointly with a family member?

Yes, senior citizens can definitely open joint FD accounts with their family members. In fact, senior citizens prefer to open joint FD accounts with their family members. The only condition for doing so is that the primary account holder must be a senior citizen.

2. Do senior citizen FD rates automatically apply, or do I need to ask for them?

Also, most banks in India offer the same interest rates to almost all senior citizens. So, you don’t have to worry about that either. However, it is always recommended to double-check before investing.

3. Is there a maximum limit to the amount of money that can be invested in senior citizen FDs?

No, there isn’t a limit to the amount of money that can be invested in a senior citizen FD. You can invest as much money as possible in the FD.

4. Can the payout option be changed after opening the FD?

No, once your FD has been locked in, there are no changes that can be made to it. You simply have to wait for it to mature.

5. Do banks offer higher FD rates for specific FD tenures like special schemes?

Yes, many banks do offer limited-period FD schemes with higher FD Rates or better terms during festive seasons or other special occasions.

6. What happens to the FD in case the investor forgets to make a payout?

If the investor forgets to make a payout, the bank automatically reinvests the FD at existing rates or informs the investor of the same.

7. Can a loan be taken against the FD in the case of senior citizens?

Yes, most banks allow investors to take loans against their FDs. It’s a quick loan with minimal paperwork and a relatively lower interest rate.

8. Is TDS applicable to the interest earned on senior citizen FDs?

Yes, it is applicable. However, the investor can avoid this by submitting Form 15H to the bank if his/her total income is below the taxable limit.

Related Blogs

Published on Mar 27, 2026

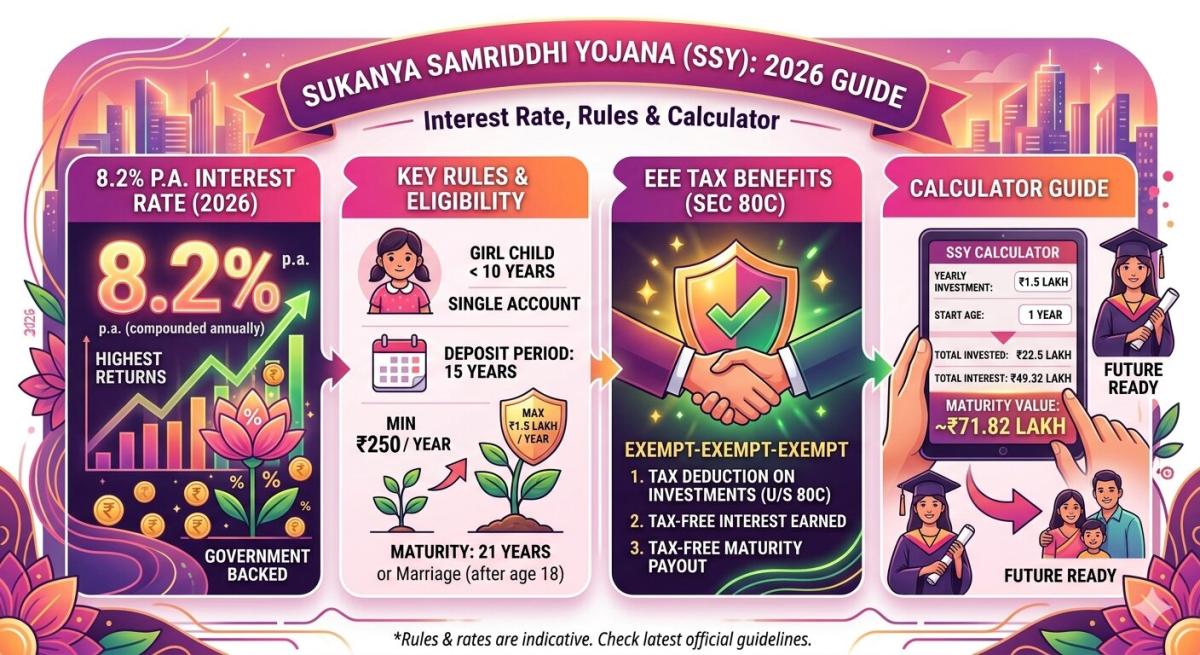

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

Arjun Sharma

Content Lead – Banking & Payments

Published on Mar 02, 2026

Planning an FD? Don’t Miss These Top Questions About FD Calculators

Curious how FD calculators work? This guide answers the top questions to help you calculate returns, compare plans, and invest smarter in fixed deposits.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2026

PPF (Public Provident Fund) Calculator – Returns, Interest & Planning Guide

A PPF Calculator helps you estimate the maturity value and interest earned on your Public Provident Fund investment. By entering your contribution amount, tenure, and current interest rate, you can project long-term returns and plan your savings effectively.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2026

Recurring Deposit (RD) Calculator – Returns, Interest & Maturity Guide

An RD Calculator helps you estimate the maturity amount and interest earned on your Recurring Deposit investment. By entering your monthly deposit, tenure, and interest rate, you can project returns and plan your savings effectively.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Jun 02, 2025

Understanding PPF Withdrawals: How to Plan Your Partial Withdrawals

Learn the rules and strategies for partial PPF withdrawals to meet financial goals without compromising long-term savings.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ