ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

Arjun Sharma

Content Lead – Banking & Payments

11 min read

Table of Contents

- ELSS vs PPF vs NPS: What You Should Know

- ELSS: What is it?

- What is PPF?

- What is NPS?

- ELSS vs. PPF vs. NPS: Which One Offers the Best Returns?

- ELSS vs PPF vs NPS: Risk vs Return

- What is the right investment option based on your risk tolerance?

- ELSS vs PPF vs NPS: Lock-in Period

- ELSS vs PPF vs NPS: Tax Benefits Explained

- ELSS vs PPF vs NPS: Liquidity and Withdrawal Rules

- ELSS vs PPF vs NPS: Who Should Invest in What?

- A Practical Way to Decide

- Can You Invest in All Three Schemes?

- ELSS vs PPF vs NPS: Which among these three is the Best?

- Conclusion

- FAQs

Nowadays, everybody wants to invest their money and grow it over a period of time. But the problem is that selecting the best investment option for this purpose is a difficult task due to the availability of a large number of schemes in the market.

The three main options for investment are: Equity Linked Savings Scheme (ELSS), Public Provident Fund (PPF), and National Pension System (NPS).

In this guide, we will help you understand everything about these schemes and select the best investment option that provides the best returns on investment.

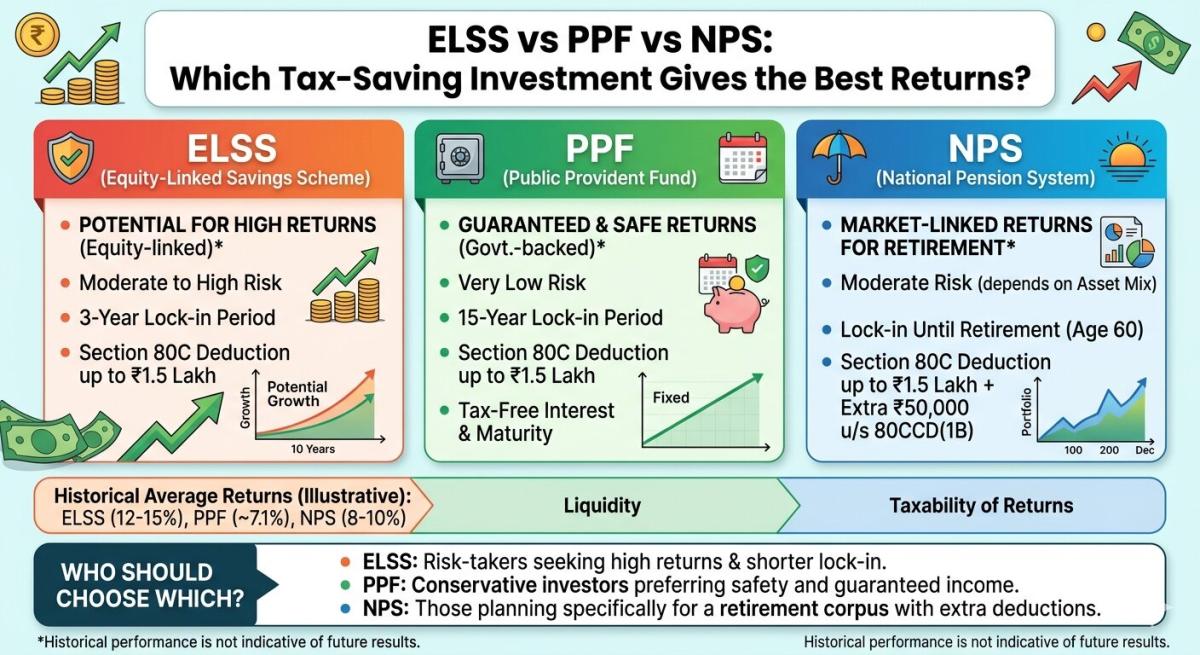

ELSS vs PPF vs NPS: What You Should Know

If you want to save tax and grow your money, these three options can help. Each one works differently, so it’s important to understand them before you choose.

ELSS: What is it?

ELSS is a type of mutual fund that primarily makes stock investments. It is well-liked because it mostly has the highest profits. Additionally, it has the shortest lock-in term of any Section 80C tax-saving option—just 3 years. Returns are not fixed and may change based on the stock market because it is connected to it.

What is PPF?

PPF scheme is a government-sponsored savings scheme. It is considered to be a very safe investment option available in the market. The interest rate is fixed; that is also decided by the government and may change over a period of time. The lock-in period is longer; however, after a certain period of years, you can withdraw money partially.

What is NPS?

If you are looking for a retirement plan, then NPS is for you. In this plan you can invest in equity, corporate debt, and government securities. It has a longer lock-in period till you retire, thus making it suitable for long-term wealth creation.

ELSS vs. PPF vs. NPS: Which One Offers the Best Returns?

This question is the most important for most people, and the answer depends on how you define 'best.'

ELSS

If you are concerned with numbers, then ELSS seems to be the best option in the long term, as it invests in the stock market, which promises higher returns in the long term compared to other traditional saving instruments. Over a period of 10-15 years, ELSS tends to offer 10-15% returns.

In certain markets, the returns can even be higher. However, depending on the market it has ups and downs. In certain years, the returns might be low or even negative.

PPF

PPF is all about stability. The returns are fixed and government-guaranteed. The returns generally remain between 7-8%. While this may seem lower than ELSS, the main advantage is that you know exactly what you are going to get from your investments. Also, the returns are entirely tax-free.

NPS

NPS falls between the two investment options above. It is neither entirely dependent on equities, as in ELSS, nor entirely fixed, as in PPF. NPS includes a mix of various funds like corporate bonds, government securities.and equity. Thus, with such a diverse portfolio the returns usually lie between 8% to 12%.

So, if we talk about the potential returns:

- ELSS has the highest growth potential

- NPS has balanced growth

- PPF has stable growth

However, the best returns also depend upon how much time you have. While ELSS may be unpredictable over short periods, it is the best over longer periods. PPF is stable but slow. On the other hand, NPS is a middle-of-the-road option for long-term retirement planning.

ELSS vs PPF vs NPS: Risk vs Return

Let’s understand the risk and return ratio among the three, as it is important to understand it to make a sound judgement. Let us understand this in simple terms.

ELSS

ELSS involves high risks because it is tied to the stock market. The value of your investment may increase or decrease depending upon the market. If the stock market is in a declining state, then the value of your investment may also decline in the short term. It may cause you some distress. However, in the long term, the stock market is likely to increase and grow.

PPF

PPF is one of the safest investment plans. The returns on your investment will not be affected by the stock market. There is almost no risk to your capital. Therefore, it is one of the safest investment plans that can help you achieve your financial objectives without worrying about the stock market.

NPS

NPS offers you a balance between returns and risk as it invests in a mix of assets. It doesn't fluctuate much and mostly remains stable.

What is the right investment option based on your risk tolerance?

- If you are young, have a stable income, and can handle some ups and downs in life, it is better to take on more risk and invest in ELSS.

- If you are close to your financial goal or simply don't like uncertainty and don't want to take any risks, then it is better to invest in PPF.

- If you want the best of both worlds and achieve your long-term financial goals, it is better to invest in NPS.

In simple terms, choose what you are comfortable with. The best investment is not one with the highest return, but one that you can stay with in bad times as well.

ELSS vs PPF vs NPS: Lock-in Period

The lock-in period is a significant factor in deciding which investment option is the best.

- ELSS has a minimum lock-in period of 3 years

- PPF requires you to lock in your savings for 15 years

- NPS requires you to lock in your savings till retirement

If you need flexibility, then ELSS is the clear winner. If you are willing to keep your savings locked in for a long time, you can choose either PPF or NPS.

ELSS vs PPF vs NPS: Tax Benefits Explained

All three options provide tax benefits, although there are some variations.

Under Section 80C

You can claim up to ₹1.5 lakhs under this section by investing in:

- ELSS

- PPF

- NPS

Extra Benefit in NPS

In NPS, you can claim an additional ₹50,000 under Section 80CCD(1B). This is over and above the ₹1.5 lakhs. This makes NPS an extremely attractive option for you if you need to save tax.

ELSS vs PPF vs NPS: Liquidity and Withdrawal Rules

Liquidity refers to the ability to withdraw your funds easily.

- ELSS: You can withdraw after 3 years

- PPF: You can make partial withdrawals after 5-7 years

- NPS: Limited withdrawal options available before retirement

If you need liquidity, then ELSS is the best option.

ELSS vs PPF vs NPS: Who Should Invest in What?

If we take into consideration your risk appetite, investment period, etc., it would be much easier for you to select from these three options. Here is a detailed description of each option for you to understand better:

Choose ELSS if:

You are a person who is looking to grow your savings much more quickly and is willing to take risks for it. It is also suitable for you if you do not want to keep your investments for a long time, as it is a 3-year lock-in product. If you are looking for creating wealth in the long term, for example, creating huge amounts of money for future requirements, etc., then ELSS can be a suitable option.

Choose PPF if:

You want safety rather than high returns. PPF is ideal for people who want to earn assured returns without taking any investment risks. If you are saving for your child's education or building a secure financial cushion for yourself PPF is a good choice for long-term goals. Also due to its long lock-in period, it encourages disciplined savings. If you want tax-free returns and absolute security, PPF is a very reliable choice.

Choose NPS if:

If you are planning for your retirement and want a steady, long-term income stream. NPS is ideal for this purpose. It is also suitable for people who are long-term thinkers and are comfortable locking in their money until they retire. In this way, you will be able to enjoy diversification, as your money will be invested across different asset types.

Another big advantage is that you can enjoy additional tax deduction, which is why NPS is suitable for people who want to save tax.

A Practical Way to Decide

Instead of choosing one, you could consider dividing your investments based on your goals.

For example:

- Use ELSS for growth and wealth creation

- Use PPF for stability and safety.

- Use NPS for retirement planning.

This way, you can achieve a balance between risk and return and your financial objectives.

Can You Invest in All Three Schemes?

The answer would be: Yes, you can. In fact, any smart investor invests in all these schemes to make their portfolio diversified.

For example:

- Use ELSS for growth and wealth creation.

- Use PPF for stability and safety.

- Use NPS for retirement planning.

This way, you are able to achieve the best of all worlds!

Real-Life Example

Let us understand this further with a real-life example.

Assume you are investing ₹1.5 lakhs per year in these schemes.

- Your money grows faster in ELSS, but it is volatile.

- Your money grows steadily with PPF, and it is safe.

- Your money grows moderately with NPS and is useful for retirement planning.

After 15-20 years, the money in an ELSS grows the most, but it is volatile. The money in the case of PPF grows steadily, but is low. The money in an NPS account grows moderately and is useful for retirement planning.

ELSS vs PPF vs NPS: Which among these three is the Best?

As you already know the details of these schemes by now, the next question is: Among these three, which is the best?

Well, the answer is quite simple: there is no single best investment scheme. Each of these schemes is designed for a purpose and is the best in its respective field.

Highest Returns

If you are looking to invest in a scheme that offers the highest possible returns and are comfortable investing in the stock market, the best option is an ELSS scheme. The reason is that, in the long run, this scheme has the potential to grow your money faster than the other two.

Stability and Security

If your main aim is safety coupled with assured returns, then PPF is the way to go. It may not offer the highest returns, but it does offer something equally valuable.

Retirement Planning

If you are planning for your retirement, you need a more stable approach to building wealth, coupled with additional tax savings. In such a case, NPS would be the best option.

The smartest investors, however, are not the ones who put all their eggs in one basket. They know that investments have different purposes.

In the end, the best investment option is not the one offering the highest returns. It is the one offering the best combination of options. Therefore, when you are investing with a clear mind, all three options can help you build a great future.

Conclusion

The decision of whether or not to invest in ELSS, PPF, or NPS ultimately depends on the benefits of each option. It does not depend on which option performs the best.

Therefore, if you are new to investments, then ELSS would be a great option. If you are looking for stability, PPF is the way to go. And if you are thinking from a future perspective, then NPS would be a great option.

The smartest option, however, is not to put all your eggs in one basket. But investing in all three would be best as it will provide all the benefits that these three have to offer.

FAQs

1. Can I redeem or switch my investment from ELSS to another fund once the lock-in period of 3 years is completed?

Yes, once the lock-in period is completed, you can redeem your investment in the mutual fund scheme at any point of time.

2. What will happen if I stop investing in PPF before 15 years?

Your account remains active, but you may face penalties and reduced benefits until you resume contributions.

3. Is it possible to change asset allocation in NPS later?

Yes, NPS allows you to adjust your equity and debt allocation periodically as your goals or risk level change.

4. Can I have both a Tier 1 and Tier 2 account in NPS?

Yes, but only Tier 1 offers tax benefits, while Tier 2 works more like a flexible investment account.

5. Do dividends from ELSS funds get taxed?

Yes, dividends are added to your income and taxed as per your income tax slab.

6. Can I extend my PPF account after maturity?

Yes, after 15 years, you can extend it in blocks of 5 years with or without additional contributions.

7. Can I invest in ELSS through SIP?

Yes, you can invest in ELSS funds through SIP. However, each SIP installment will have its own 3-year lock-in period.

8. Is partial withdrawal allowed in PPF?

Yes, partial withdrawals are allowed from the 7th financial year onwards, subject to certain limits set by the rules.

Related Blogs

Published on Mar 26, 2026

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

Arjun Sharma

Content Lead – Banking & Payments

Published on Mar 02, 2026

What is a Lumpsum Calculator and How Does It Work? Benefits, Accuracy & Planning Tips

Learn how a Lumpsum Calculator works, how it estimates one-time investment returns, and how to use it for smarter financial planning.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2026

Mutual Fund Returns Calculator: How It Works, Accuracy & FAQs Explained

A Mutual Fund Returns Calculator helps you estimate the future value of your mutual fund investment using inputs like investment amount, tenure, contributions, and expected returns. It uses compounding to project potential growth and helps you plan smarter investment decisions.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 10, 2025

Financial Planning: Using SIP Calculators Effectively

Confused about future finances? Learning how to use SIP Calculators can help you reach your goals! Invest small, grow big.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 22, 2025

SIP Explained: How SIP is Calculated for Indian Investors

Invest smart in India with SIPs! Learn how SIP is calculated, the benefits, and grow your wealth through cost averaging & compounding

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ