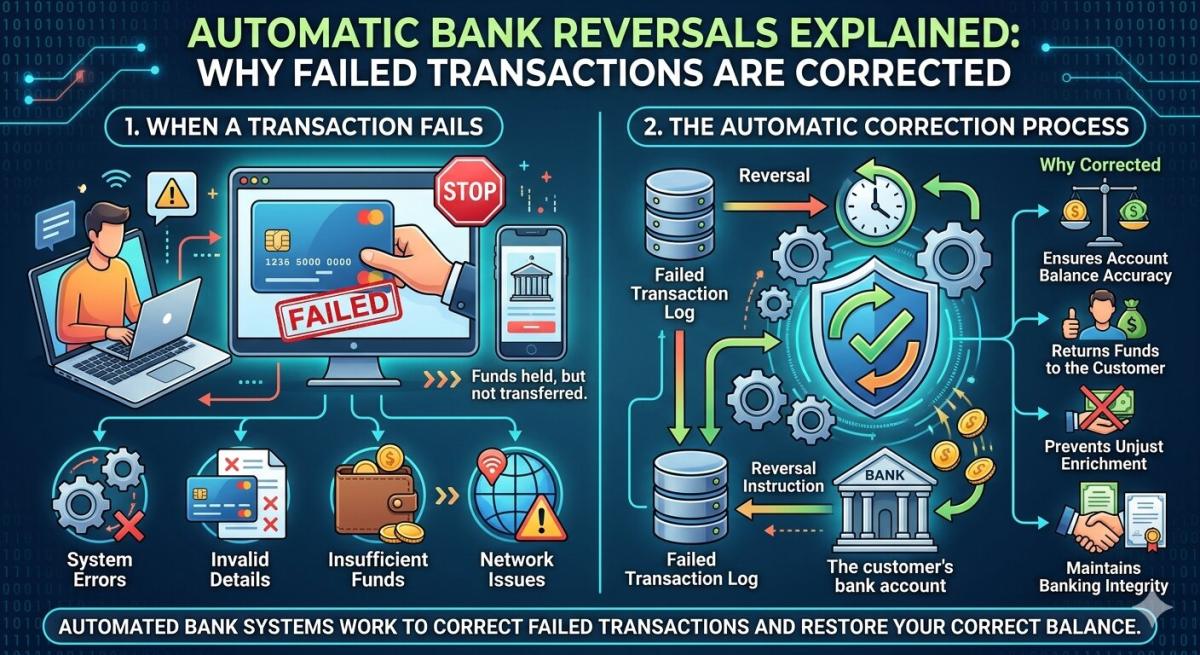

Automatic Bank Reversals Explained: Why Failed Transactions Are Corrected

Ever wonder why a failed transaction charge disappears from your bank account? Learn the mechanics of automatic reversals, payment holds, and consumer protections.

Table of Contents

Have you ever completed an online purchase, only to see a dreaded “transaction failed” message pop up? It’s a stomach-dropping moment, isn’t it? My heart has sunk more times than I care to admit, especially when trying to snag limited-edition concert tickets or book a critical flight. The immediate panic is usually about the money: Did it go through? Will I be charged? Then, often, a wave of relief washes over you as the pending charge vanishes, sometimes almost instantly. This automatic disappearance isn’t magic; it’s a sophisticated system at work. Understanding exactly Why Bank Reverses Failed Transactions Automatically is crucial for anyone navigating the modern digital economy, offering peace of mind and clarity in an increasingly complex financial landscape.

The Mechanics of a Transaction Failure

When you initiate a payment, whether online or in-store, a complex series of communications occurs between your bank, the merchant’s bank, and the respective payment networks. A transaction can fail for numerous reasons: insufficient funds, an expired card, incorrect CVV, network timeout, or even a fraud detection flag. Each failure point triggers a specific response within the payment ecosystem. It’s a ballet of data, and if one dancer misses a step, the whole performance is halted, but not without a predetermined fallback plan to ensure fairness.

The system is designed with inherent fail-safes to prevent money from being stuck in limbo. Upon a failed authorization, the payment network (like Visa or Mastercard) immediately communicates this to both banks. Your bank, having received the initial request to hold funds, is then instructed to release that hold. This process is typically automated and happens very quickly, often within seconds or minutes, ensuring your available balance reflects the reality of the failed attempt. It’s an essential consumer protection mechanism that has evolved significantly over the years.

Protecting Consumers and Merchants Alike

The primary reason banks automatically reverse failed transactions is to protect both consumers and merchants from financial discrepancies and potential fraud. Imagine the chaos if every failed attempt resulted in a temporary hold on your funds that required manual intervention to resolve. Consumers would face endless frustration, and merchants would be inundated with customer service inquiries, hindering their ability to conduct business efficiently. This automated reversal ensures that funds are not inadvertently tied up, maintaining liquidity and trust in the payment system.

From a merchant’s perspective, an automatic reversal means they never actually receive the funds for a failed transaction, preventing situations where they might accidentally ship goods for which they haven’t been paid. It streamlines their accounting and reduces chargeback risks, which can be costly and time-consuming. This system is a cornerstone of modern commerce, built on the principle that only successful transactions should result in actual fund transfers, preserving the integrity of financial records for all parties involved.

Regulatory Frameworks and Network Rules

The necessity for automatic reversals is deeply embedded in the regulatory frameworks governing financial institutions and the operating rules set by major payment networks. Organizations like the Federal Reserve in the United States, through regulations such as Regulation E (Electronic Fund Transfers), mandate specific consumer protections regarding unauthorized transactions and error resolution. These rules ensure that banks have clear guidelines for handling transaction discrepancies and protecting consumers’ funds. You can find more details on these regulations on the Federal Reserve’s official website.

Furthermore, global payment networks like Visa, Mastercard, and American Express enforce strict operating rules for their member banks. These rules dictate how transactions are processed, authorized, settled, and, crucially, how failed transactions are handled. They mandate the immediate release of authorization holds for unsuccessful attempts, ensuring consistency across millions of daily transactions worldwide. These network rules are non-negotiable for participating banks, forming a critical layer of consumer and merchant protection that underpins the entire payment ecosystem.

Common Scenarios for Automatic Reversals

One of the most frequent reasons for an automatic reversal is an “insufficient funds” error. If your account balance cannot cover the transaction amount, the authorization request is declined, and any temporary hold on a partial amount is immediately released. This prevents your account from being overdrawn and incurring fees, which is a huge relief for many. Another common scenario involves technical glitches, such as a momentary network outage at the merchant’s point-of-sale system or an internet connectivity issue during an online payment. The system detects the communication breakdown and automatically cancels the pending transaction.

Card security features also play a significant role. If a transaction triggers a fraud alert – perhaps it’s an unusually large purchase, or it occurs in a location far from your typical spending habits – your bank might decline the transaction as a protective measure. In such cases, the system immediately reverses any pending charge, preventing potential fraudulent activity from impacting your actual balance. This proactive approach, while sometimes inconvenient, is vital for safeguarding your financial security in an increasingly digitized world, especially as we look towards more integrated systems by 2026.

When an Automatic Reversal Doesn’t Happen

While automatic reversals are the norm, there are rare instances where a failed transaction might still show as a pending charge for a longer period. This usually occurs due to a timing discrepancy or a specific type of error in the authorization process, where the initial hold was placed but the subsequent “void” or “reversal” message didn’t propagate correctly or quickly enough. It’s not that the bank isn’t working to fix it; it’s often a matter of reconciliation between various systems that operate on different schedules. Most banks have a policy to automatically drop these pending holds within a few business days, typically 3-5, if the merchant doesn’t claim the funds.

If you encounter a persistent pending charge for a failed transaction, the first step is always to wait a few business days. If it still hasn’t cleared, contact your bank. They can investigate the specific transaction, identify why the hold hasn’t been released, and often manually intervene to remove it. Remember, these situations are exceptions, not the rule, and financial institutions are generally quite adept at resolving them. It’s also worth checking the merchant’s policy, as some have specific procedures for handling failed payments, which you can often find on reputable sites like the Consumer Financial Protection Bureau.

Key Takeaways

- Automatic reversals protect you and merchants by preventing funds from being stuck in limbo after a failed payment attempt.

- These reversals are mandated by payment network rules and financial regulations, ensuring consistency and consumer safety across all transactions.

- Common reasons for automatic reversals include insufficient funds, technical errors, and fraud detection flags, all designed to safeguard your financial well-being.

- While most failed transactions reverse instantly, a persistent pending charge might require a few days to clear; contact your bank if it lingers beyond that timeframe.

Frequently Asked Questions

How quickly do failed transactions usually reverse?

Typically, failed transactions reverse almost instantly, within seconds or minutes. Your bank’s systems are designed to immediately release authorization holds if the transaction doesn’t go through. In some cases, especially with certain merchant systems or network delays, it might take a few hours, but usually not longer than a business day.

Can a bank charge me for a failed transaction?

No, banks generally do not charge you for a failed transaction itself. However, if the transaction failed due to insufficient funds and caused your account to go into overdraft before the system could fully process the decline, you might incur an overdraft fee. This is why banks often decline immediately to prevent such fees.

What should I do if a failed transaction doesn’t reverse?

If a pending charge from a failed transaction doesn’t disappear after 3-5 business days, your best course of action is to contact your bank directly. Provide them with the transaction details (date, merchant, amount), and they can investigate the hold and often manually release it for you. Keeping records is always a good idea.

Are automatic reversals different from refunds?

Yes, absolutely. An automatic reversal happens when a transaction fails to complete, so the funds are never actually transferred to the merchant; it’s just a hold that gets released. A refund, on the other hand, occurs when a transaction successfully completed and the merchant later initiates a return of funds for various reasons, such as a product return or service cancellation.

Conclusion

The automatic reversal of failed transactions is a testament to the robust and increasingly intelligent infrastructure underpinning our financial world. It’s a critical, often unseen, safety net that protects both consumers and businesses from the complexities of digital payments. My personal experience has taught me to appreciate this seamless process, recognizing it as a fundamental pillar of trust and efficiency. As we move towards 2026, with even more sophisticated payment technologies emerging, these automated safeguards will only become more refined, ensuring your money is always where it should be – securely in your account, until a successful transaction truly calls for its transfer.

Related Blogs

Published on Apr 09, 2026

IFSC Code Explained: How Banks & Branches Connect Internally

Ever wonder how banks communicate? Explore the internal mechanics of how the IFSC code links your branch to the national payment network for NEFT, RTGS, and IMPS.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Transaction Cut-Off Times: Avoid Fund Transfer Delays

Learn how transaction cut-off times affect fund transfers, ACH payments, wire transfers, and real-time payments to avoid delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Transactions Are Delayed on Weekends & Holidays

Learn why bank transactions are delayed on weekends and holidays, including ACH processing, bank cut-off times, fraud checks, and interbank settlement delays in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Bank Processing Times Differ Between Banks

Learn why bank processing times vary between banks, including ACH, wire transfers, SWIFT, compliance checks, cut-off times, and banking technology in 2026.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 09, 2026

Why Are Bank Transfers So Slow? The Real Reasons Revealed

Discover why bank transfers are slow, including legacy banking systems, ACH processing, fraud checks, intermediary banks, and cut-off times in 2026.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ