Decoding Your IFSC Code: Meaning of Each Digit Explained Clearly

What does each digit of an IFSC mean? Learn the 4-1-6 structure, the secret of the "Control Zero," and see real-bank examples for SBI, HDFC, and more.

Table of Contents

Have you ever initiated a bank transfer, perhaps for an urgent bill payment or sending money to a loved one, and felt that slight pang of anxiety as you double-checked the account number and the IFSC code? I certainly have. Years ago, a small typo in an IFSC almost sent a critical payment into the digital abyss, only to be recovered after a frantic call to the bank. That experience cemented my understanding that while an IFSC code might seem like just another string of characters, it is, in fact, the digital backbone of secure and accurate financial transactions within India. Understanding the meaning of each digit in an IFSC code isn’t just for banking professionals; it’s a fundamental aspect of modern financial literacy that empowers you to transact with confidence and precision.

Decoding the Indian Financial System Code

The Indian Financial System Code, universally known as IFSC, is an 11-character alphanumeric code that uniquely identifies every bank branch participating in online money transfers across India. This distinctive code is indispensable for various electronic payment systems, including NEFT (National Electronic Funds Transfer), RTGS (Real Time Gross Settlement), and IMPS (Immediate Payment Service). Without a correct IFSC, your funds simply cannot reach their intended destination, making it a critical piece of information for anyone engaging in digital banking. It’s akin to a digital postal code for your bank branch, ensuring that money navigates the vast network of Indian banks efficiently and without error.

Conceived by the Reserve Bank of India (RBI) to streamline inter-bank transactions, the IFSC acts as a digital signpost, guiding funds to the precise branch where the recipient’s account is held. This standardized system eliminates ambiguity and significantly reduces the chances of misdirected payments, a common concern in the past. Its structured format, which we’ll delve into shortly, is designed for both clarity and future scalability, ensuring that as the Indian banking sector grows, the IFSC remains robust and effective. For consumers and businesses alike, knowing how to locate and verify an IFSC is a fundamental skill in today’s digital-first economy.

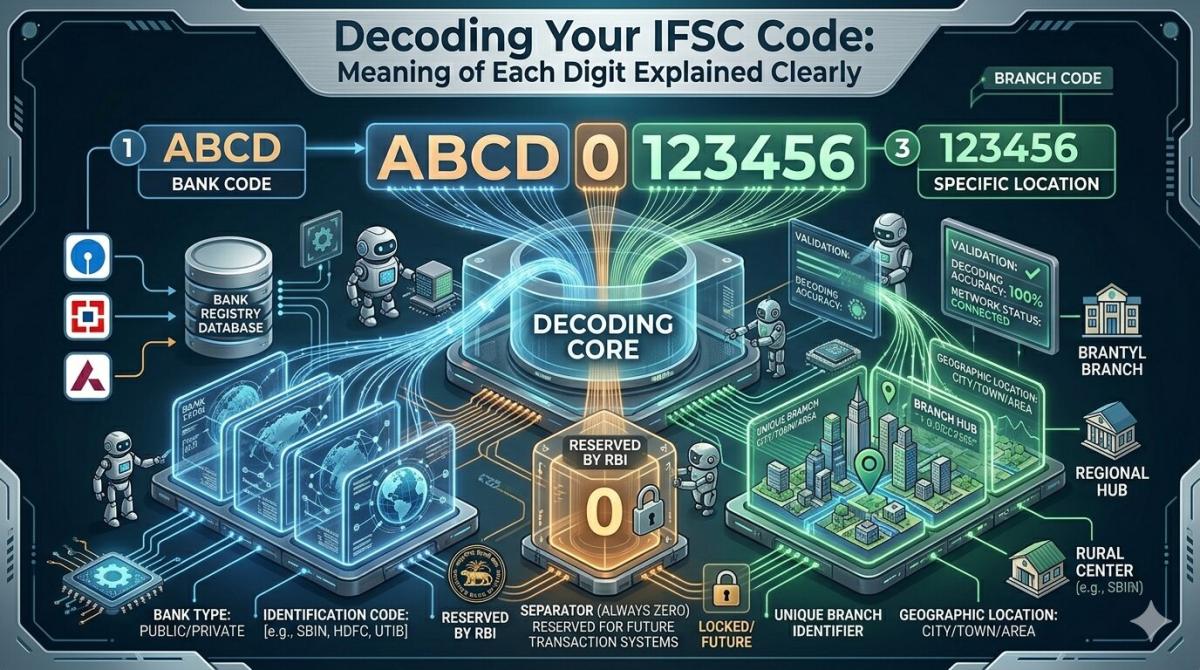

The First Four Characters: Bank Identification

The journey into understanding the IFSC code begins with its initial four characters, which are always alphabetic. These characters serve a singular, crucial purpose: to identify the specific bank involved in the transaction. For example, ‘ICIC’ signifies ICICI Bank, ‘SBIN’ denotes State Bank of India, and ‘HDFC’ naturally points to HDFC Bank. This standardization ensures that no matter which branch you’re dealing with, the overarching financial institution is immediately recognizable, forming the primary layer of identification within the code. It’s a simple yet highly effective method to categorize India’s myriad banking entities.

This initial segment is particularly vital because it quickly directs the payment gateway to the correct banking network. Imagine the complexity if every single branch had a completely random code; the system would be unmanageable. By grouping branches under a common bank identifier, the RBI has created an intuitive and logical framework that enhances processing speed and reduces computational overhead. This design choice highlights a pragmatic approach to managing a massive financial infrastructure, ensuring that even as new banks emerge or existing ones expand by 2026, the foundational identification remains consistent and easily processable.

The Fifth Character: The Control Digit

Moving past the bank identifier, we encounter the fifth character of the IFSC code, which is invariably the digit ‘0’ (zero). This specific placement and fixed value often raise questions among those looking at the code for the first time. Far from being a random inclusion or an oversight, this ‘0’ serves as a crucial control character. Its primary role is as a placeholder, designed to facilitate future expansion and adaptability of the IFSC system. Should the need arise, for instance, to introduce new sub-categories within banks or implement additional layers of identification, this digit can be reassigned to carry new information without disrupting the entire existing framework.

A Forward-Thinking Design Choice

This forward-thinking design choice by the RBI underscores a deep understanding of evolving financial landscapes. By reserving a digit for potential future use, the system builds in flexibility, allowing for modifications and enhancements without requiring a complete overhaul of the existing IFSC structure. It’s a testament to robust planning, ensuring the longevity and scalability of India’s electronic payment infrastructure. This foresight guarantees that the IFSC system can accommodate growth and innovation, remaining relevant and efficient well into the future, perhaps even beyond 2026, as the digital transformation of banking continues its rapid pace.

The Last Six Characters: Branch Identification

The final six characters of the IFSC code are numeric and hold the critical responsibility of uniquely identifying the specific bank branch. Once the initial four characters point to the bank and the fifth character holds its place, these last six digits precisely pinpoint the exact physical location where the recipient’s account is domiciled. This level of granularity is paramount for ensuring that funds are credited to the correct branch, even if a bank has hundreds or thousands of branches spread across the country. Each branch, regardless of its size or location, possesses its own distinct six-digit identifier.

This detailed branch identification is what truly makes the IFSC an indispensable tool for accurate electronic fund transfers. Without this specificity, money could easily be misdirected to another branch of the same bank, leading to delays and complications for both the sender and the receiver. The uniqueness of these six digits ensures that once the bank is identified, the payment system can navigate directly to the correct branch, completing the transaction seamlessly. It’s this combination of bank and branch specificity that underpins the reliability of India’s digital payment ecosystem, making transfers both fast and secure.

Why IFSC Codes Matter for Seamless Transactions

Beyond merely understanding its structure, appreciating the functional significance of the IFSC code is crucial for anyone navigating the modern financial world. The IFSC is not just a regulatory requirement; it’s the bedrock upon which the entire edifice of electronic fund transfers within India stands. It acts as an error-prevention mechanism, ensuring that millions of transactions processed daily through NEFT, RTGS, and IMPS reach their intended beneficiaries without a hitch. This meticulous identification system dramatically reduces the possibility of funds being stuck in limbo or erroneously credited, which can have significant financial and emotional repercussions for individuals and businesses alike.

Moreover, the IFSC code facilitates the incredible speed and efficiency we’ve come to expect from digital payments. Imagine manually verifying each bank and branch for every transaction; it would be an impossible task. The standardized and machine-readable nature of the IFSC allows automated systems to process large volumes of transfers rapidly, often within seconds or minutes. This efficiency supports India’s burgeoning digital economy, enabling quick payments for e-commerce, bill settlements, and peer-to-peer transfers, all while maintaining a high degree of security and accuracy. For more details on payment systems, you can always refer to the Reserve Bank of India website.

Key Takeaways

- The IFSC is an 11-character alphanumeric code essential for online money transfers within India, uniquely identifying each bank branch.

- Its structure consists of the first four alphabetic characters for the bank name (e.g., ‘SBIN’), a fifth ‘0’ (zero) as a control character for future expansion, and the final six numeric characters for the specific branch identification.

- Understanding the IFSC code is vital for ensuring accurate, secure, and timely electronic fund transfers via NEFT, RTGS, and IMPS, preventing misdirected payments.

- The system is designed for scalability and robustness, with the ‘0’ placeholder allowing for future adaptations to the evolving financial landscape, ensuring its relevance even in 2026 and beyond.

Frequently Asked Questions

Can an IFSC code change for a bank branch?

While relatively rare, an IFSC code can indeed change, typically if a bank merges with another, a branch relocates, or undergoes a significant restructuring. Banks usually provide ample notice to their customers in such scenarios. It’s always a good practice to verify the IFSC, especially for recurring payments, if you hear about any changes affecting your bank or branch.

Is the IFSC code different from the SWIFT code?

Yes, the IFSC code and SWIFT code serve different purposes. The IFSC (Indian Financial System Code) is used exclusively for domestic money transfers within India. The SWIFT (Society for Worldwide Interbank Financial Telecommunication) code, also known as BIC (Bank Identifier Code), is an international standard used for cross-border transactions to identify banks globally. They are not interchangeable.

Where can I find the correct IFSC code for a branch?

You can reliably find the correct IFSC code on your bank’s chequebook, passbook, or account statements. Most banks also provide an IFSC search tool on their official websites. Additionally, the National Payments Corporation of India (NPCI) and the RBI websites often have directories or tools to verify IFSC codes.

What happens if I use an incorrect IFSC code?

If you use an incorrect IFSC code, the transaction will most likely fail immediately, and the funds will be returned to your account. In some rare cases, if the incorrect IFSC matches another valid bank and branch, the funds might be credited to a wrong account, leading to complications and a potentially lengthy reversal process. Always double-check before confirming a transfer.

Conclusion

The IFSC code, though seemingly a mundane detail, is a sophisticated and indispensable component of India’s financial infrastructure. Its 11 characters, meticulously designed to identify the bank, accommodate future growth, and pinpoint the exact branch, are the unsung heroes of countless daily transactions. Understanding the meaning of each digit in an IFSC code empowers you with the knowledge to conduct your financial affairs with greater confidence and accuracy. As we move towards an increasingly digital economy, mastering these fundamental concepts ensures your money always finds its way home, swiftly and securely.

Related Blogs

Published on Apr 09, 2026

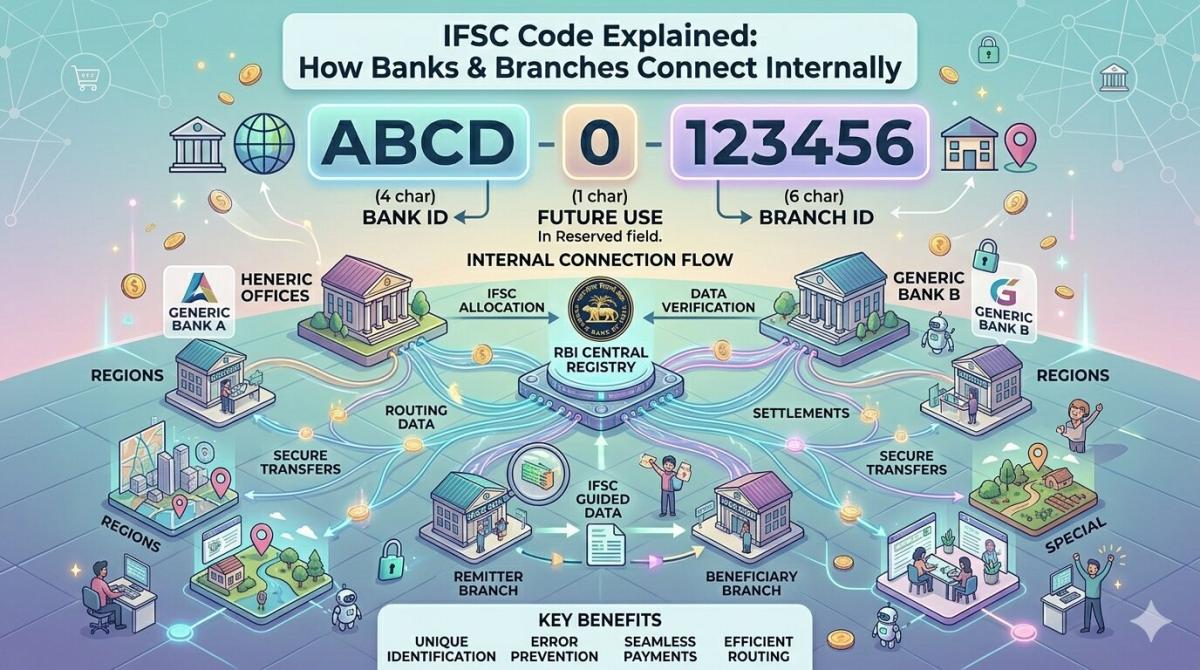

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

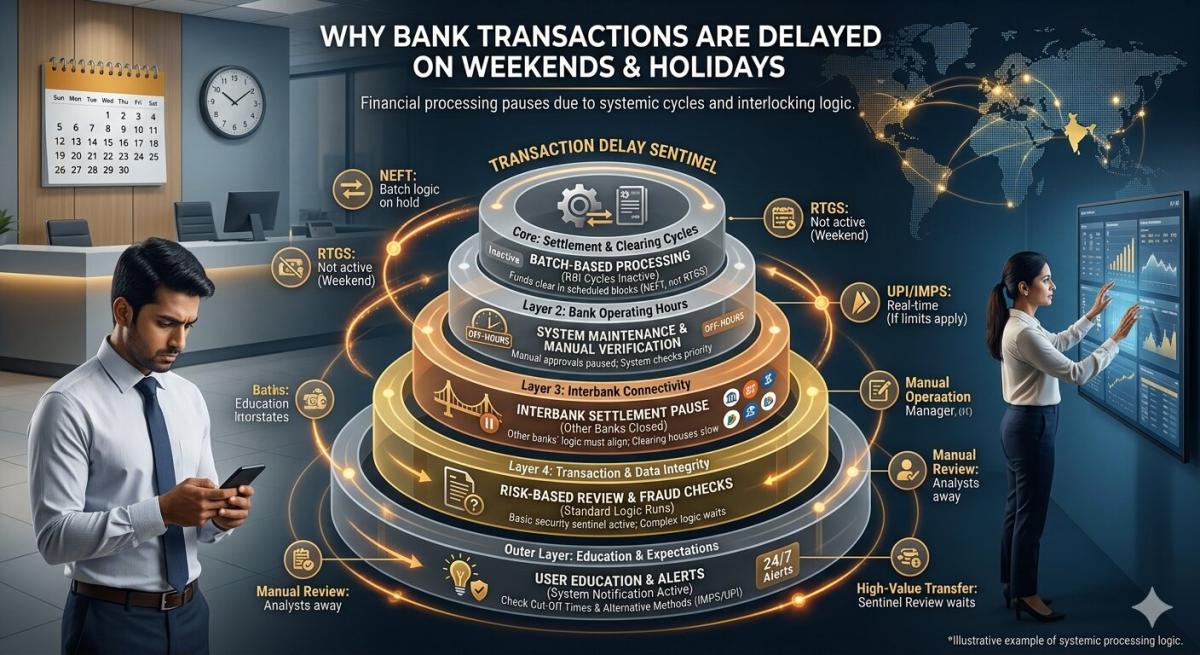

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ