Clearing Houses: Essential for Secure & Efficient Banking Transactions

Discover how clearing houses act as central counterparties to prevent financial chaos. Learn about risk mitigation, margin requirements, and their role in market stability.

Table of Contents

Imagine a bustling financial marketplace, millions of transactions occurring simultaneously, each party trusting the other implicitly. Now, imagine that same market without traffic lights, without rules, without a central authority ensuring everyone honors their commitments. Chaos, right? That’s precisely the scenario the financial world faced before the widespread adoption of clearing houses. Their pivotal

The Role Of Clearing Houses In Banking Transactions

is to act as the essential traffic cop, bringing order, stability, and efficiency to an otherwise incredibly complex and risky system, a function I’ve often seen underestimated by those outside the industry.

The Fundamental Problem Clearing Houses Solve

Before the advent of robust clearing systems, banking transactions, especially interbank ones, were fraught with counterparty risk. Each bank had to assess the creditworthiness of every other bank it traded with directly. If Bank A bought a security from Bank B, Bank A was exposed to Bank B defaulting before delivery, and vice-versa. This bilateral exposure created a tangled web of risks, where the failure of one major institution could trigger a cascade of defaults across the entire financial ecosystem, a stark reality that became painfully evident during historical financial crises.

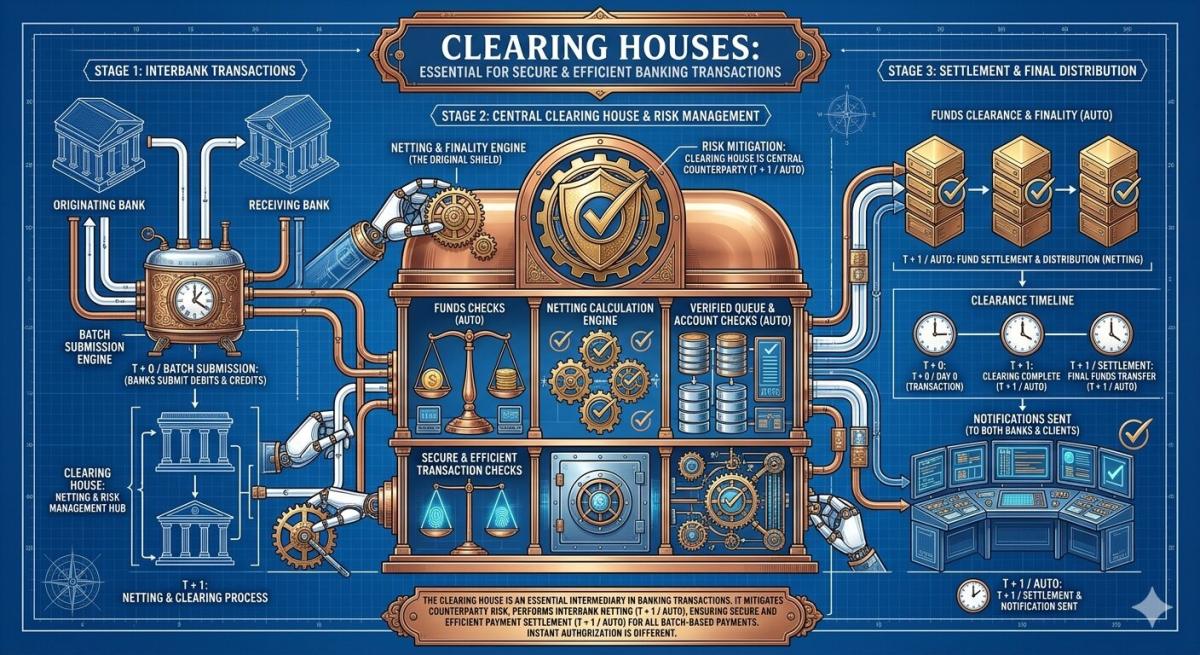

Clearing houses stepped in to untangle this web by becoming a central counterparty (CCP). They effectively interpose themselves between the original buyer and seller. This process, known as novation, means the clearing house becomes the buyer to every seller and the seller to every buyer. This fundamentally transforms a network of bilateral risks into a series of bilateral risks with a single, highly regulated entity, drastically simplifying risk management and significantly reducing the potential for systemic contagion across the banking sector.

How Clearing Houses Mitigate Risk

The core mechanism through which clearing houses mitigate risk is a multi-layered system of financial safeguards. Primarily, this involves demanding collateral, known as margin, from all participants. Initial margin is collected upfront to cover potential future losses, while variation margin is settled daily (or even intra-day) to account for changes in the market value of positions. This “skin in the game” approach ensures that participants have a vested interest in honoring their obligations and provides a buffer against adverse market movements.

Beyond margin, clearing houses maintain substantial default funds, often contributed by their members, which act as an additional layer of protection. These funds are structured to absorb losses that might exceed a defaulting member’s margin contributions. Furthermore, strict membership criteria and robust risk management frameworks, including stress testing and liquidity management, are continuously refined. My experience tells me that these combined safeguards are what allow clearing houses to confidently manage trillions of dollars in transactions daily, providing a bedrock of stability for global finance.

The Importance of Initial and Variation Margin

Initial margin is like a security deposit, collected at the outset of a trade to cover potential losses from adverse price movements over a specified liquidation period. It’s a crucial component of a CCP’s risk management framework, ensuring that even if a participant defaults, there’s enough capital already on hand to cover the costs of unwinding their positions. Variation margin, on the other hand, is the daily (or more frequent) settlement of profits and losses based on market-to-market valuations. If your position loses value, you pay variation margin; if it gains, you receive it. This continuous true-up prevents the accumulation of large, unsecured exposures, which is vital for maintaining market integrity and liquidity.

Operational Efficiency and Market Integrity

Beyond risk mitigation, clearing houses are indispensable for fostering operational efficiency within banking transactions. By centralizing the settlement process, they significantly reduce the administrative burden on individual banks. Instead of reconciling trades with dozens or hundreds of different counterparties, banks only need to settle their net positions with the clearing house. This netting process dramatically reduces the number of payments and deliveries required, freeing up capital and operational resources that would otherwise be tied up in managing complex bilateral relationships. This efficiency is a quiet but powerful force in keeping transaction costs down for everyone.

Moreover, clearing houses play a critical role in maintaining market integrity and transparency. By providing a centralized point for trade information and often facilitating price discovery, they help ensure fair and orderly markets. The data collected by clearing houses offers regulators and market participants valuable insights into overall market exposures, liquidity, and potential vulnerabilities. This transparency is crucial for regulatory oversight and for building confidence among market participants, ensuring that the financial system remains robust and trustworthy, especially as we look towards the complexities of 2026 and beyond.

Clearing Houses in the Derivatives Market

The role of clearing houses became particularly prominent and critically important following the 2008 global financial crisis, especially concerning the vast, opaque over-the-counter (OTC) derivatives market. Before 2008, many OTC derivatives were traded bilaterally, leading to immense, hidden counterparty risk that contributed significantly to the systemic breakdown. Regulators worldwide, notably through the G20 commitments, mandated a shift towards central clearing for standardized OTC derivatives, recognizing that greater transparency and risk management were desperately needed in this complex sector. This regulatory push fundamentally reshaped the landscape of derivatives trading.

Today, a significant portion of the derivatives market, from interest rate swaps to credit default swaps, is centrally cleared. This transition has dramatically enhanced the stability of these markets by imposing standardized risk management practices, collateral requirements, and default management protocols. While not without its own set of challenges, central clearing has undoubtedly made the derivatives market more resilient and less prone to the kind of cascading failures witnessed in the past. It’s a testament to how proactive regulatory intervention, leveraging the infrastructure of clearing houses, can fundamentally strengthen the financial system. For more in-depth information, the Bank for International Settlements (BIS) offers extensive publications on central counterparty clearing at bis.org.

Challenges and Future Outlook

Despite their undeniable benefits, clearing houses are not without their challenges. One prominent concern is the concentration of systemic risk. By centralizing risk, a clearing house itself becomes a single point of failure. While they are heavily capitalized and regulated, a catastrophic failure of a major CCP could have devastating consequences for the global financial system. Regulators are acutely aware of this, constantly refining stress tests, recovery and resolution plans, and ensuring robust governance structures. This balancing act – centralizing risk to manage it better, while simultaneously mitigating the risk of that centralization – is a complex ongoing endeavor.

Looking ahead to 2026 and beyond, clearing houses are also grappling with technological advancements and evolving market structures. The rise of blockchain and distributed ledger technology (DLT) presents both opportunities for greater efficiency and new challenges for integration and regulation. Furthermore, the need for enhanced global regulatory cooperation remains paramount to ensure consistent standards and effective oversight across jurisdictions. The dynamic nature of financial markets means clearing houses must continuously innovate and adapt, balancing stability with the imperative for efficiency and progress. Another excellent resource for understanding regulatory perspectives on clearing is the Commodity Futures Trading Commission (CFTC) at cftc.gov.

Key Takeaways

- Clearing houses act as central counterparties (CCPs), interposing themselves between buyers and sellers to transform bilateral risks into risks with a single, highly regulated entity, thereby drastically reducing counterparty risk.

- They employ a multi-layered risk mitigation framework, including initial and variation margin requirements, default funds, and stringent membership criteria, to safeguard against participant defaults and ensure financial stability.

- CCPs significantly enhance operational efficiency by centralizing settlement and netting transactions, which reduces the number of payments and deliveries, freeing up capital and streamlining processes for banks.

- The push for central clearing of OTC derivatives post-2008 demonstrated their critical role in bringing transparency and stability to complex markets, making the financial system more resilient against systemic shocks.

Frequently Asked Questions

What is a Central Counterparty (CCP)?

A Central Counterparty (CCP) is a financial institution that interposes itself between counterparties to contracts traded in one or more financial markets, becoming the buyer to every seller and the seller to every buyer. This process, known as novation, guarantees the performance of trades, even if one of the original parties defaults, significantly reducing counterparty risk.

How do clearing houses prevent a domino effect in the financial system?

Clearing houses prevent a domino effect by mutualizing risk and providing robust safeguards. By requiring margin and maintaining default funds, they absorb losses from defaulting members without directly impacting other participants. This ring-fencing of risk prevents the failure of one institution from triggering a cascade of failures across the entire market, maintaining systemic stability.

Are all financial transactions cleared through a clearing house?

No, not all financial transactions are cleared through a clearing house. While a significant portion of exchange-traded derivatives, equities, and increasingly, standardized over-the-counter (OTC) derivatives are centrally cleared, many bespoke OTC transactions and certain types of bilateral loans or foreign exchange trades may still be settled directly between counterparties without a CCP. The trend, however, is towards greater central clearing for systemic risk reduction.

What happens if a clearing house itself faces financial distress?

A clearing house facing financial distress is a serious concern, given its systemic importance. They are heavily regulated and subject to strict capital requirements, stress tests, and recovery and resolution plans. These plans outline steps, such as using their own capital, accessing default funds, making calls for additional collateral, or even unwinding positions, to manage a crisis and prevent broader market disruption. Global regulators work to ensure these entities are robust enough to withstand extreme scenarios.

Conclusion

In the intricate ballet of global finance, clearing houses are the unsung heroes, diligently orchestrating order and stability behind the scenes. Their role in banking transactions is far more than just administrative; it’s foundational, providing the critical infrastructure that mitigates risk, enhances efficiency, and fosters market integrity. As markets evolve and new challenges emerge, the adaptive nature and robust safeguards of these institutions will remain indispensable. They are, quite simply, essential for the smooth, trustworthy, and resilient functioning of our modern financial world, a truth that becomes clearer with every passing year, including 2026.

Related Blogs

Published on Apr 09, 2026

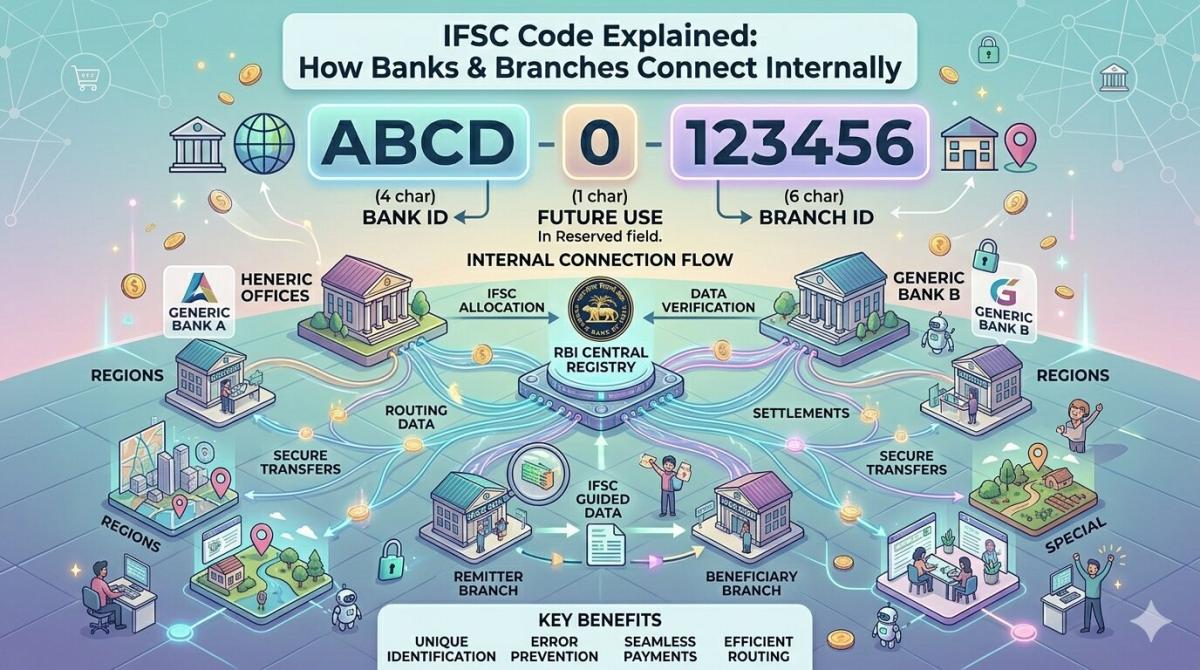

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

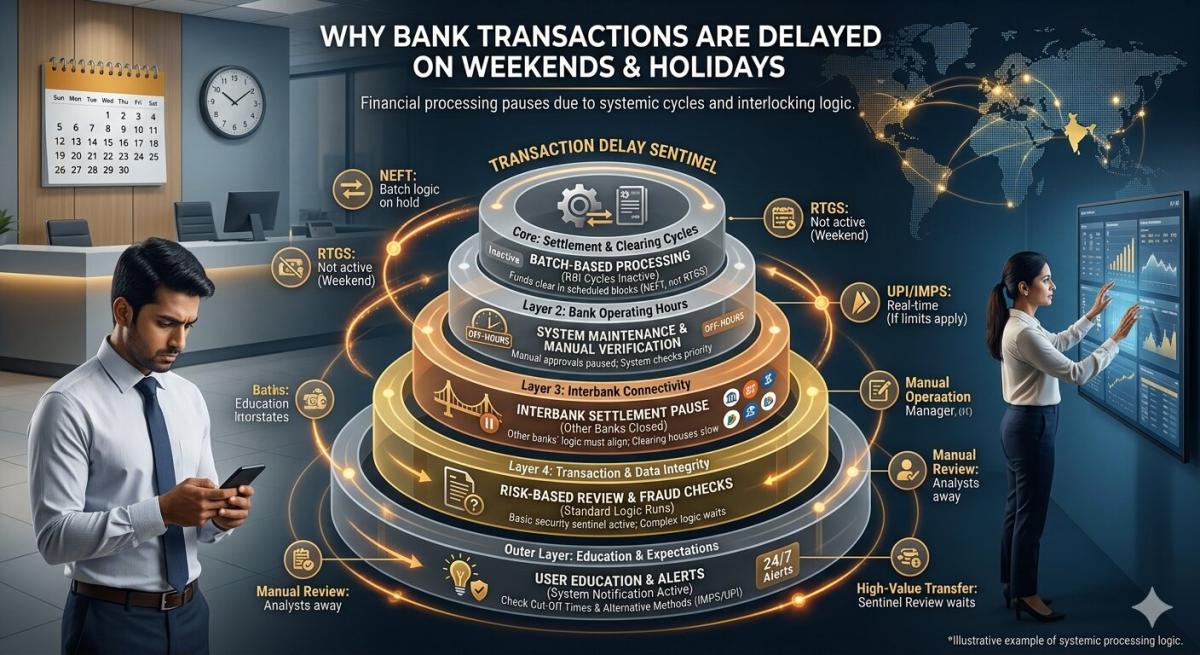

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ