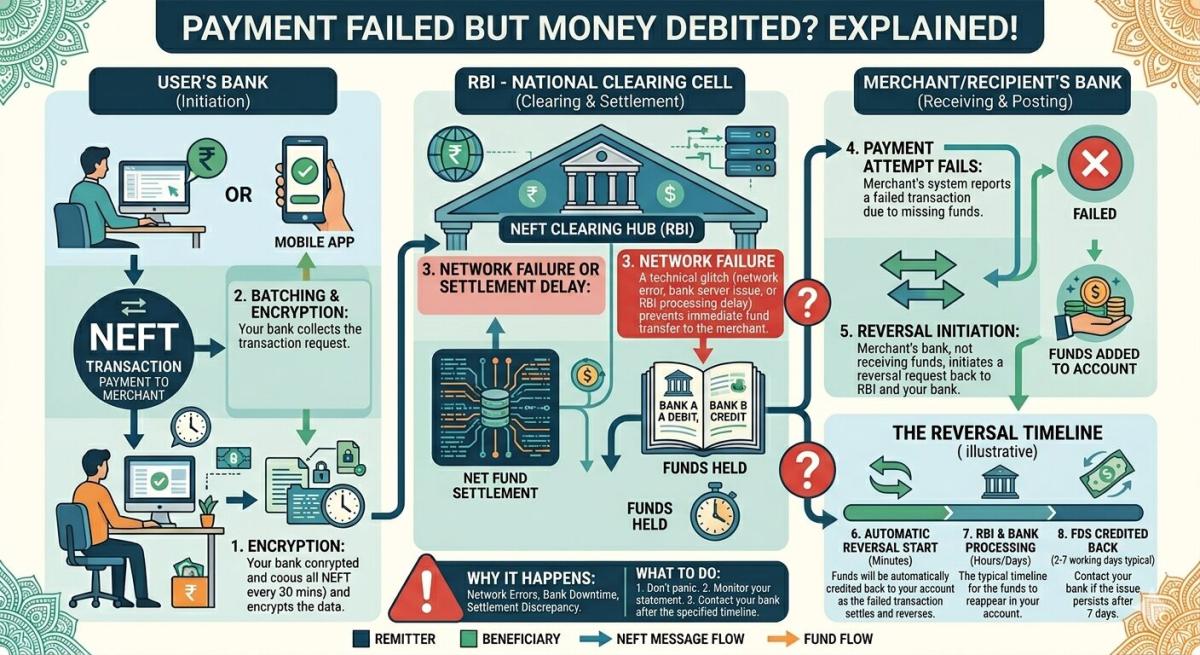

Payment Failed But Money Debited? Explained!

Did your bank balance drop after a failed payment? Learn the difference between authorization holds and settlements, and how long it takes for your money to return.

Table of Contents

There are few things more anxiety-inducing in our digital-first lives than seeing your bank account debited, only for the transaction to fail. I remember vividly a few years ago trying to book a crucial flight, receiving an error message, yet seeing my balance drop. That gut-wrenching feeling of “where did my money go?” is universal. You’re left staring at your screen, wondering why money gets debited without successful transfer, feeling helpless and confused. This isn’t just an inconvenience; it can disrupt plans, cause financial stress, and erode trust in digital payments. Understanding the intricate dance between banks, payment processors, and merchants is key to navigating these frustrating moments, and reassuring yourself that your funds are almost certainly not lost forever.

The Transaction Lifecycle: A Complex Dance

When you initiate a payment, whether online or in person, it triggers a surprisingly complex sequence of events involving multiple entities. It’s not a direct transfer from your account to the merchant’s. Instead, your bank, the card network (Visa, Mastercard, etc.), the payment gateway, and the merchant’s bank all play a role. Each of these steps, from authorization request to final settlement, must complete successfully and in sequence. Think of it as a relay race where the baton must pass perfectly between many runners; a stumble at any point can disrupt the entire process.

This multi-party system means there are numerous points of potential failure. Your bank might approve the funds, but the merchant’s payment gateway could experience a timeout, or the card network might encounter a momentary glitch. Sometimes, even after your bank has provisionally debited your account, the final confirmation that the merchant successfully received the payment never arrives. This creates a temporary limbo where the funds are held by your bank, awaiting either a successful completion signal or a timeout that triggers their return. It’s a delicate balance of speed and security that sometimes goes awry.

Authorization vs. Settlement: The Crucial Distinction

One of the most common reasons for a debited amount without a successful transfer lies in the critical difference between authorization and settlement. When you make a purchase, your bank first “authorizes” the transaction. This means they check if you have sufficient funds and put a temporary hold on that amount, reducing your available balance. This isn’t the actual transfer of money; it’s more like a reservation. The merchant then has a certain period to “settle” the transaction, which is the actual request to move the money from your bank to theirs.

A debit occurs when your bank authorizes the payment and places a hold. If the subsequent settlement fails for any reason – perhaps the merchant’s system crashed, or the connection was lost – the authorized hold might persist for a short period. Your bank has already earmarked those funds, hence the debit you see, but the merchant hasn’t actually received them. The system is designed this way to prevent double-spending and ensure funds are available, but it can lead to confusion when the second, crucial step of settlement doesn’t materialize. It’s a common banking practice, explained further by institutions like the Federal Reserve on payment processes.

Technical Glitches and Network Congestion

In our hyper-connected world, we rely on a vast, intricate network of servers, APIs, and communication protocols for every digital transaction. Even minor technical glitches can wreak havoc on this delicate ecosystem. A momentary server error at the payment gateway, a dropped internet connection on the merchant’s side, or an API timeout between different financial institutions can interrupt the flow of information, causing a transaction to fail mid-process. Your bank might have processed its part, but if the confirmation doesn’t reach the other end, the transfer is incomplete.

Beyond individual system failures, network congestion can also play a significant role. Imagine millions of people trying to complete transactions simultaneously, especially during peak shopping periods like holiday sales or major online events in 2026. The sheer volume can overwhelm payment networks, leading to slowdowns, dropped packets, and ultimately, failed transactions. While banks and payment processors continuously upgrade their infrastructure, there’s always a limit to capacity. When the system is overloaded, some transactions inevitably get stuck in limbo, resulting in a temporary debit without a successful transfer.

The Role of Payment Gateways

Payment gateways act as the crucial intermediary between the merchant, your bank, and the card networks. They encrypt your payment information, route it securely, and ensure compliance with various financial regulations. However, like any complex piece of technology, they are not infallible. A gateway might experience an internal processing error, a database issue, or even a security alert that temporarily halts transactions. When a gateway fails to relay the final confirmation of a successful payment back to your bank, or to the merchant, the money can appear to be debited from your account while the purchase itself is not completed. This often results in a “pending” transaction that eventually reverses.

Insufficient Funds (Even When You Think You Have Them)

This scenario is particularly frustrating: you know you have enough money, yet the transaction fails with a debit. Sometimes, what you see as your “available balance” might not accurately reflect the funds genuinely accessible for new transactions. This can happen if you have other pending transactions that haven’t fully cleared but have already placed a hold on funds. For instance, a gas station pre-authorization or a hotel security deposit might be temporarily holding a larger sum than the actual purchase, impacting your perceived available balance.

Moreover, banks employ sophisticated fraud detection systems that can occasionally flag a legitimate transaction as suspicious, especially if it’s unusual for your spending patterns or involves a new merchant. When this happens, the bank might initiate a temporary debit to hold the funds while they investigate or await your confirmation, but the actual transfer to the merchant is blocked. Daily transaction limits, either set by your bank or the merchant, can also cause a perfectly solvent account to appear to have insufficient funds for a specific purchase, leading to a temporary debit before the transaction is ultimately rejected. For more detailed information, reputable financial institutions like Bank of America often provide resources on how pending transactions affect your balance.

Merchant-Side Issues and Refunds

Sometimes the problem isn’t with your bank or the payment network, but squarely with the merchant’s internal systems. Imagine trying to buy a product online, and the merchant’s inventory system incorrectly shows an item as available. Your payment gets authorized and debited, but when the merchant’s system tries to process the order, it realizes the item is out of stock. The transaction is then cancelled on their end, but the initial debit from your bank might still be pending.

When a transaction fails due to a merchant-side issue, the funds are not lost; they simply haven’t reached the merchant’s account. What typically happens is that the authorization hold on your account will expire, and the funds will automatically be returned to your available balance. This process isn’t instantaneous, however. Depending on your bank and the merchant’s payment processor, it can take anywhere from a few hours to 3-5 business days, and sometimes even longer, for the reversal to fully reflect. Patience is key here, but proactive communication with the merchant can sometimes expedite the process or at least provide clarity on the expected refund timeline for a smoother experience in 2026.

Key Takeaways

- Most debited amounts without successful transfers are temporary authorization holds, not lost money.

- Understand the difference between authorization (temporary hold) and settlement (actual transfer) to grasp why your balance drops.

- Patience is crucial; funds typically auto-reverse within 1-5 business days as authorization holds expire.

- If the issue persists beyond a few business days, contact your bank first, then the merchant, providing all transaction details.

Frequently Asked Questions

How long does it take for my money to be returned after a failed transaction?

Typically, funds from a failed transaction, which are usually just authorization holds, will be automatically released back to your account within 1 to 5 business days. The exact timeframe can vary depending on your bank’s policies and the specific payment processor involved. It’s rarely instant because the systems need to communicate and reconcile the failed attempt.

Should I try the transaction again immediately if it fails and my money is debited?

It’s generally not advisable to immediately retry a transaction if you see a debit without success. Doing so could result in multiple authorization holds on your account, temporarily tying up more of your funds. It’s better to wait a few minutes, check your transaction history for any pending reversals, and if the issue persists, contact the merchant or your bank before attempting again.

Who should I contact first if my money is debited but the transfer failed?

Your first point of contact should usually be your bank. They can confirm the status of the debit (whether it’s an authorization hold or a settled transaction that failed) and provide information on when the funds are expected to be released. If your bank confirms the funds were never successfully transferred to the merchant, then you can reach out to the merchant for further clarification on their end.

Can I prevent my money from getting debited without successful transfer?

While you can’t entirely prevent technical glitches from happening, you can minimize risks. Always ensure you have a stable internet connection. Double-check your payment details before confirming. Keep an eye on your bank statements and available balance regularly. For high-value transactions, consider contacting your bank beforehand to pre-authorize or inform them, especially if you’re traveling or making an unusual purchase, as this can prevent fraud detection systems from blocking a legitimate payment.

Conclusion

Experiencing a debit without a successful transfer is undoubtedly frustrating, but it’s a common occurrence in the complex world of digital payments. By understanding the underlying mechanisms of authorization holds, the multi-party transaction lifecycle, and potential points of failure, you can approach these situations with more confidence and less panic. Remember, your money is almost certainly not lost; it’s usually just in a temporary holding pattern. A little patience, coupled with knowing when and who to contact, will ensure your funds are returned safely to your account, allowing you to proceed with your financial activities without undue stress.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ