Section 80C Investments: Full List, ₹1.5 Lakh Limit, and Which Option Wins

Save tax with Section 80C investments. Explore the full list, ₹1.5 lakh limit, and compare options to choose the best tax-saving investment for you.

Priya Nair

Senior Compliance Editor at IFSC.co

12 min read

Table of Contents

- What is Section 80C?

- ₹1.5 Lakh Deduction Limit Explained

- Why Section 80C Is So Popular

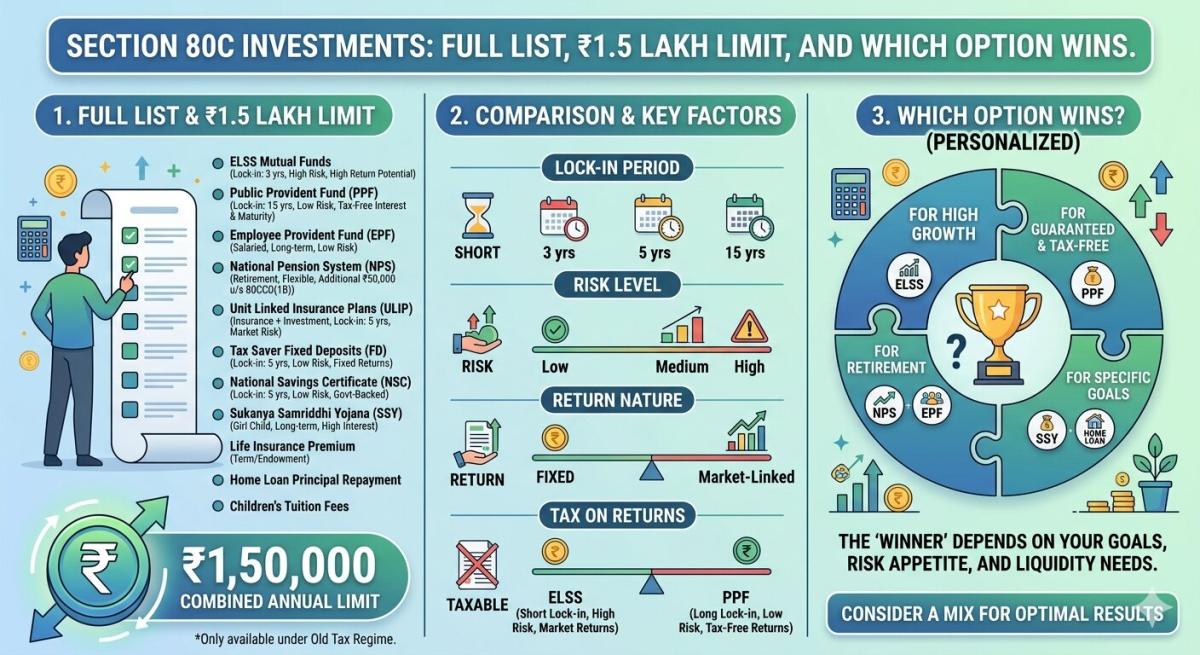

- Full List of Eligible Section 80C Investments

- Comparing the Best Section 80C Investment Options

- Which Section 80C Investment Option is the Best?

- How to Claim Section 80C Deductions?

- Limitations of Section 80C

- Final Thoughts

- FAQs

Saving on taxes is a thought that almost everyone thinks about during the financial year. Many individuals seek ways to legally reduce their taxes while also planning for future wealth creation. Making investments under Section 80C is one of the most popular ways to save big on taxes.

Section 80C is a part of the Income Tax Act that allows individuals to claim a deduction for their investments. This is a good option for saving on taxes and creating future wealth.

However, the deductions can only be claimed if the taxpayer has opted for the old tax slab. In this blog, we will discuss everything you need to know about investments under Section 80C, where we will also understand the deduction limit of 1.5 lakhs and which option is the best for you.

What is Section 80C?

Section 80C is a popular option for saving income tax under the Income Tax Act, 1961. This section enables individuals to save income tax by claiming a deduction for the financial instruments.

In other words, if you invest your money through the 80C investment option, you can save income tax on the money you have invested. This is because you can claim a deduction for the money you have invested.

Assume that you have an income of 10 lakhs. Now, if you have invested 1.5 lakhs through the 80C investments option, you can save income tax on the money you have invested by claiming a deduction for the money you have invested.

Section 80C is a popular option for saving on income tax because it allows you to reduce your tax bill and build wealth for the future.

₹1.5 Lakh Deduction Limit Explained

One of the most important aspects of Section 80C investments is the deduction limit. The maximum deduction limit allowed under Section 80C is up to ₹1.5 lakh.

This includes all the following:

- Section 80C

- Section 80CCC

- Section 80CCD(1)

All these have a combined deduction limit of up to ₹1.5 lakh.

Although one more deduction is available under Section 80CCD(1B). It allows an additional ₹50,000 in tax deductions for investments in the National Pension Scheme (NPS). This additionally increases the maximum amount available for deduction under Section 80C up to ₹2 lakhs.

Who Can Claim Section 80C Deductions?

Not everyone can claim these deductions under Section 80C. Only the following taxpayers are eligible for these deductions:

- Individual taxpayers

- Hindu Undivided Families (HUF)

Note that companies, partnership firms, LLPs, etc., cannot claim these deductions.

One more condition must be satisfied to claim these deductions. This deduction can be claimed only if you have opted for the old system.

Therefore, if you have opted for the new system of taxation, then these deductions are not available to you. This is why these two need to be compared, and then the best option can be selected.

Why Section 80C Is So Popular

There are several reasons for this.

Diverse Investment Options: Taxpayers can invest in a variety of options available under government schemes.

Long-Term Investment Options: By investing in the Section 80C scheme, the taxpayer is helped in the long term.

Full List of Eligible Section 80C Investments

There are plenty of investment options available in the market under the tax-saving scheme of Section 80C. Each investment option in the scheme has its own characteristics. Here are some of the most popular investment options available in the scheme:

1. Life Insurance Premium

Investing in life insurance is one of the most popular investment options under Section 80C tax-saving schemes.

When investing in life insurance, the taxpayer can save on taxes, as the premium is deductible.

Although a caveat here is that the policy should be able to satisfy the conditions with respect to the premium amount invested in the life insurance for the taxpayer in order to become eligible for the tax benefits under the scheme.

2. Public Provident Fund (PPF)

PPF is a long-term savings instrument with a government guarantee. It is one of the safest investment options under Section 80C.

It has a 15-year lock-in period. It also offers fixed interest rates, which are revised by the government from time to time.

One of the major advantages of PPF is the tax benefits it offers. It offers tax benefits at three levels: the investment amount, the interest generated, and the maturity amount.

Here’s an example of the money invested in a PPF: Rs. 1.5 lakh invested annually for 15 years at ~7.1% interest yields Rs. 40 lakh. If you want to do a detailed calculation of the returns you will earn on the investment, you can use a PPF calculator.

3. National Savings Certificate (NSC)

NSC is another government-sponsored investment plan that is eligible for Section 80C deductions.

The scheme has a fixed tenure of five years and offers assured returns. This is an excellent option for conservative investors seeking regular income.

3. Equity Linked Savings Scheme (ELSS)

ELSS is a type of mutual fund that offers tax benefits. ELSS investments are linked to the market and considered a safe option under Section 80C.

Among all investments under Section 80C, ELSS has the shortest lock-in period of just 3 years.

Since the investments are market-linked and carry more risk, they also promise higher returns. ELSS investments have shown higher returns in the long term.

4. Sukanya Samriddhi Yojana (SSY)

SSY is a government-approved scheme for the higher education of a girl child. It is a long-term savings plan with attractive interest rates and tax benefits.

The scheme's maturity period is until the child turns 21. The account can be withdrawn partially after the child turns 18.

5. Home Loan Principal Repayment

Homeowners are unaware that the principal repayment component of their home loan Equated Monthly Instalment (EMI) is eligible for deduction under Section 80C.

This enables you to reduce your tax liability while you pay off your home loan.

However, you would not be allowed to sell your property within five years of possession, or you would face a reversal of tax benefits.

6. Tuition Fees

Parents may also claim tax deductions for tuition fees paid for the education of their children.

The deduction is applicable for a maximum of two children, and the fees must be paid to any school, college, or university within the country.

This is a good incentive for people to invest in the education of their children while at the same time benefiting from a tax deduction.

Comparing the Best Section 80C Investment Options

The best investment option depends on an individual's financial goals and the level of risk they are willing to take. The table below compares the popular Section 80C investment options.

|

Investment Option |

Average Returns |

Lock-in Period |

Risk Level |

|

ELSS Mutual Funds |

12%-15% |

3 years |

High |

|

ULIP |

8%-10% |

5 years |

Medium |

|

Tax Saving FD |

6%-8% |

5 years |

Low |

|

PPF |

Around 7.9% |

15 years |

Low |

|

NSC |

Around 7.9% |

5 years |

Low |

|

Sukanya Samriddhi Yojana |

Around 8.5% |

Long term |

Low |

By comparing the options, you can understand their performance.

Which Section 80C Investment Option is the Best?

The "best" investment option under Section 80C will depend on many factors, including a person's financial goals. There's no single "best" investment option. Different investment options under Section 80C are suitable and tailored for different types of people and investors. However, here's a breakdown that will help investors:

- People who prefer low-risk investments: Invest in PPF, NSC, or fixed deposits. These options offer low and fixed returns with very low risk.

- People with a higher risk tolerance: If you want better returns, opt for an ELSS. This option has the potential to offer higher returns in the long term.

- People seeking stable returns: This group should opt for a tax-saving FD or a ULIP for safety and relatively predictable returns.

The best strategy is to invest your money across multiple schemes and maintain a balanced portfolio. This will greatly increase the chances of stability and maximise your returns.

Example: How Section 80C Reduces Tax

Let us learn how Section 80C investments help in reducing tax through an example.

- For example, a person’s salary is ₹10 lakh, and their additional income is ₹1 lakh.

- The total income is ₹11 lakh.

- After deducting the standard deduction of ₹50,000, the income becomes ₹10.5 lakh.

- If the individual invests ₹1.5 lakh in Section 80C investments, the income is reduced to ₹9 lakh.

Let us now understand this example in detail using income and tax calculations:

Income Calculation (Before and After Section 80C Deduction)

|

Particulars |

With 80C Deduction |

Without 80C Deduction |

|

Salary Income |

₹10,00,000 |

₹10,00,000 |

|

Standard Deduction |

₹50,000 |

₹50,000 |

|

Income After Deduction |

₹9,50,000 |

₹9,50,000 |

|

Other Income |

₹1,00,000 |

₹1,00,000 |

|

Gross Total Income |

₹10,50,000 |

₹10,50,000 |

|

Section 80C Deduction |

₹1,50,000 |

— |

|

Taxable Income |

₹9,00,000 |

₹10,50,000 |

This shows how investing under Section 80C reduces the taxable income.

Tax Calculation (Old Tax Regime)

|

Tax Slab |

With 80C Deduction |

Without 80C Deduction |

|

Up to ₹2.5 lakh |

Nil |

Nil |

|

₹2.5L – ₹5L (5%) |

₹12,500 |

₹12,500 |

|

₹5L – ₹9L / ₹10L (20%) |

₹80,000 |

₹1,00,000 |

|

Above ₹10L (30%) |

— |

₹10,000 |

|

Total Tax |

₹92,500 |

₹1,22,500 |

|

Health & Education Cess (4%) |

₹3,700 |

₹4,900 |

|

Final Tax Payable |

₹96,200 |

₹1,27,400 |

This table compares the actual tax payable in both scenarios.

Final Tax Saving

- Tax without deduction: ₹1,27,400

- Tax with deduction: ₹96,200

Total Tax Saved = ₹31,200

As shown in the tables, Section 80C deductions reduce taxable income by ₹1,50,000, thereby reducing the tax payable.

How to Claim Section 80C Deductions?

If you want to claim the deductions under Section 80C, you should follow these steps:

You should invest in the options under Section 80C before the end of the financial year, i.e., before March 31.

You should have proper documents for the investments you have already made.

You should inform your employer about your investments so that the tax deduction at source (TDS) is correctly calculated.

While filing your income tax return, you should claim the deductions under Chapter VI-A.

If you follow these steps, you will definitely enjoy the benefits of investing under Section 80C without any problem while filing your income tax return.

Limitations of Section 80C

Although this section is extremely useful for taxpayers, it also has some limitations.

First and foremost, the limitation in this section is the amount of 1.5 lakhs, which was last revised in 2014.

This amount has remained constant over the years, and many people feel that this amount is no longer sufficient.

In some cases, even paying the premium for your life insurance policy, the principal for your home loan, and the tuition fees for your children's education can exhaust the entire amount.

Another limitation of this section is that the benefits of this section are not applicable in the new tax regime.

Due to this limitation as well, taxpayers are forced to choose between the old and the new tax regime, which is more beneficial for them.

Final Thoughts

Making investments under Section 80C is one of the best and safest options for taxpayers to save their taxes and invest for the long term. A taxpayer has a wide range of options to choose from according to their needs and requirements. Are you a conservative person who wants to invest in government schemes like PPF and NSC, or a bold person who wants to invest in the stock market through ELSS schemes? The options are wide for everyone under Section 80C.

However, the key point is to start making investments as early as possible during the financial year. This not only helps you save your taxes at the end of the financial year but also gives your investments a chance to grow.

Instead of making investments during the last month of the financial year, i.e., March, it is always advisable to spread the investments throughout the year and create a diversified portfolio. With the help of investments under Section 80C, not only can you save your taxes, but also achieve your financial objectives.

FAQs

1. Can I invest in multiple Section 80C options in the same year?

You may invest in multiple options under Section 80C investments; however, the total deduction that you claim should not exceed ₹1.5 lakh in a financial year.

2. Are joint investments eligible for Section 80C deduction?

Yes, they are eligible; however, the deduction is available only to the person who actually makes the payment or earns the income from investment.

3. What if I withdraw my investment before the lock-in period ends?

Normally, if you withdraw your investment before the lock-in period ends, you may lose the tax benefits, and the tax deduction you have already taken may become taxable.

4. Does the interest earned on Section 80C investments become taxable?

The tax implications vary for different types of investments under Section 80C; however, for some investments, such as PPF, the returns are tax-free.

5. Can NRIs claim deductions under Section 80C?

Yes, NRIs may claim deductions for eligible Section 80C investments.

6. Can both spouses claim deductions for the same investment?

No, you may claim a deduction for a tax-saving investment under Section 80C if you have actually invested the amount.

7. What is the last date to make Section 80C investments?

You must complete all eligible Section 80C investments on or before March 31 of the financial year to claim deductions.

8. Does EPF contribution count towards the ₹1.5 lakh limit?

Yes, your employee contribution to EPF is included within the ₹1.5 lakh limit for investments under Section 80C.

Disclaimer

Please consult a qualified financial advisor for personalised advice. This article is for informational purposes only and does not constitute financial advice.

Related Blogs

Published on Mar 27, 2026

HRA Exemption: How Salaried Indians Can Claim It and Avoid Common Mistakes

Learn how HRA exemption works, how to calculate it, and common mistakes salaried Indians make. Step-by-step guide with examples for FY 2025-26.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 25, 2026

How to File ITR-1 (Sahaj) Online in 2026: Step-by-Step Guide for Salaried Employees

Learn how to file ITR-1 (Sahaj) online in 2026 with this simple step-by-step guide for salaried employees. Avoid errors, claim deductions, and file easily.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 09, 2026

New Tax Regime vs Old Tax Regime: A Real-Numbers Comparison for Salaried Indians (FY 2025-26)

New vs old tax regime FY 2025-26 — compare real tax on ₹6L, ₹10L & ₹15L salaries. See who pays zero tax and find your break-even point.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ