Bank Settlement Cycle: Explained in Simple Terms

Ever wonder why your money isn't instant? Learn how the bank settlement cycle works, the difference between clearing and settlement, and the role of RTGS in 2026.

Table of Contents

Have you ever transferred money to a friend or paid a bill online, only to find the funds aren’t immediately available to the recipient? That brief, often frustrating delay isn’t just your bank being slow; it’s a fundamental part of the financial plumbing known as the Bank Settlement Cycle. It’s the invisible, intricate dance that ensures money truly moves from one account to another, guaranteeing finality and trust in every transaction. As someone who’s spent years peering into the gears of global finance, I can tell you this cycle is far more fascinating and critical than most people realize, underpinning the entire economy and ensuring your money is where it’s supposed to be, eventually.

What Exactly Is Bank Settlement?

At its heart, bank settlement is the conclusive transfer of funds or securities between two parties, marking the point where an obligation is discharged. It’s the moment of truth when ownership truly changes hands, and the transaction becomes irreversible. Think of it as the final handshake after a complex negotiation – all promises are fulfilled, and everyone can move on. Before settlement, a transaction might be “cleared,” meaning the banks have communicated and agreed on the details, but the actual value hasn’t yet moved.

This distinction between clearing and settlement is crucial. Clearing is like checking if all the paperwork is in order and everyone agrees on the amount. Settlement, however, is the actual exchange of value, making the funds available for use. Without a robust settlement process, the financial system would be rife with credit risk, as there would be no guarantee that one party would actually receive the funds it’s owed. It’s the bedrock upon which all modern financial transactions, from a simple debit card swipe to multi-million dollar interbank transfers, are built.

The Core Steps of the Cycle

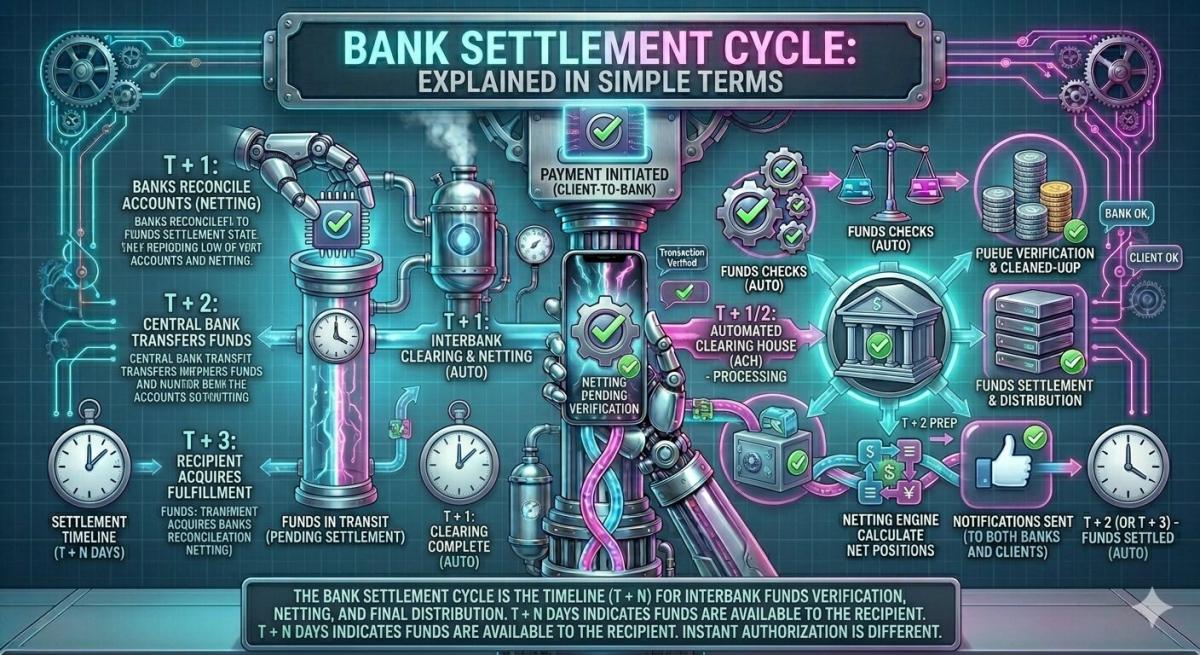

Understanding the bank settlement cycle involves breaking it down into a few distinct stages. It typically begins with a payment instruction, initiated by you through your bank. This could be a direct debit, a wire transfer, or a check deposit. Your bank then sends this instruction to a clearinghouse or directly to the receiving bank, depending on the payment type and network. This initial phase is about communicating the intent to move funds.

The next critical step is clearing, where the banks involved exchange information and reconcile accounts to determine the net obligations between them. For instance, if Bank A owes Bank B several payments, and Bank B also owes Bank A, they might net these amounts out. Finally, settlement occurs. This is the actual transfer of value, usually through accounts held at a central bank. Once the central bank debits the sending bank’s account and credits the receiving bank’s account, the settlement is final and irrevocable, typically confirmed back to the participating institutions. For a deeper dive into how central banks facilitate this, the Federal Reserve’s resources on payment systems are invaluable.

Different Types of Settlement

Not all settlements are created equal; the method largely depends on the urgency and value of the transaction. One primary method is Real-Time Gross Settlement (RTGS), which processes payments individually and continuously throughout the day. Each transaction settles on a one-to-one basis, meaning the full value of the payment is transferred without netting against other payments. This significantly reduces systemic risk, as the finality of funds is achieved almost instantly. High-value interbank transfers, for example, often utilize RTGS systems globally.

Conversely, Net Settlement systems aggregate multiple payments over a period, often a day, and then settle the net difference between participants. This is common for lower-value, high-volume transactions, such as those processed through Automated Clearing House (ACH) networks. While net settlement is more efficient in terms of liquidity, as banks only need to hold enough funds for the net amount, it introduces a degree of systemic risk because finality only occurs at the end of the netting period. Should a participant default before final settlement, it could ripple through the system. The choice between gross and net settlement is a constant balancing act between efficiency and risk mitigation in financial infrastructure, a balance that continues to evolve, especially looking ahead to 2026.

Why RTGS is a Game Changer

Real-Time Gross Settlement (RTGS) systems truly revolutionized the financial world by providing immediate finality for high-value payments. Before RTGS, banks often faced significant counterparty risk, as they might have extended credit based on payments that hadn’t yet been definitively settled. With RTGS, once a payment is executed, it’s done – the funds are irrevocably transferred. This drastically reduces the potential for a domino effect if one bank experiences financial distress, thereby bolstering overall financial stability. It’s like moving from a system of IOUs to immediate cash exchanges for critical transactions.

Key Players and Their Roles

The settlement cycle isn’t a solo act; it involves a sophisticated cast of characters, each playing a vital role. At the forefront are the Originating Bank and the Receiving Bank, your everyday financial institutions that hold your accounts and initiate or receive payment instructions. They are the direct interfaces for consumers and businesses, translating your payment requests into the language of the financial system. Their internal systems manage ledgers and communicate with external networks, ensuring your money leaves or arrives at the correct destination.

Beyond these direct banks, Clearing Houses and Payment System Operators are indispensable. Organizations like the Federal Reserve (for Fedwire and ACH in the U.S.) or global networks like SWIFT (Society for Worldwide Interbank Financial Telecommunication) provide the infrastructure for banks to exchange payment messages and calculate net obligations. Finally, Central Banks act as the ultimate arbiters and settlement agents. They provide settlement accounts for commercial banks and ensure the finality of payments, often through their own RTGS systems. Their role as the “bankers’ bank” is critical for maintaining liquidity and stability across the entire financial ecosystem.

Why Does It Matter to You?

While the bank settlement cycle might seem like a technical abstraction, its efficiency and robustness directly impact your daily financial life. The speed at which your paycheck clears, how quickly a vendor receives your payment, or even the availability of funds after a stock trade are all dictated by this underlying process. A slow or inefficient settlement cycle can lead to liquidity issues for businesses, delayed access to funds for individuals, and increased credit risk across the economy. Understanding this helps you contextualize why some transactions are instant, while others take a day or two.

Looking ahead to 2026, the ongoing evolution of payment systems, including the rise of instant payment initiatives like FedNow in the US, aims to compress these settlement times dramatically. This movement towards real-time payments is driven by consumer demand for immediate access to funds and businesses seeking faster cash flow. However, even with instant payments, the core principles of the bank settlement cycle remain; the difference lies in the technology and infrastructure that accelerate the clearing and finality of transactions, making the invisible gears spin much faster and more seamlessly than ever before.

Key Takeaways

- Settlement vs. Clearing: Clearing is the agreement on transaction details; settlement is the final, irrevocable transfer of value and ownership. This distinction is fundamental to understanding payment delays.

- Risk Mitigation: The bank settlement cycle, especially through Real-Time Gross Settlement (RTGS), is crucial for reducing systemic risk in the financial system by providing immediate finality for high-value payments.

- Impact on Daily Life: The efficiency of settlement directly affects when funds become available to you, influencing personal finance, business cash flow, and the overall pace of economic activity.

- Evolving Landscape: The drive towards instant payment systems, exemplified by initiatives like FedNow, is transforming the settlement landscape, aiming to provide near real-time finality while maintaining security and stability, a trend set to be prominent in 2026.

Frequently Asked Questions

How long does the bank settlement cycle typically take?

The duration varies significantly based on the payment type and system. High-value transactions via RTGS can settle in seconds or minutes. Lower-value, batch-processed payments (like ACH transfers) might take 1-3 business days for final settlement, often referred to as T+1 or T+2, meaning transaction date plus one or two days.

What is the difference between “cleared” and “settled” funds?

Cleared funds mean your bank has recognized the incoming payment and credited your account, but the underlying interbank settlement might not be final. Settled funds mean the actual transfer of value between the banks involved has been completed, making the transaction irrevocable and the funds truly yours to use without reversal risk.

Can a bank settlement be reversed?

Once a payment is fully settled, especially through a Real-Time Gross Settlement (RTGS) system, it is generally considered final and irrevocable. Reversals are extremely rare and typically only occur in cases of fraud or error, requiring complex legal and banking procedures, often with the consent of both parties.

How do international bank settlements work?

International settlements are more complex, often involving multiple banks and different currencies. They typically rely on correspondent banking relationships and messaging systems like SWIFT to relay payment instructions. Final settlement usually occurs through accounts held at central banks or through specialized clearinghouses in the respective countries, often taking several days due to time zone differences and processing windows.

Conclusion

The bank settlement cycle, though often hidden from view, is the unsung hero of our financial world. It’s the intricate, carefully orchestrated process that transforms a mere promise of payment into a definitive transfer of value, ensuring trust and stability across billions of transactions daily. From safeguarding against systemic risks to impacting when your funds become available, its importance cannot be overstated. As we move towards increasingly instant payment systems, the fundamental principles of finality and security that underpin the settlement cycle will remain paramount, continuing to evolve for a more seamless financial future in 2026 and beyond.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ