What Happens When Your Transaction Fails?

Staring at a "Transaction Failed" message? Learn what happens to your money, why authorization holds appear as pending, and the 4 steps to take immediately.

Arjun Sharma

Content Lead – Banking & Payments

11 min read

Table of Contents

Have you ever been there? You’ve meticulously filled out your shipping details, double-checked your order, and hit ‘purchase,’ only to be greeted by that dreaded message: “Transaction Failed.” It’s a gut punch, isn’t it? That moment of confusion, frustration, and a touch of panic as you wonder, “What happens when transaction is marked as failed?” Is my money gone? Will my order ever arrive? As someone who’s navigated the labyrinth of digital payments for over a decade, both as a consumer and on the backend, I can tell you it’s a far more common occurrence than most realize, and understanding the mechanics behind it can save you a lot of undue stress and potential headaches.

The Immediate Aftermath: What You See and Feel

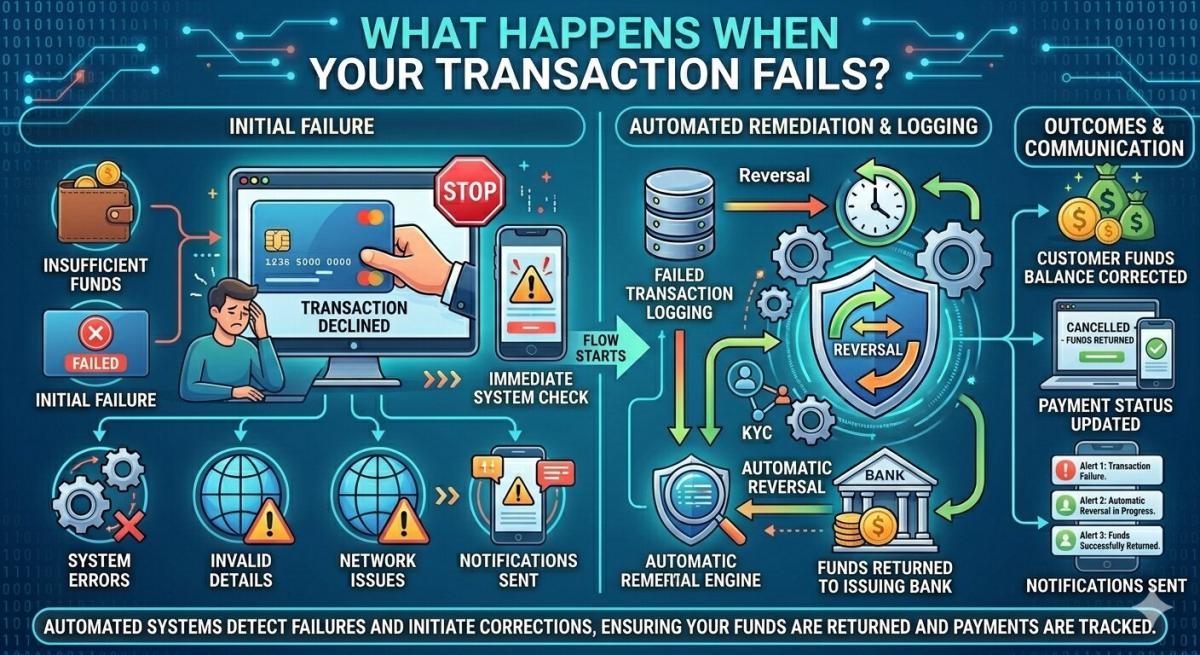

When a transaction is marked as failed, the immediate sensation is often one of bewilderment. You might see a generic error message on the merchant’s website, an email notification that your order couldn’t be processed, or even a push notification from your bank indicating a declined attempt. My personal experience, and countless stories from others, reveal that these messages are rarely specific enough to tell you why it failed, leaving you to guess. This ambiguity is precisely why the initial moments are crucial for preventing further issues and understanding the next steps, rather than simply trying again blindly.

The emotional rollercoaster that follows can range from mild annoyance to significant concern, especially if it’s a large purchase or an urgent bill payment. You might immediately check your bank account or credit card statement, often finding a “pending” charge that adds to the confusion. It’s important to remember that a “failed” status on the merchant’s end usually means the transaction did not complete, and while an authorization hold might appear on your bank statement, the funds are rarely debited permanently. This distinction is paramount for maintaining calm and proceeding with a clear head.

The Underlying Reasons: Why Transactions Fail

Behind every “transaction failed” message lies a specific reason, though it’s often obscured from the end-user. The most common culprits include insufficient funds in the account, incorrect payment details (a mistyped card number, wrong expiry date, or CVV), or a daily spending limit being exceeded. Sometimes, it’s a simple network glitch – a momentary hiccup between your device, the merchant’s server, and your bank. These technical blips are increasingly rare in 2026 thanks to robust infrastructure, but they do still occur, especially during peak shopping periods or with less sophisticated payment gateways.

Beyond these user-centric or technical issues, banks play a significant role in declining transactions. They might flag a payment as suspicious due to unusual activity, a large purchase out of your normal spending pattern, or an attempt to purchase from a new, unknown merchant, all in the name of fraud prevention. Additionally, the merchant’s payment processor might encounter an issue, or their fraud detection systems could mistakenly decline a legitimate transaction. Understanding this multifaceted landscape helps demystify the failure and guides your investigation, rather than leaving you in the dark wondering if your card is broken.

The Psychology of Held Funds

One of the most anxiety-inducing aspects of a failed transaction is the appearance of a “pending” charge on your bank statement. It feels like your money is gone, yet the transaction didn’t go through. This is what’s known as an authorization hold. When you attempt a purchase, your bank “authorizes” the merchant to take the funds, essentially earmarking that amount. If the transaction then fails for any reason (e.g., incorrect CVV, merchant server error), the authorization is never “captured.” The funds are temporarily held, but they are not actually debited from your account. It’s a common misconception that this means the transaction went through and will eventually post; in most failed scenarios, it will simply expire.

The duration of these authorization holds varies, typically from a few hours to several business days, depending on your bank’s policies and the type of transaction. For example, some banks might release an authorization hold within 24 hours for a failed online purchase, while others could take up to 7-10 business days. It’s a frustrating waiting game, but knowing that the money is almost certainly not lost can alleviate significant stress. This temporary ‘limbo’ state highlights the crucial difference between an authorized transaction and a settled, completed one, a distinction that often eludes consumers.

Funds in Limbo: Pending vs. Posted

The distinction between a “pending” transaction and a “posted” or “settled” one is critical when dealing with failures. When you initiate a payment, your bank often places an authorization hold on the funds. This means the money is temporarily set aside, reducing your available balance, but it hasn’t actually left your account and gone to the merchant. If the transaction fails, this authorization is never “captured” by the merchant. Consequently, after a certain period, the hold expires, and the funds are released back into your available balance, as if nothing happened. This process can be frustratingly slow, sometimes taking several business days, but it’s a standard banking procedure designed to ensure funds are available if the transaction proceeds.

A “posted” transaction, on the other hand, means the funds have successfully been transferred from your account to the merchant’s. If a transaction is marked as failed on the merchant’s side, but it appears as “posted” on your bank statement, then you have a more complex issue. This typically indicates a discrepancy between the merchant’s system and your bank’s, or perhaps a delayed update. In such rare cases, you would need to contact both your bank and the merchant, as the merchant might need to initiate a refund for funds they received but for which they did not fulfill an order. Understanding this difference is key to knowing whether your funds are truly in limbo or if they’ve actually been debited.

Your Action Plan: Steps to Take Immediately

When faced with a failed transaction, your first step should always be to verify the details. Did you enter the correct card number, expiry date, and CVV? Is your billing address accurate? A surprising number of failures stem from simple typos. Next, check your bank or credit card statement for any pending charges. If there’s an authorization hold, note it, but understand it’s likely temporary. If you’re still unsure, or if the failure persists after re-entering details, it’s time to contact the merchant’s customer support. They can often see more detailed decline codes from their payment processor, which can pinpoint the exact reason for the failure. Be prepared with your attempted transaction details, including time and amount.

If the merchant can’t provide a clear resolution, or if your bank statement shows a posted charge for a failed transaction, your next call is to your bank. Explain the situation clearly, providing them with all the information you’ve gathered. They can confirm whether the transaction was truly declined, if an authorization hold is in place, or if funds were indeed debited. They can also investigate if their fraud detection system was the cause of the decline. Remember to remain calm and methodical; most issues are resolvable with a bit of patience and communication. For more general advice on consumer rights, resources like the Consumer Financial Protection Bureau offer valuable guidance in the US, and similar bodies exist globally.

Merchant Perspective: Handling Failed Transactions

From a merchant’s standpoint, every failed transaction is a lost sale and a potential blow to customer satisfaction. Businesses invest heavily in robust payment gateways and fraud detection systems to minimize these occurrences. When a transaction fails, it triggers a series of backend processes. Many sophisticated e-commerce platforms in 2026 incorporate automated retry mechanisms for certain types of declines, such as temporary network errors, attempting the charge again within a short window. However, for hard declines (like incorrect card details or bank refusal), the merchant must rely on the customer to re-initiate the payment.

Furthermore, failed transactions also inform a merchant’s fraud prevention strategies. A high rate of failed attempts from a specific IP address or card number can trigger alerts, potentially leading to manual review or even blacklisting to protect against fraudulent activity. It’s a delicate balance: minimize legitimate declines to ensure sales, while maximizing fraud prevention. Customer service teams are often trained to handle these inquiries, viewing each failed transaction as an opportunity to salvage a sale and build trust. Sometimes, a customer service agent can even guide you through alternative payment methods or troubleshoot specific errors unique to their system, demonstrating the interconnectedness of payment processing and customer retention.

Key Takeaways

- “Failed” Doesn’t Mean “Lost”: A transaction marked as failed on the merchant’s side almost always means your money was not debited, even if a temporary authorization hold appears on your bank statement.

- Common Causes Are Preventable: Many failures stem from simple errors like incorrect card details, insufficient funds, or exceeding daily limits. Always double-check your input.

- Authorization Holds Are Temporary: Funds placed on hold after a failed transaction will typically be released back to your available balance within a few business days, depending on your bank’s policy.

- Be Proactive, Not Panicked: If a transaction fails, methodically check details, review your bank statement, and contact the merchant’s support, followed by your bank if necessary. Patience and clear communication are key.

Frequently Asked Questions

Why do I see a pending charge if the transaction failed?

When you attempt a purchase, your bank places an authorization hold on the funds. This temporarily reserves the money. If the transaction then fails for any reason (e.g., incorrect CVV, merchant error), the merchant never “captures” these funds. The hold will automatically expire, and the money will be released back to your account, typically within 1-7 business days, depending on your bank.

Should I try the transaction again immediately?

It depends on the suspected reason for the failure. If you suspect a simple typo in your card details, correcting it and trying again is reasonable. However, if the reason is unclear, or if your bank explicitly declined it, repeatedly trying could lead to multiple authorization holds or even temporarily lock your card for suspicious activity. It’s best to investigate first.

What if my bank account shows the money was actually debited, but the merchant says it failed?

This is a less common but more concerning scenario. It indicates a discrepancy between your bank’s records and the merchant’s. Immediately contact both your bank and the merchant. Your bank can provide proof of debit, and the merchant can investigate if funds were received but not matched to an order. You may need to dispute the charge with your bank if the merchant cannot resolve it.

How long does it take for a pending charge from a failed transaction to disappear?

The timeframe varies significantly by bank and transaction type. Most authorization holds for failed online transactions are released within 24-72 hours. However, some can take up to 5-10 business days. If it persists beyond this, contact your bank to inquire about the specific hold and its expected release date.

Conclusion

While encountering a “transaction failed” message is undeniably frustrating, understanding the mechanics behind it can transform a moment of panic into a manageable situation. Most often, your funds are safe, merely held in limbo, and a little investigative work is all that’s required. By being prepared, methodical, and communicating effectively with merchants and banks, you can navigate these digital hiccups with confidence. Remember, in 2026, payment systems are more resilient than ever, but human error and the occasional technical glitch are still part of the online experience.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ