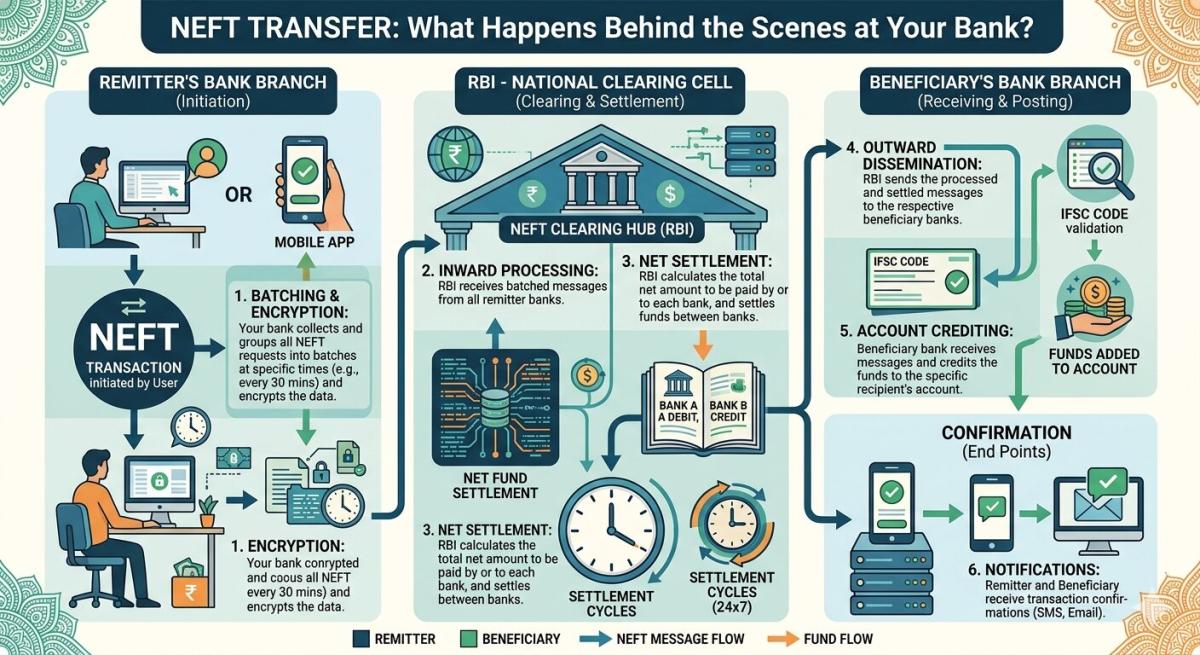

NEFT Transfer: What Happens Behind the Scenes at Your Bank?

Ever wondered how NEFT works? Follow the journey of your money from the originating bank to RBI clearing and beneficiary credit in our 2026 guide.

Table of Contents

- The Initial Handshake: Your Bank’s Role

- Journey Through the NEFT Clearing System

- Understanding Batch Processing Nuances

- The Beneficiary Bank’s Reception and Credit

- Behind the Scenes: Security and Reconciliation

- Why NEFT Remains a Pillar of Digital Payments

- Key Takeaways

- Frequently Asked Questions

- Conclusion

Have you ever hit ‘send’ on an NEFT transfer and wondered, as I often have, what exactly happens inside the bank after NEFT transfer initiation? It’s a question that plagued me years ago when a crucial payment seemed to vanish into the digital ether for hours. I remember feeling a mix of anxiety and curiosity, realizing there was a complex, hidden ballet of data and funds orchestrated behind the scenes. We often take the seamlessness of digital transactions for granted, but beneath that user-friendly interface lies a robust, multi-layered system designed for security and efficiency. Let’s pull back the curtain and explore the fascinating journey your money takes.

The Initial Handshake: Your Bank’s Role

When you initiate an NEFT (National Electronic Funds Transfer) request, your bank, the ‘originating bank’ or ‘remitter bank,’ springs into action. The first step involves a series of internal checks. Your account balance is verified to ensure sufficient funds are available, and the beneficiary details you’ve provided, such as account number and IFSC code, are validated for format and basic correctness. This critical initial screening prevents transfers from failing later in the process due to insufficient balance or malformed data, saving time and reducing friction for everyone involved.

Once these preliminary checks are passed, your account is debited, and the transaction details are securely packaged. This package isn’t sent directly to the beneficiary’s bank. Instead, it’s routed to a central NEFT clearing system managed by the Reserve Bank of India (RBI). Think of it as your bank preparing a meticulously labeled parcel, ready for a highly organized postal service. The internal systems create an audit trail, assigning a unique transaction reference number that allows you and the bank to track its progress, offering a crucial layer of transparency.

Journey Through the NEFT Clearing System

The NEFT clearing system is the heart of the entire operation, acting as a crucial intermediary between thousands of banks across India. Your bank’s packaged request joins a stream of other NEFT transactions from various banks. The RBI’s system doesn’t process each transaction individually in real-time; instead, it operates on a batch processing model. Throughout the day, at specified intervals, these collected transactions are bundled together into batches. This method, while not instant, is incredibly efficient for handling the sheer volume of daily transfers.

Within these batches, the RBI system performs the interbank settlement. It calculates the net amount owed by each remitting bank to each beneficiary bank and vice versa. This netting process significantly reduces the number of individual transfers that need to occur between banks, streamlining the entire financial movement. Once the settlement is complete, the RBI’s system then dispatches the relevant transaction details to the respective beneficiary banks, essentially telling them, “Funds are available; please credit your customer.”

Understanding Batch Processing Nuances

Batch processing is a cornerstone of NEFT’s design, influencing why funds aren’t credited instantaneously. The RBI facilitates these settlements in half-hourly batches, 24 hours a day, 7 days a week, including holidays, a significant enhancement introduced in 2019. This means that if you initiate a transfer, it will be picked up in the next available batch. The beauty of this system lies in its ability to manage massive transaction volumes reliably and cost-effectively, ensuring that even in 2026, it remains a robust payment rail for countless transactions daily.

This systematic approach, while seemingly less “real-time” than some newer payment methods, provides a predictable and secure framework. Banks have specific windows to submit and receive these batches, allowing their internal systems to process them in an organized manner. It’s a testament to good engineering, balancing speed with the utmost financial integrity, which is paramount when dealing with vast sums of money flowing through the national banking infrastructure.

The Beneficiary Bank’s Reception and Credit

Upon receiving the batch file from the NEFT clearing system, the beneficiary bank’s internal systems get to work. They meticulously process the incoming transactions, matching the details in the batch file with their own customer records. This reconciliation process is crucial to ensure that the correct amount is credited to the intended beneficiary’s account without errors. It’s a highly automated procedure, but with checks and balances to flag any discrepancies that might arise, ensuring accuracy is maintained.

Once the beneficiary bank confirms the details and successfully processes the transaction, the specified amount is credited to the beneficiary’s account. This usually triggers a notification to the beneficiary via SMS or email, confirming the successful receipt of funds. From your perspective as the remitter, this is when the transfer is finally complete, and your peace of mind is restored. The entire journey, from initiation to credit, generally takes a few hours, depending on when your transaction falls within the batch processing cycle.

Behind the Scenes: Security and Reconciliation

Security is paramount throughout the entire NEFT process. Every step, from your bank’s initial verification to the final credit, is protected by robust encryption and stringent security protocols. The RBI, as the central authority, employs state-of-the-art cybersecurity measures to safeguard the clearing system, protecting against fraud, data breaches, and unauthorized access. This layered security ensures that your financial information and funds remain secure during their digital journey. You can learn more about India’s payment systems on the Reserve Bank of India website.

Beyond security, a continuous reconciliation process operates in the background. Banks constantly match their internal records with the NEFT system’s logs to ensure all debits and credits align perfectly. Any discrepancies are immediately flagged and investigated, ensuring financial integrity. This diligence is why NEFT is incredibly reliable. Even looking ahead to 2026, the underlying architecture is designed for resilience, with backup systems and disaster recovery plans in place to ensure uninterrupted service, minimizing any potential for system-wide disruptions.

Why NEFT Remains a Pillar of Digital Payments

Despite the emergence of faster payment systems like IMPS and UPI, NEFT continues to be a cornerstone of India’s digital payment landscape. Its widespread adoption across virtually all banks, coupled with its reliability and cost-effectiveness for both individuals and businesses, makes it an indispensable tool. It supports a broad range of transactions, from utility bill payments and loan EMIs to large-value corporate transfers, demonstrating its versatility and enduring utility.

While NEFT might not offer instantaneous credit, its batch processing model ensures a highly secure and auditable trail for every transaction. This structured approach is particularly valued for non-urgent payments where certainty and detailed record-keeping are prioritized over immediate settlement. The system’s continuous availability, 24x7x365, further solidifies its position as a go-to option, proving that even a system based on periodic settlements can offer immense convenience and efficiency. For more insights into national payment systems, you might find resources on the NPCI website helpful.

Key Takeaways

- NEFT operates on a batch processing system managed by the Reserve Bank of India, not real-time, which allows for efficient handling of large transaction volumes.

- The process involves three main stages: your bank debiting and packaging the request, the RBI’s central clearing system settling interbank transfers, and the beneficiary bank crediting the account.

- Security and rigorous reconciliation are embedded throughout the entire NEFT framework, ensuring accuracy, preventing fraud, and maintaining the financial integrity of transactions.

- Despite newer, faster payment methods, NEFT’s reliability, cost-effectiveness, and 24/7 availability make it a vital and enduring component of India’s digital financial infrastructure.

Frequently Asked Questions

Why isn’t NEFT instantaneous like IMPS?

NEFT utilizes a batch processing system, meaning transactions are collected and processed in groups at specific intervals throughout the day. This differs from IMPS (Immediate Payment Service), which processes transactions individually in real-time. The batch approach allows NEFT to handle vast volumes efficiently and securely, although it means funds aren’t credited instantly.

Can an NEFT transfer fail, and if so, why?

Yes, an NEFT transfer can fail. Common reasons include incorrect beneficiary account details (account number or IFSC code mismatch), insufficient funds in the remitter’s account, or technical issues at either the remitting or beneficiary bank. In most cases of failure, the funds are automatically reversed to the remitter’s account within a few hours.

Is NEFT available on weekends and holidays?

Absolutely! Since December 2019, NEFT services have been available 24 hours a day, 7 days a week, 365 days a year, including all weekends and public holidays. This significant enhancement ensures that you can initiate and receive NEFT transfers at any time, adding immense convenience for users across the country.

What is the maximum amount I can transfer via NEFT?

While the Reserve Bank of India does not impose any upper limit for NEFT transactions, individual banks may set their own per-transaction limits based on their risk management policies. For instance, some banks might cap online NEFT transfers at ₹10 lakhs or ₹25 lakhs per day, though larger amounts can often be processed by visiting a branch.

Conclusion

Understanding what happens inside the bank after NEFT transfer initiation demystifies a crucial aspect of our digital financial lives. It reveals a meticulously designed system, balancing speed with security and efficiency, all orchestrated by the Reserve Bank of India. The next time you hit ‘send’ on an NEFT transfer, you’ll have a deeper appreciation for the intricate journey your money undertakes, a testament to the robust and reliable infrastructure supporting India’s digital economy. NEFT truly is an unsung hero of modern banking.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ