IFSC Code Structure Explained: Breakdown & Real Bank Examples

What do the 11 characters in an IFSC mean? Learn the technical breakdown of bank codes, the "zero" rule, and real examples for SBI, HDFC, and ICICI in 2026.

Table of Contents

Have you ever stared at a bank transfer form, meticulously typing in a string of 11 characters, wondering what arcane magic held them together? I certainly have. Years ago, a minor typo almost sent a critical payment into the ether, teaching me a valuable lesson about the precision required in modern banking. Understanding the IFSC Code Structure Breakdown With Example Bank Codes isn’t just about avoiding costly errors; it’s about appreciating the intricate system that underpins India’s vast financial network, ensuring billions of rupees flow smoothly and securely every single day. Let’s demystify this essential banking tool together.

What Exactly is an IFSC Code?

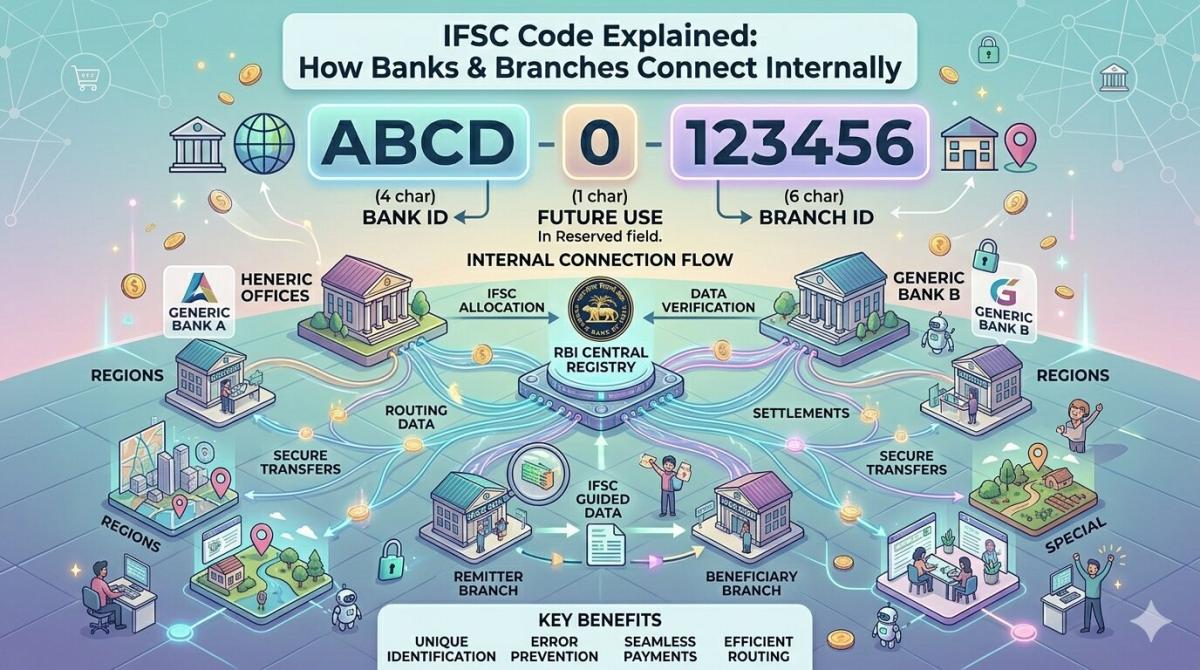

The Indian Financial System Code, or IFSC, is a unique 11-character alphanumeric code assigned by the Reserve Bank of India (RBI) to identify every bank branch participating in online money transfers. It’s the digital fingerprint for a specific branch, essential for facilitating electronic funds transfers such as NEFT (National Electronic Funds Transfer), RTGS (Real Time Gross Settlement), and IMPS (Immediate Payment Service). Without a correct IFSC, your funds simply cannot reach their intended destination within India.

Think of the IFSC as the postal code for a bank branch in the digital realm. Its primary purpose is to ensure that when you initiate a transfer, the money goes to the exact branch of the beneficiary’s bank, not just the right bank. This precision is paramount in preventing misdirected funds and ensuring transaction security. The integrity of India’s financial system, particularly for digital payments, heavily relies on the unique and accurate identification provided by these codes, which will only grow in importance by 2026.

Decoding the 11 Alphanumeric Characters

At first glance, an IFSC code might seem like a random assortment of letters and numbers, but it’s far from it. Each of the 11 characters holds a specific meaning and plays a crucial role in directing your funds. The structure is meticulously designed to provide a hierarchical identification, starting from the bank itself and narrowing down to a specific branch. It’s a testament to thoughtful system design.

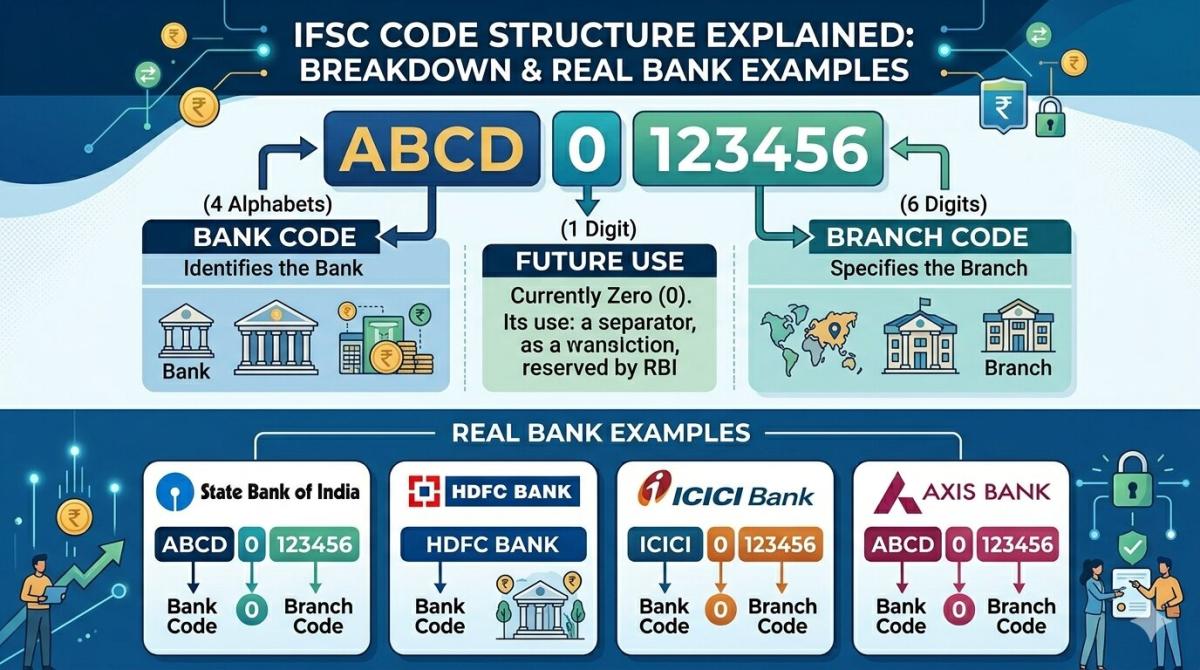

The 11 characters are divided into three distinct parts: the first four characters identify the bank, the fifth character is always a ‘0’ for future use and control, and the final six characters identify the specific branch. This standardized format ensures consistency across all participating banks and streamlines the processing of millions of transactions daily, making the system incredibly robust and efficient for users nationwide.

The First Four Characters: Bank Identifier

The initial four characters of any IFSC code are dedicated to identifying the bank itself. These characters are unique to each financial institution operating in India, providing an immediate identifier for the bank involved in the transaction. For instance, “HDFC” signifies HDFC Bank, “SBIN” points to State Bank of India, and “ICIC” refers to ICICI Bank. This segment is standardized by the RBI, ensuring no two banks share the same four-character identifier.

This standardization is a cornerstone of the IFSC system’s efficiency. When you see “KOTK” or “AXIS” at the beginning of an IFSC, you instantly know which bank is being referred to, regardless of the branch. This simplifies the initial routing of funds within the vast interbank network, acting as the first crucial filter in the electronic transfer process. It’s a remarkably intuitive way to categorize hundreds of banks.

The Fifth Character: The Control Zero

The fifth character in every IFSC code is always a ‘0’ (zero). This character serves a specific, though often overlooked, purpose. Primarily, it’s reserved for future use, allowing for potential expansion or modifications to the IFSC structure without disrupting the existing system. It acts as a placeholder, ensuring flexibility in the long-term evolution of India’s financial identification framework.

Beyond futureproofing, this ‘0’ also acts as a control character, differentiating the bank code from the branch code. Its fixed nature provides a clear demarcation point within the 11-character string, making parsing and validation of the code simpler for automated banking systems. It’s a subtle but vital component that underscores the meticulous planning behind the IFSC system.

The Last Six Characters: The Branch Code

Following the control zero, the final six characters of the IFSC code are dedicated to identifying the specific branch of the bank. This segment is alphanumeric and uniquely pinpoints the exact branch where the beneficiary holds an account. For example, while “HDFC” identifies HDFC Bank, the subsequent six characters like “0000001” or “0000123” differentiate between thousands of HDFC branches across the country.

This level of granularity is what makes the IFSC system so powerful and precise. Without these unique branch identifiers, funds could easily be misdirected to the wrong branch of the correct bank, causing significant delays and complications. It’s this precise targeting that enables seamless and error-free electronic transfers, giving users confidence that their money will arrive exactly where it’s intended. You can verify IFSC codes on official bank websites or through the Reserve Bank of India’s portal for added assurance.

Real-World IFSC Code Examples and Usage

Let’s look at some practical examples to solidify our understanding of the IFSC Code Structure Breakdown With Example Bank Codes. Consider “HDFC0000001”. Here, “HDFC” is HDFC Bank, the ‘0’ is the control character, and “0000001” represents a specific HDFC branch (often the first or main branch in a city, like Fort Branch, Mumbai). Another example, “SBIN0000001”, identifies the State Bank of India’s Parliament Street branch in New Delhi. Each component plays its part in making these codes work.

These codes are indispensable for virtually all electronic banking transactions in India. Whether you’re sending money to a family member via IMPS, paying a vendor through NEFT, or settling a large business transaction with RTGS, the correct IFSC code is paramount. Always double-check the IFSC code on your beneficiary’s cheque book, passbook, or through official bank channels to ensure accuracy. Reliable financial portals like BankBazaar’s IFSC search tool can also be helpful for verification.

Key Takeaways

- The IFSC (Indian Financial System Code) is an 11-character alphanumeric code crucial for all electronic fund transfers within India.

- Its structure comprises a 4-character bank identifier, a fixed ‘0’ for control and future use, and a 6-character unique branch identifier.

- Accuracy is paramount: an incorrect IFSC code can lead to transaction failure or, in rare cases, misdirection of funds to an unintended account.

- Understanding the breakdown of an IFSC code empowers users to verify details and ensures secure, efficient financial transactions in the modern banking landscape of 2026.

Frequently Asked Questions

Can an IFSC code change?

While generally stable, an IFSC code can change due to specific circumstances like bank mergers, branch relocation, or a bank undergoing a rebranding exercise. In such scenarios, the bank typically notifies its customers, and new codes are updated in official records, so it’s wise to verify for critical transactions.

Is IFSC required for international transfers?

No, the IFSC code is exclusively for domestic electronic fund transfers within India. For international money transfers, a different code called the SWIFT (Society for Worldwide Interbank Financial Telecommunication) code, also known as BIC (Bank Identifier Code), is required to identify the receiving bank globally.

How do I find my bank’s IFSC code?

You can easily find your bank’s IFSC code on your cheque book, bank passbook, or bank statement. Most banks also prominently display their branch IFSC codes on their official websites, mobile banking apps, and through their customer service channels. Reliable third-party financial aggregators also list these codes.

What happens if I use a wrong IFSC code?

If you enter an incorrect IFSC code, the most common outcome is that the transaction will fail, and your bank will notify you. The funds typically remain in your account. However, in rare instances where the incorrect IFSC code happens to match another valid branch and the account number also matches, funds could potentially be transferred to the wrong beneficiary, highlighting the need for vigilance.

Conclusion

The IFSC code is far more than just a random string of characters; it’s the meticulous backbone of India’s digital financial transactions. Understanding its structure – the bank identifier, the control zero, and the unique branch code – empowers you to navigate electronic payments with confidence and precision. As India’s digital economy continues its rapid expansion towards 2026, the importance of these 11 characters will only grow, underscoring the value of knowing exactly how your money finds its way home. Stay informed, stay secure.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ