Transaction Pending vs. Under Process: What’s the Key Difference?

Confused by "Pending" and "Under Process" bank statuses? Learn what these terms mean for your money, how they affect your balance, and when to take action on delays.

Arjun Sharma

Content Lead – Banking & Payments

10 min read

Table of Contents

Have you ever stared at your online banking app, seeing a transaction stuck in limbo, wondering if your money is truly on its way or if it’s vanished into the digital ether? I certainly have. Just last year, I made a significant international payment, and for what felt like an eternity, it bounced between “pending” and “under process.” The anxiety was real, and it highlighted a common point of confusion for many: the subtle yet critical difference between transaction pending and under process. Understanding these distinct statuses isn’t just about satisfying curiosity; it’s essential for managing your finances, anticipating cash flow, and knowing when to take action. As someone who’s navigated the labyrinth of digital payments for over a decade, I’ve come to appreciate the nuances that separate these seemingly similar terms, and I’m here to demystify them for you.

Understanding Transaction States

Every financial transaction, from swiping your card at a coffee shop to transferring funds online, embarks on a journey through various stages before it’s finally settled. Initially, your bank or payment processor receives the request, marking the very beginning of this intricate process. Think of it as a series of checkpoints, each designed to ensure the validity, security, and accuracy of the funds movement. Without these defined states, the financial system would descend into chaos, making it impossible to track where your money is at any given moment. This structured approach provides clarity and a framework for both institutions and consumers.

These distinct statuses are vital for transparency and accountability within the financial ecosystem. They allow banks to communicate the current stage of a payment to their customers, preventing undue worry or confusion. Furthermore, these states help in identifying potential issues early on, such as insufficient funds, fraud alerts, or technical glitches. For businesses, understanding these states is crucial for inventory management, service delivery, and revenue recognition, ensuring smooth operations and customer satisfaction. It’s a foundational element of modern banking that often goes unnoticed until a transaction hits a snag.

Delving into “Pending”

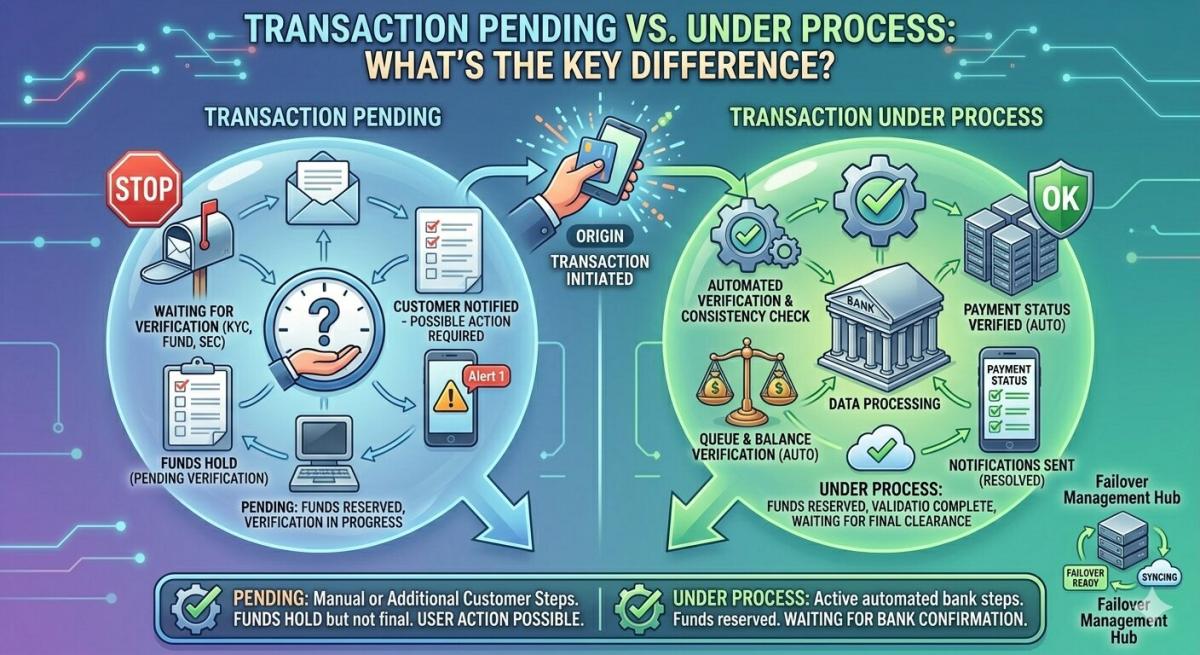

When a transaction is labeled “pending,” it signifies that the payment has been initiated and authorized, but the funds have not yet been fully transferred or settled. Your bank has likely put a hold on the funds in your account, ensuring they are available for the eventual debit, but the actual exchange of money between financial institutions is still in progress. This stage is akin to placing an item in a shopping cart and proceeding to checkout; you’ve committed to the purchase, and the item is reserved, but the payment hasn’t been completely processed by the merchant’s bank. It’s a temporary pre-authorization, safeguarding the funds.

A pending status often arises due to various factors, including the processing times of different banks, the type of transaction (e.g., credit card, debit card, ACH transfer), or even the time of day the transaction was initiated. For instance, a purchase made on a Friday evening might remain pending throughout the weekend because banks typically don’t process settlements on non-business days. While the funds are inaccessible to you, they haven’t officially left your account for good. It’s a waiting game, but one where the outcome is generally predictable, assuming no underlying issues.

Common Reasons for Pending Transactions

Several factors can contribute to a transaction remaining in a “pending” state. One frequent reason is the difference in processing speeds between the originating and receiving banks, especially with cross-border payments or smaller financial institutions. Another common cause involves merchant authorization holds, where a business verifies funds before finalizing a sale, like when you check into a hotel. Technical delays, such as system maintenance or network issues, can also temporarily stall a transaction. Moreover, security protocols, like fraud detection, might flag a transaction for manual review, extending its pending status until verified by an analyst. These are all part of the digital payment landscape we navigate in 2026.

Unpacking “Under Process”

The term “under process” typically indicates a more active and complex stage than “pending.” While “pending” often refers to the initial authorization and hold, “under process” suggests that the transaction is actively moving through the internal systems of one or more financial institutions. This could involve validation checks, compliance reviews, fraud scrutiny, or queuing for batch processing. It implies that the transaction is undergoing a series of steps to ensure its legitimacy and to prepare it for final settlement. The funds are no longer just held; they are being actively managed and moved through the payment network.

In my professional experience, “under process” often signals a point where the transaction is being reconciled with bank ledgers, undergoing clearing, or awaiting final settlement instructions from a payment network like Visa or Mastercard. It might also mean that a manual review is underway due to a flagged anomaly or a specific regulatory requirement. Unlike a simple pending status, which usually resolves itself, a prolonged “under process” status can sometimes hint at a deeper issue that requires attention. It’s a more active state of flux, where the transaction is deeper within the financial system’s machinery.

Why These Distinctions Matter

Understanding the difference between transaction pending and under process is crucial for effective financial management and peace of mind. For consumers, it helps in accurately tracking available balances and avoiding overdrafts. If a transaction is merely pending, the funds are temporarily reserved; if it’s under process, it’s closer to being finalized, meaning those funds are truly committed. This distinction informs your spending decisions and helps you anticipate when your account balance will reflect the true impact of a transaction. It’s about having a clearer picture of your real-time financial standing.

For businesses, these distinctions are even more critical. Knowing whether a payment is pending or actively under process affects cash flow forecasting, inventory management, and customer relations. A pending payment might mean goods shouldn’t be shipped yet, whereas an under-process payment indicates a higher likelihood of successful completion, allowing for earlier fulfillment. It also helps in identifying potential bottlenecks in their payment gateway or banking relationships. In the fast-paced economy of 2026, precise understanding of these statuses can be a significant competitive advantage, improving operational efficiency and customer trust.

Navigating Delays and Next Steps

When a transaction lingers in either “pending” or “under process” for an unusually long time, it’s natural to feel concerned. The first step is always to check the estimated processing times for the specific type of transaction and the institutions involved. For example, an international wire transfer will naturally take longer than a local debit card purchase. If the delay exceeds the typical timeframe, contact your bank or the payment processor directly. Provide them with all relevant details, such as the transaction ID, date, amount, and recipient. They have the tools to investigate the specific stage and reason for the hold-up.

What I’ve observed over the years is that proactive communication can often resolve issues faster. Don’t wait for days if you suspect a problem. If your bank can’t provide a satisfactory answer, the next step is to contact the recipient’s bank or the merchant. Sometimes, the issue lies with their end of the transaction. Keep meticulous records of all communications, including dates, times, and names of representatives you speak with. This documentation can be invaluable if you need to escalate the issue further, perhaps to a regulatory body like the Federal Reserve’s payment systems division or a consumer protection agency.

Key Takeaways

- “Pending” means authorized but not settled: Funds are reserved, but the actual transfer between banks hasn’t completed. It’s a temporary hold, usually resolving within a few business days.

- “Under Process” indicates active movement and checks: The transaction is actively being processed through financial systems, undergoing validation, compliance, and potentially manual review. It’s a more involved stage than simple pending.

- Distinctions impact financial planning: Understanding these statuses helps consumers manage available funds more accurately and allows businesses to better forecast cash flow and manage operations.

- Know when to act on delays: If a transaction remains in either state beyond typical processing times, initiate contact with your bank, payment processor, or the recipient to investigate and resolve potential issues.

Frequently Asked Questions

How long do transactions typically stay pending?

Most pending transactions, especially credit or debit card purchases, typically resolve within 1-3 business days. ACH transfers can take 3-5 business days. Factors like weekends, holidays, and the specific banks involved can extend these timeframes, but generally, they don’t linger for more than a week without a specific reason.

Can I cancel a transaction that is “under process”?

Canceling an “under process” transaction is significantly more difficult than canceling a pending one, and often impossible without the cooperation of the recipient or the recipient’s bank. Once funds are actively moving through the clearing system, they are largely committed. You would typically need to request a reversal, which is not guaranteed and can incur fees.

What if my transaction is stuck in “pending” or “under process” for too long?

If a transaction seems stuck, first verify the typical processing time for that transaction type. If it exceeds that, immediately contact your bank’s customer service with all transaction details. They can often provide insights into the delay or initiate an investigation. If the issue persists, consider escalating to a supervisor or relevant regulatory body.

Does the difference between transaction pending and under process affect my credit score?

No, the status of an individual transaction (pending vs. under process) does not directly affect your credit score. Your credit score is influenced by factors like payment history, credit utilization, and length of credit history. However, a transaction failing to settle due to insufficient funds, leading to an overdraft, could indirectly impact your financial health if it results in fees or reported negative activity.

Conclusion

Navigating the world of digital payments can feel like a maze, but a clear understanding of terms like “pending” and “under process” empowers you. These aren’t just technical jargon; they are vital indicators of your money’s journey through the financial system. By recognizing the subtle yet significant difference between transaction pending and under process, you gain greater control over your finances, reduce anxiety, and know precisely when to intervene if things go awry. In an increasingly digital economy, being an informed participant is your best defense against financial headaches, ensuring your transactions move smoothly into 2026 and beyond.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ