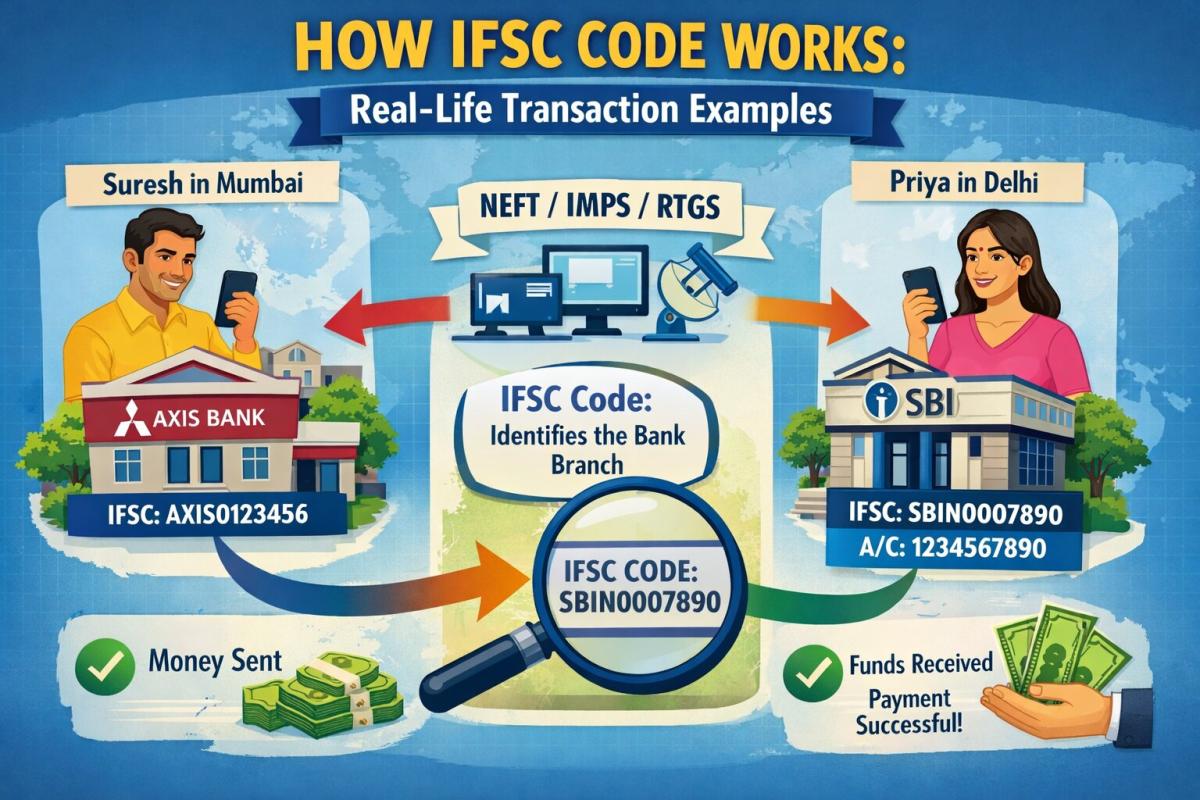

How IFSC Code Works: Real-Life Transaction Examples

See exactly how the IFSC code is used in real life—from receiving your salary to buying a car. Learn why this 11-digit code is the backbone of NEFT, RTGS, and SIPs.

Table of Contents

Have you ever stared at a bank transfer form, a little bead of sweat forming, wondering if you’ve got every digit right, especially that cryptic IFSC code? I certainly have. I vividly recall a time I was buying a used car, a significant sum for me back then, and the seller was in another city. The only way to transfer the down payment instantly was via NEFT. My heart pounded as I double-checked the “Real Life Example Of IFSC Code Usage In Transactions” on the form, knowing a single错could send my money into the void. Thankfully, I got it right, and the transaction sailed through, highlighting the silent but crucial role this code plays in our financial lives. It’s not just a string of characters; it’s the digital backbone ensuring your money reaches its precise destination, every single time.

Transferring Funds for a Large Purchase

One of the most common and critical real-life examples of IFSC code usage is when you need to transfer a substantial amount of money, such as for a property down payment, a vehicle purchase, or even a child’s college admission fee. These transactions often exceed daily UPI limits or require the immediate confirmation that RTGS (Real Time Gross Settlement) provides. Without the correct IFSC, your bank wouldn’t know which branch of the recipient’s bank to route the funds to, leading to delays, rejections, or even the dreaded “money stuck in limbo” scenario. It’s the digital postal code for banks, ensuring your funds are delivered to the right financial address.

Imagine purchasing a new apartment in mid-2026 and needing to transfer a significant token amount to the builder. You log into your net banking portal, enter the builder’s account number, and then comes the crucial step: inputting the IFSC. This 11-character alphanumeric code, unique to each bank branch, acts as a precise identifier. It ensures that your funds, perhaps several lakhs, don’t just go to the correct bank, but specifically to the correct branch where the builder holds their account. It’s a testament to the robust infrastructure that facilitates secure, high-value inter-bank transfers across India.

Receiving Your Salary or Freelance Payments

For millions, the IFSC code is implicitly used every month when their salary lands in their account. Employers, whether large corporations or small businesses, rely on your bank account details, including the IFSC, to initiate bulk salary disbursements. When you first join a company, one of the primary pieces of information they request is your bank account number and the associated IFSC. This allows their payroll system to accurately direct your earnings to your specific bank branch, regardless of which bank you use.

Freelancers and consultants also experience this regularly. When an international client pays you via a local payment gateway or a domestic client transfers funds directly, they will invariably ask for your bank details, including the IFSC. This ensures the money you’ve earned for your hard work reaches your specific account without any hitches. It’s a foundational piece of information that makes the financial engine of employment and independent work run smoothly, preventing the frustration of delayed or misdirected payments that can significantly impact one’s livelihood.

Managing Recurring Loan EMIs and Investments

The IFSC code plays a pivotal, often background, role in setting up and managing recurring financial commitments like Equated Monthly Installments (EMIs) for loans or Systematic Investment Plans (SIPs) for mutual funds. When you take out a home loan or car loan, the bank requires your IFSC to set up an Electronic Clearing Service (ECS) mandate or a National Automated Clearing House (NACH) mandate. These mandates automatically debit your account on specific dates, ensuring timely payments and avoiding penalties.

Similarly, for disciplined investors, SIPs are a popular way to build wealth. When you initiate an SIP, your investment platform or AMC will ask for your bank details, including the IFSC, to establish a recurring debit. This automation, powered by the IFSC, ensures your investments are made regularly without manual intervention. It’s a prime example of how this code facilitates long-term financial planning and stability, making sure your money moves exactly when and where it’s supposed to for your financial goals.

Understanding NACH Mandates

NACH (National Automated Clearing House) is a centralized system implemented by the National Payments Corporation of India (NPCI) that facilitates interbank, high-volume, electronic transactions that are repetitive in nature. The IFSC code is absolutely indispensable for setting up a NACH mandate. When you authorize a financial institution (like a bank or an asset management company) to debit your account periodically, your bank’s IFSC ensures that the mandate is correctly registered and executed against your specific branch. This system underpins countless automatic payments, from utility bills to insurance premiums, streamlining financial operations for both individuals and corporations.

Facilitating E-commerce Refunds and Merchant Payments

Online shopping has become ubiquitous, and with it, the need for efficient refund mechanisms. When you return a product purchased online, the e-commerce platform needs a way to send your money back to your bank account. While many platforms link directly to your payment method, for direct bank transfers or when a card isn’t available, providing your account number and IFSC is the standard procedure. This ensures the refund amount is credited directly and accurately to your original bank account, completing the transaction cycle.

Furthermore, businesses often make payments to their vendors or service providers via direct bank transfers. A small business owner paying for raw materials or a digital marketer settling an invoice with a content writer will use the recipient’s IFSC code to ensure the funds reach the correct business account. This streamlined process, underpinned by the IFSC, is crucial for maintaining healthy business relationships and ensuring smooth operational cash flow in today’s digital economy. It’s a critical component for the seamless functioning of online commerce and B2B financial interactions.

Business-to-Business (B2B) Transactions

In the corporate world, large-scale Business-to-Business (B2B) transactions are a daily occurrence, ranging from supplier payments to inter-company fund transfers. These often involve significant sums and require absolute precision. Companies routinely use NEFT and RTGS for these payments, and the IFSC code is the cornerstone of these systems. A manufacturing unit paying for a bulk order of components from a vendor in another state will rely on the vendor’s correct IFSC to ensure the payment is processed without error and on time.

Consider a scenario in 2026 where a large conglomerate needs to transfer dividends to its numerous shareholders or disburse funds to its subsidiaries across various cities. Each of these transactions, whether singular or batched, hinges on the accuracy of the recipient bank’s IFSC. This robust identification system prevents misdirection of critical business funds, which could otherwise lead to severe financial and operational disruptions. The IFSC code is an unsung hero in maintaining the intricate web of corporate finance, ensuring precision in every financial exchange. For more details on the operational aspects, the Reserve Bank of India website offers comprehensive information.

Key Takeaways

- The IFSC code is an 11-character alphanumeric identifier crucial for inter-bank electronic fund transfers within India, including NEFT, RTGS, and IMPS, ensuring funds reach the exact intended bank branch.

- It underpins a wide array of financial activities, from receiving salaries and making large personal purchases to setting up recurring payments for loans (EMIs) and investments (SIPs), simplifying complex financial movements.

- Accuracy is paramount when using an IFSC; even a single incorrect digit can lead to transaction failures, delays, or misdirection of funds, emphasizing the need for careful verification before initiating transfers.

- While often working behind the scenes in modern digital payment systems like UPI, the IFSC remains the foundational routing mechanism that enables these instantaneous and seamless transactions to occur between different banks.

Frequently Asked Questions

What does IFSC stand for?

IFSC stands for Indian Financial System Code. It is an 11-character alphanumeric code used to identify all bank branches participating in the electronic funds settlement systems in India. This unique code helps to accurately route transactions to the correct bank and branch.

Where can I find the IFSC code for a bank branch?

You can typically find the IFSC code printed on your bank passbook or cheque book. It is also readily available on your bank’s official website, through their mobile banking app, or by using online IFSC finders provided by financial portals. For example, you can often search for it on a bank’s official site like SBI’s branch locator.

What happens if I use an incorrect IFSC code?

If you use an incorrect IFSC code, the transaction will most likely fail and be reversed, with the funds returned to your account. However, in rare cases, if the incorrect IFSC code corresponds to another valid branch and the account number also matches a valid account in that branch, the funds could be debited from your account and credited to an unintended recipient. Always double-check the code.

Is the IFSC code required for all types of bank transactions?

The IFSC code is specifically required for electronic fund transfers between different banks and branches within India, such as NEFT, RTGS, and IMPS. For intra-bank transfers (transactions within the same bank), it may not always be explicitly required, as the bank’s internal system already knows its branches. UPI transactions often abstract the IFSC from the user, but it’s still used behind the scenes for routing.

Conclusion

The IFSC code, while seemingly a minor detail, is an indispensable cog in the vast machinery of India’s financial system. From ensuring your monthly salary reaches you punctually to facilitating multi-lakh property transactions, its role in enabling secure and precise electronic fund transfers cannot be overstated. Understanding its importance and ensuring its accuracy is key to smooth financial operations for individuals and businesses alike. As we move towards 2026, with increasing reliance on digital payments, the foundational integrity provided by the IFSC will only grow in significance, continuing to be the silent guardian of our money transfers.

Related Blogs

Published on Apr 09, 2026

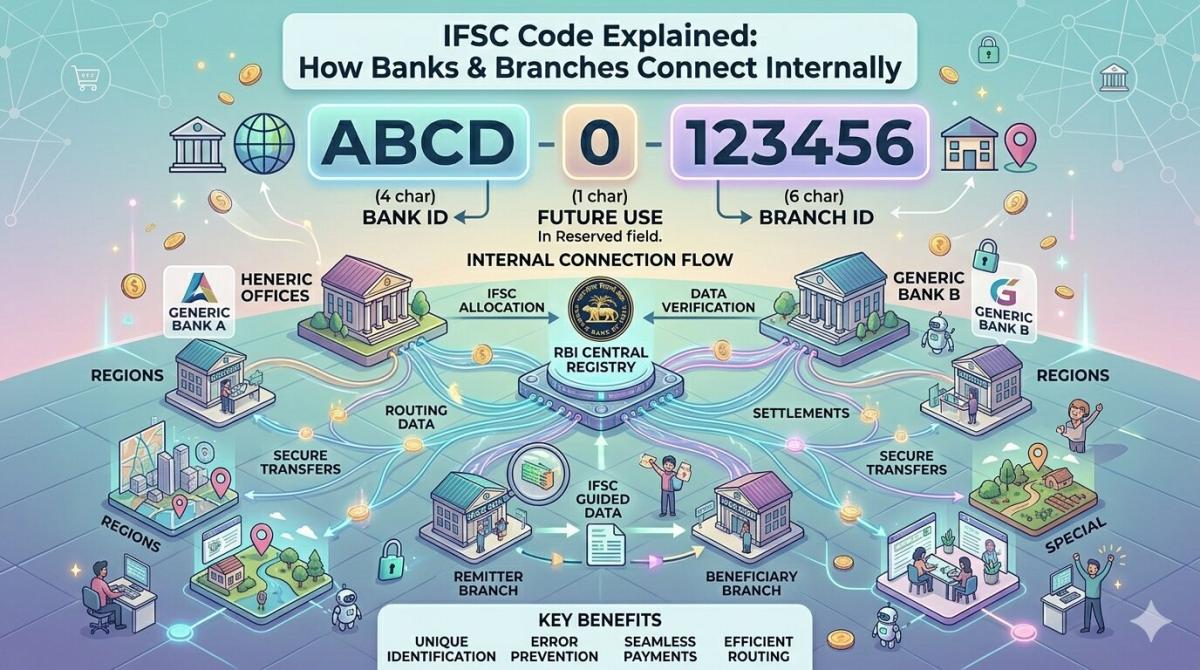

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

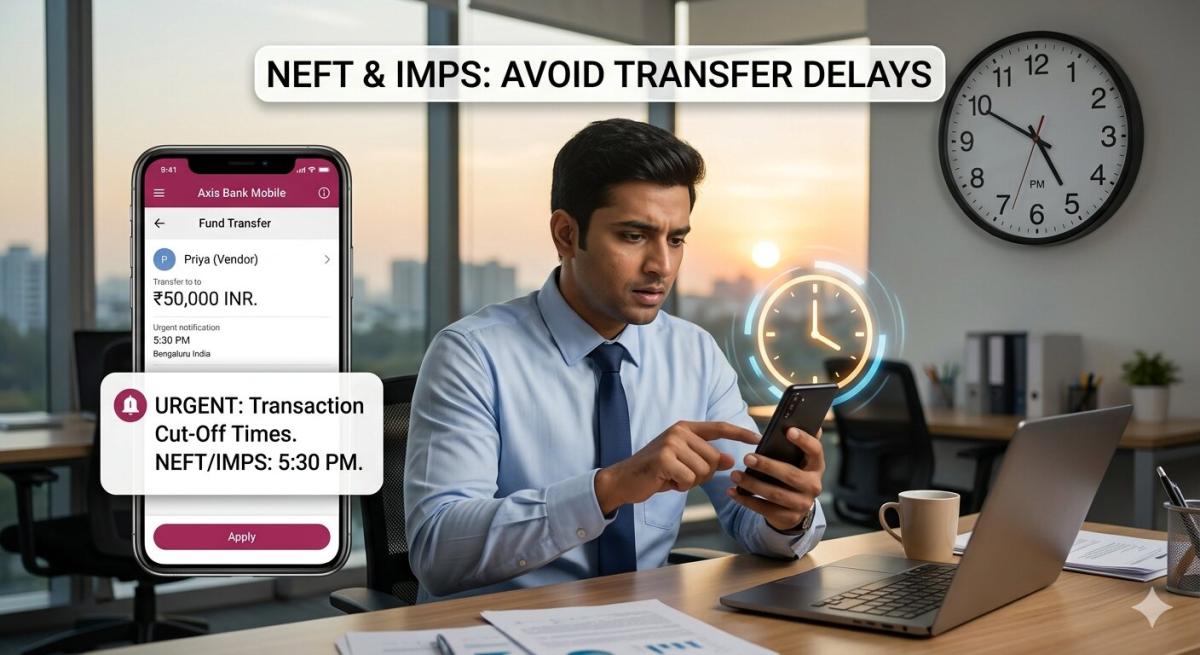

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

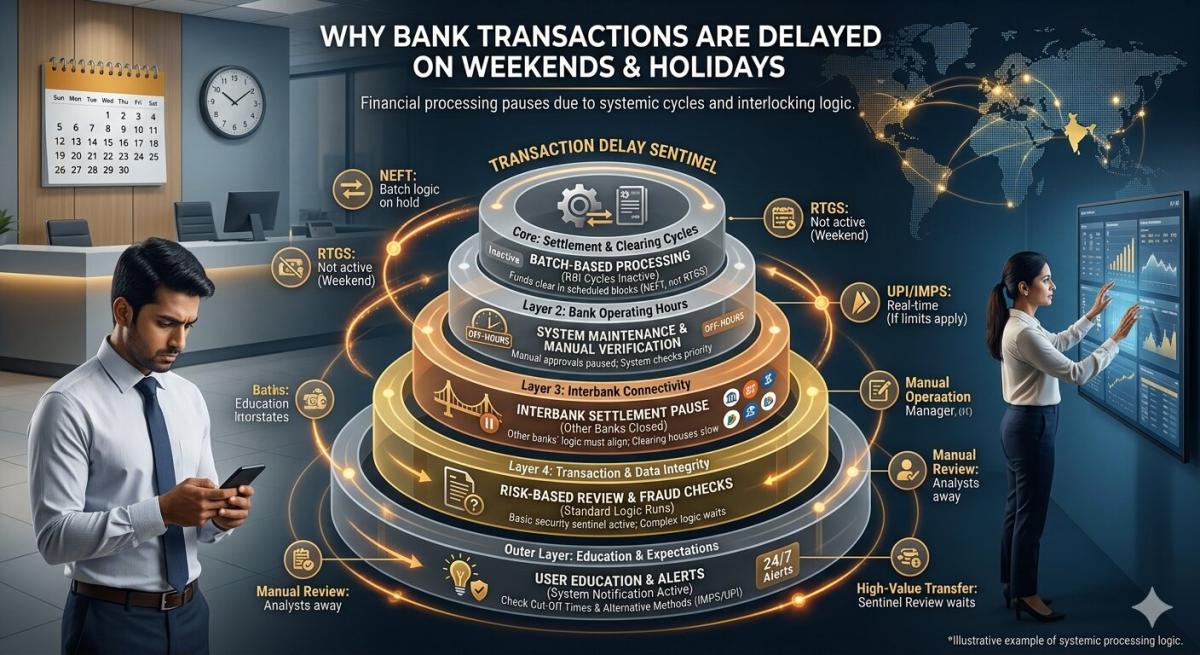

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ