How RBI Controls IFSC Code Allocation: The Regulatory Process Explained

Understand the RBI's role in IFSC code management. Learn about the allocation process, uniqueness checks, and the regulatory framework for Indian banks in 2026.

Table of Contents

Have you ever paused to consider the intricate machinery behind every seamless online bank transfer you make? It’s a fascinating world, often taken for granted. I recall a time years ago, setting up a new payment for a vendor, and mistakenly entering a single wrong digit in the IFSC. The transaction failed immediately, and I remember thinking how robust the system must be to catch such a minor error. This experience solidified my appreciation for the precision required in banking, and it’s precisely why understanding how RBI controls IFSC code allocation process is so crucial. It’s not merely an administrative task; it’s a foundational pillar ensuring the integrity and efficiency of India’s entire financial system.

Understanding the IFSC Code’s Significance

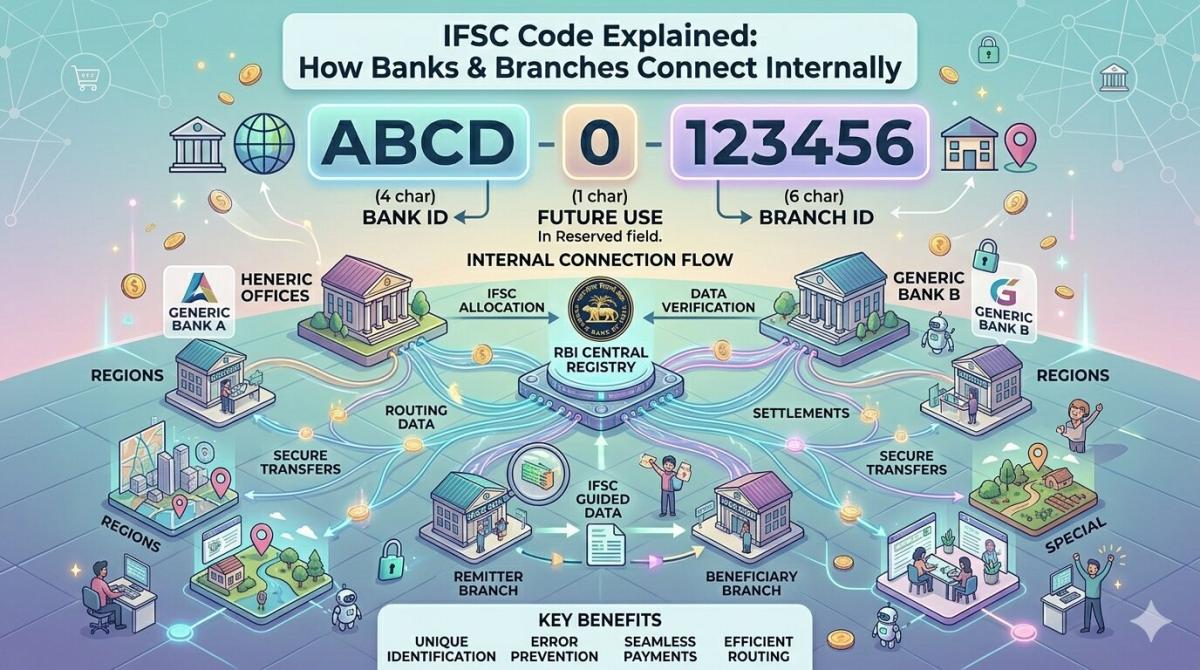

The Indian Financial System Code, or IFSC, is an 11-character alphanumeric code uniquely identifying every bank branch participating in online funds transfers. Think of it as the specific postal address for a digital transaction, guiding your money precisely to its intended destination. Without this unique identifier, processing transactions via NEFT (National Electronic Funds Transfer) or RTGS (Real Time Gross Settlement) would be chaotic, prone to errors, and significantly slower. Its structure is deliberate: the first four characters denote the bank, the fifth is always zero (reserved for future use), and the last six characters identify the specific branch.

The importance of the IFSC extends beyond mere identification; it’s a critical component in maintaining the security and reliability of India’s digital payment infrastructure. Every time you initiate a transaction, the banking system cross-references the IFSC to ensure the recipient’s bank and branch are correctly identified. This meticulous verification prevents misdirection of funds, reduces fraud risks, and instills confidence in users. It’s a testament to the foresight in designing a robust system, ensuring that even as digital transactions surge towards 2026, the underlying mechanisms remain dependable.

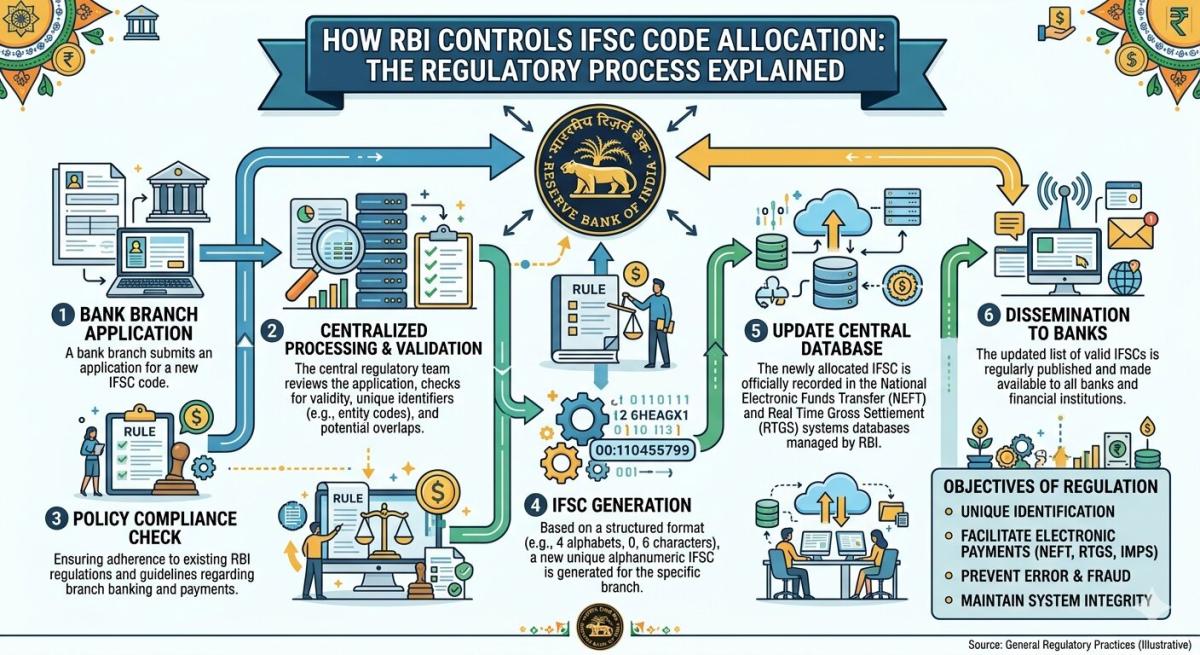

RBI’s Central Authority in Allocation

The Reserve Bank of India (RBI) stands as the ultimate authority overseeing the allocation and management of IFSC codes, a responsibility it takes with utmost seriousness. As the nation’s central banking institution, the RBI is tasked with regulating the banking sector, ensuring financial stability, and promoting the efficient functioning of payment systems. This broad mandate naturally extends to controlling critical identifiers like the IFSC, which are indispensable for the secure and orderly flow of money across the country. Their direct involvement ensures standardization and prevents any potential fragmentation or inconsistencies.

The RBI’s control isn’t just about assigning codes; it’s about maintaining the integrity and exclusivity of each one. They act as the central repository and administrator, ensuring that no two branches, regardless of the bank, ever share the same IFSC. This centralized approach eliminates ambiguity and fosters a uniform system across all participating financial institutions. It’s a crucial aspect of their regulatory framework, preventing operational bottlenecks and safeguarding consumers from potential financial losses due to erroneous transfers.

The Meticulous Allocation Process

When a bank decides to open a new branch, the process to obtain an IFSC code is far from trivial; it involves a rigorous application and verification procedure directly with the RBI. Banks must submit detailed proposals including the branch’s physical address, operational details, and justification for its establishment. This isn’t just about paperwork; it’s about ensuring that every new point of financial service integration meets the necessary regulatory standards and contributes positively to the banking network. The RBI scrutinizes these applications to ensure compliance and viability.

Upon receiving an application, the RBI undertakes a thorough review, cross-referencing existing data to confirm the uniqueness of the proposed branch and its location. Once approved, a unique 11-character IFSC is systematically generated and assigned. This process is designed to be foolproof, integrating the new branch seamlessly into the national electronic funds transfer network. It underscores the RBI’s commitment to maintaining an uncluttered and highly efficient system, a principle that will continue to guide their efforts well into 2026 and beyond.

Ensuring Uniqueness and Preventing Duplication

The absolute uniqueness of each IFSC is paramount, and the RBI employs sophisticated internal systems to guarantee this. Their robust database acts as the single source of truth, meticulously tracking every allocated code. Before assigning a new IFSC, the system performs comprehensive checks to ensure there are no existing codes that could even remotely cause confusion or duplication. This level of diligence is critical because even a single duplicated or incorrectly assigned IFSC could lead to significant operational disruptions and financial mishaps, undermining public trust in the banking system.

Dynamic Management and Updates

The financial landscape is ever-evolving, with banks frequently undergoing mergers, acquisitions, branch relocations, or closures. Each of these changes necessitates an update to the corresponding IFSC codes, and the RBI diligently manages this dynamic environment. When a branch closes, its IFSC is typically deactivated; if it relocates, a new code might be issued, or the existing one updated with new details. Mergers often lead to consolidation, requiring careful mapping of old IFSCs to new ones. This continuous oversight ensures the accuracy of the entire system.

To keep the public and banking institutions informed, the RBI regularly publishes updated lists of IFSC codes. These lists are crucial for banks to ensure their internal systems are current, and for customers to verify details when initiating transactions. This transparency and proactive dissemination of information are hallmarks of the RBI’s governance. It allows the ecosystem to adapt smoothly to changes, demonstrating a forward-thinking approach to financial infrastructure management. You can often find these updated lists on official banking portals or the RBI’s own website for reference.

Impact on Digital Banking and Future Trends

The RBI’s stringent control over the IFSC allocation process has been instrumental in fostering the rapid growth and widespread adoption of digital banking in India. By ensuring a reliable and unambiguous system for identifying bank branches, the RBI has laid a solid foundation for secure electronic transactions. This meticulous management directly contributes to the trust users place in platforms like UPI, NEFT, and RTGS, which are the backbone of India’s digital economy. Without this foundational reliability, the leap towards a cashless society would be fraught with significantly more challenges and hesitancy.

Looking ahead, the role of the RBI in managing these critical identifiers will only become more significant. As financial technology evolves, with innovations like Open Banking and blockchain-based payment systems on the horizon, the underlying mechanisms for identifying and routing funds will need to be adaptable yet robust. The RBI is continuously evaluating these trends, ensuring that the existing framework, including the IFSC system, can either evolve or seamlessly integrate with future advancements. We can expect their oversight to ensure that India’s financial infrastructure remains cutting-edge and secure, potentially even introducing new identifier standards or enhancements by 2026 to complement the existing IFSC framework, as the digital payments landscape continues its rapid expansion globally.

Key Takeaways

- Centralized Control is Paramount: The RBI’s direct oversight of IFSC allocation is crucial for standardizing India’s financial system, preventing inconsistencies, and maintaining the integrity of electronic fund transfers like NEFT and RTGS.

- Ensuring Uniqueness Prevents Errors: Each 11-character IFSC is meticulously assigned to guarantee absolute uniqueness, eliminating ambiguity and significantly reducing the risk of misdirected funds or fraudulent transactions.

- Dynamic Management for a Changing Landscape: The RBI actively manages IFSC codes in response to branch closures, mergers, and new openings, publishing regular updates to ensure the accuracy and reliability of the entire banking network.

- Foundation for Digital Banking Trust: The robust and reliable IFSC system, managed by the RBI, underpins the confidence in India’s digital payment ecosystem, facilitating the widespread adoption of online transactions and contributing to financial inclusion.

Frequently Asked Questions

What is an IFSC code and why is it important?

An IFSC (Indian Financial System Code) is an 11-character alphanumeric code that uniquely identifies every bank branch in India participating in online money transfers. It’s crucial because it ensures your funds are accurately routed to the correct recipient bank and branch during NEFT, RTGS, and IMPS transactions, preventing errors and ensuring security.

How does RBI ensure the uniqueness of each IFSC code?

The RBI maintains a central, sophisticated database of all allocated IFSC codes. When a new branch applies for an IFSC, the RBI’s system performs rigorous checks to confirm that the proposed code or any similar variation does not already exist, thereby guaranteeing the absolute uniqueness of each assigned identifier across the entire banking network.

What happens to an IFSC code if a bank branch closes or merges?

If a bank branch closes, its IFSC code is typically deactivated to prevent further usage. In the event of a merger or acquisition, the RBI oversees the consolidation process, which may involve deactivating old IFSCs and assigning new ones, or mapping old codes to the new entity’s structure, always ensuring continuity and clarity for users.

Can an individual or a business apply for an IFSC code?

No, individuals or businesses cannot directly apply for an IFSC code. Only banks, when establishing a new branch, can apply to the Reserve Bank of India for the allocation of a unique IFSC. The codes are assigned to bank branches, not to individual accounts or entities.

Conclusion

The RBI’s meticulous control over the IFSC code allocation process is far more than an administrative detail; it is a foundational pillar supporting the vast and complex edifice of India’s digital financial system. It ensures that every electronic transaction, from a small personal transfer to a large corporate payment, reaches its intended destination with precision and security. This unwavering commitment to standardization and oversight by the RBI instills vital confidence in millions of users and will remain paramount as India continues its journey towards an even more interconnected and digitally advanced economy by 2026 and beyond. It truly is the silent guardian of our digital money flows.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ