BHIM App vs GPay vs PhonePe vs Paytm: Which UPI App Should You Use in 2026?

Confused between BHIM, Google Pay, PhonePe or Paytm, this in-depth guide explains differences, pros and cons, and helps you choose the best UPI app in India based on your usage.

Arjun Sharma

Content Lead – Banking & Payments

10 min read

Table of Contents

Imagine this: four friends are sitting at a restaurant. When they get the bill, everyone takes out their phones to pay via the UPI application. However, it was seen that none of them used the same app. One person used Google Pay, another used PhonePe, a third one had Paytm, and then there is always that one friend who uses BHIM UPI.

All these UPI apps function pretty much the same, but they pay instantly using UPI. Today, these apps do much more than just transfer or receive money. They help in additional facilities like buying insurance, paying bills, and even investing. In this blog, we will look into the basis of UPI, what its pros and cons are, and which one to choose for your daily needs. So, let’s get going!

Understanding UPI

To talk about in literal terms, UPI is an electronic link between bank accounts. It helps users to transfer funds directly from their bank account to another person's. With UPI, you need not remember those long IFSC codes or account numbers. Instead, you can simply enter your phone number, scan a QR code, or use a UPI ID. It was developed by the National Payments Corporation of India (NPCI) as an initiative to digitalise the payment mechanism of the country. Additionally, UPI is compatible with several apps. This means that you can send money to someone who uses Paytm or PhonePe using Google Pay without any issue.

UPI Limits and Rules

To prevent fraud and keep your transactions secure, banks put a limit on UPI payments.

For any one-time payment, the upper limit is ₹1 lakh. However, this can vary depending on which bank you're with. For a 24-hour time-frame, whether you're using PhonePe, Google Pay, Paytm, or any other UPI app, everything adds up to a combined daily limit of around ₹1-2 lakh on your account.

There's also a rule on how many times you can pay in a day. Usually, a user can make between 10 - 20 transactions in a day. If you hit that number, you will have to wait for 24 hours to make your next transaction.

If your account is new, expect things to be a little more restricted in the first 24 hours of activation. Banks do this to prevent scammers from opening accounts and immediately moving large amounts of money.

One thing people often overlook is when someone sends you a collect request, and you approve it, that still counts against your daily limit. So, if you're approving several of those in a day, your limit can quietly drain faster than you'd expect. We advise our customers to be mindful with their transactions!

Different UPI Apps

Let’s look into the different UPI applications you can choose from.

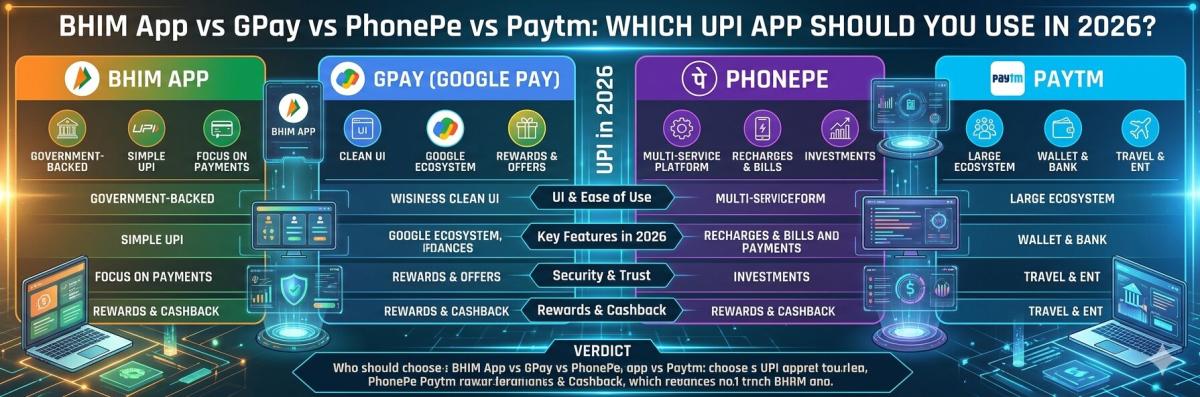

BHIM

BHIM was India's first UPI application. It's reliable, but not as fancy as others.

Pros:

- Backed by the government

- No advertisements

- Works great on inexpensive phones or slow internet

- Easy for beginners

- User-friendly interface

- Highly safe

Cons:

- Basic features only

- Old interface

- No extras like investments

Best for?

- It is highly functional for people who have just begun their digital payments journey and want a simple-use application.

- It has been ideal for people who just want to send or receive money without.

Google Pay (GPay)

Google Pay functions as a secure digital wallet system together with a payment solution which enables users to make contactless payments and conduct online transactions through mobile applications.

Pros

- Very easy to set up and link your bank

- Payments are fast and secure

- Clean interface with less confusion

- Gives scratch cards and rewards for making users come back to the app

Cons

- Fewer features like investment options

- Cashback is not as good as before

- No wallet for small payments

- No extra services like ticket booking

Best for

- It is best for people who want a simple app for daily payments like bills and money transfer, without any confusion.

- Teens aged 13-18 who make use of Google Pay for peer-to-peer payments and in-store purchases in a managed environment.

PhonePe

PhonePe is backed by Walmart. It is not just for sending money. People used this app for multiple uses.

Advantages

- Send money, recharge, and pay bills

- Buy gold or invest money

- Pay at shops using QR code

- Available in many Indian languages

Disadvantages

- App can be slow on old phones

- Too many options on screen

- Many notifications

- Can be confusing at first

It is best for users who want one app for all daily payments and services, while getting to experience safety in payments.

Paytm

Paytm , which is Pay Through Mobile, is one of the oldest payment apps in India. It is run by One97 Communications.

Pros

- Works easily at commercial outlets

- Pay bills and recharge

- Book tickets

- Invest in gold or mutual funds

Cons

- App looks a bit crowded

- Too many messages and offers cause irritation to customers

- Some people don’t fully trust it

- Can be slow on old phones

Best for?

Good for shopkeepers and people who do many types of payments. You can do everything in one app.

Which UPI App is Best for You?

So far, we have seen the key features, pros & cons of each app, but the question of which app is better is still unanswered.

Is there any single winner that we can use?

Actually if you’re looking for single winner then unfortunately there is none because choice of the best UPI app entirely depends less on the many features and more on how you actually want to use it in daily life:

- Best for Simple Payments: For simple payments involving sending and receiving money through UPI, BHIM would be ideal because it does not have lots of clutter, and overall experience is simple and reliable for everyday use.

- Best for Clean Experience: In case the need or want in digital payments is just a smooth and minimal interface then Google Pay is the perfect choice. It balances simplicity with usability, loads quickly, and does not overwhelm users with too many features.

- Best for All-in-One Finance: If the need is beyond just payments then PhonePe can be considered as the preferred one. It combines UPI transfers with bill payments, investments, and other financial services.

- Best for Wallet + Business Use: In case the need is both wallet and bank payment flexibility then Paytm might be appropriate. It is also used by small business owners who handle daily transactions, QR payments, and additional services like FASTag or bookings.

Can You Use Multiple UPI Apps? Should You?

There is no such restriction on use of multiple UPI apps because majorly these apps run on the same UPI infrastructure means accounts can be linked across BHIM, Google Pay, PhonePe, and Paytm at the same time. But multiple UPI apps may leave you feeling cluttered because it creates unnecessary friction as payment history gets scattered, notifications come from different platforms, and it becomes harder to track transactions or resolve issues in daily use.

On the other hand, just using only one UPI app is not also good because of downtimes which are a result of situations like bank server issues, app-specific glitches etc can interrupt transactions when we need them most.

That’s why practical approach would work in real life:

- For all routine transactions use only a single primary app

- Keep backup app so in case of primary fails we can use backup

- Regarding more than two, do it only if it is absolutely necessary

- Only consider using different apps when you’re actively utilising their special features

Some Common UPI Issues

These are some common UPI issues which many of us users face while using UPI apps. The prominent ones are-

- Payment Failed but Money Debited: Sometimes when we make payments it gets debited from the bank but transaction shows failed, this amount debited usually reversed automatically within a few minutes to a few hours only in some cases it may take up to 48 hours depending on the bank.

- Unable to Send Money: Under UPI there is a daily limit threshold so if we already crossed that then high chances are further transactions would fail and other reasons could be incorrect UPI PIN attempts, or temporary bank server downtime etc.

- Incorrect Payment Sent: In case if we accidently transfer money to the wrong person then there is no option of direct reversal. The only solution is to contact the recipient or raise a complaint through the app and bank support.

- UPI ID Not Found or Invalid: This usually happens when the UPI ID is typed wrong or is no longer active. It’s always better to double-check the UPI ID or confirm it with the receiver before sending money.

Conclusion

There is no single best UPI app for everyone. Different apps work well for different people. The best choice depends on how you use it daily.

For most people, it is a good idea to use one main UPI app and keep another one as backup. What really matters is ease of use, reliability, and acceptance, not just rewards or extra features.

FAQS

1. Which is the safest UPI app in India?

All major UPI apps like BHIM, Google Pay, PhonePe, and Paytm are safe. They all follow rules set by RBI and NPCI. Safety mostly depends on how carefully you use the app, like keeping your UPI PIN safe and checking details before paying.

2. Is BHIM better than Google Pay?

BHIM is simple and easy to use, with fewer distractions. Google Pay has a more modern and smooth experience. So, it depends on what you prefer.

3. Which UPI app gives the best cashback in 2026?

There is no app that always gives high cashback now. Rewards are less common and mostly based on offers. You can still check apps like PhonePe and Paytm for deals sometimes.

4. I’ve only a single bank account but I want to use multiple apps so can I do so?

Yes, there is no restriction. We can absolutely link the same bank account across multiple UPI apps which will allow us freely switching between apps.

5. I’ve started my small business so which UPI app I can consider as the best UPI app for me?

Generally for small business owners the best UPI app is PhonePe and Paytm because they offer strong merchant networks, QR-based payment systems, and additional tools that help manage daily transactions more efficiently while other UPI apps can also be used but these 2 are often used by many individuals for their small businesses.

6. Is UPI completely free or do they charge any fees for transactions?

In day to day life majorly UPI transactions between individuals are free of cost. Only in some cases such as merchant payments or value-added services may involve charges which will also depend on the platform or policies of the bank.

7. I’ve seen many people saying transactions failed so why do UPI payments sometimes fail?

Failure in UPI payments sometimes happens due to reasons like bank server downtime, poor internet connectivity, or temporary technical issues within the app. These are the reasons people suggest keeping a backup app for such situations.

8. I’m just a beginner, so which one UPI app is best for me?

In case if you’re just starting to use them at this initial phase the best option would be to use either Google Pay or BHIM because these 2 have a clean interface and are simple.

Related Blogs

Published on May 06, 2026

Role of Middleware in Banking Transaction Systems

Discover the role of middleware in banking transaction systems, enabling real-time processing, secure integration, and seamless communication between banking platforms.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 28, 2026

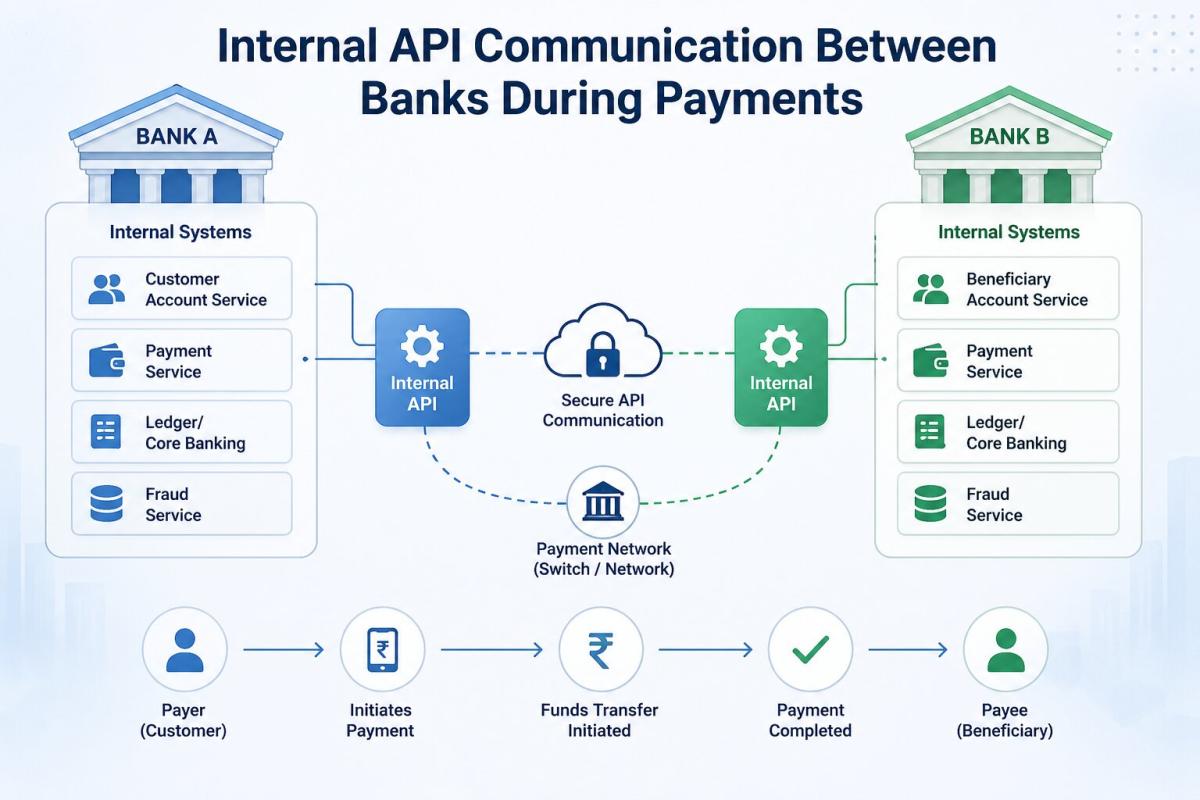

Internal API Communication Between Banks During Payments

Understand how internal API communication between banks powers digital payments, enabling real-time transaction processing, secure data exchange, and seamless fund transfers.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 28, 2026

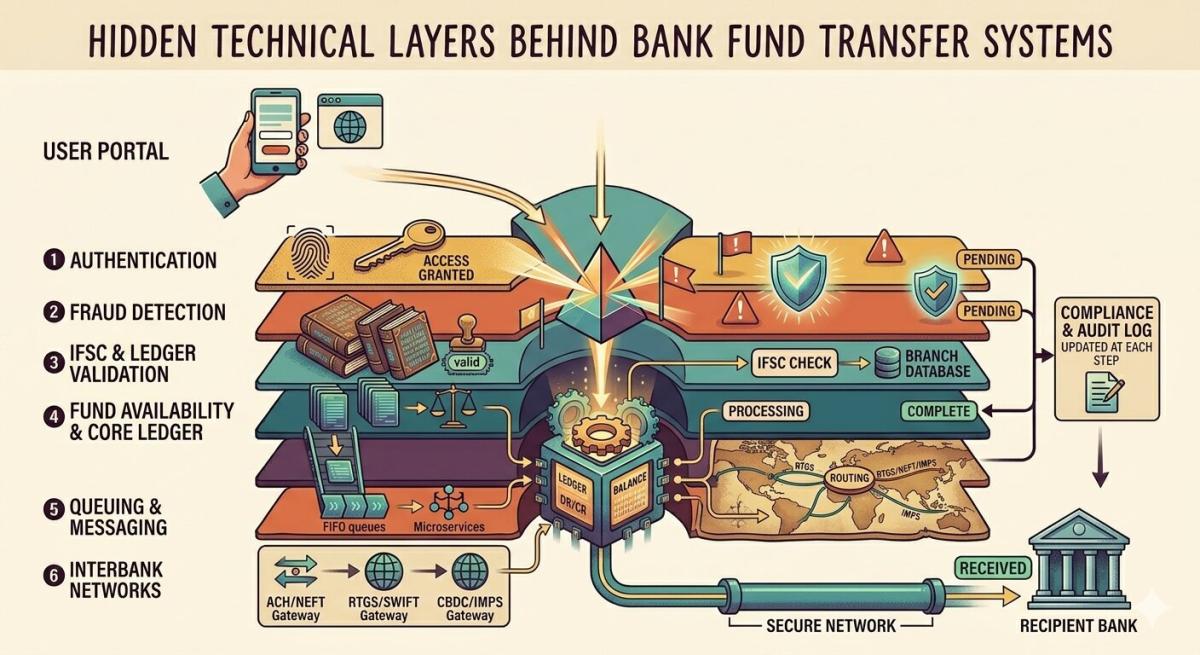

Hidden Technical Layers Behind Bank Fund Transfer Systems

Explore the hidden technical layers behind bank fund transfer systems, including SWIFT messaging, clearing, settlement, APIs, and security frameworks that power modern digital payments.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 28, 2026

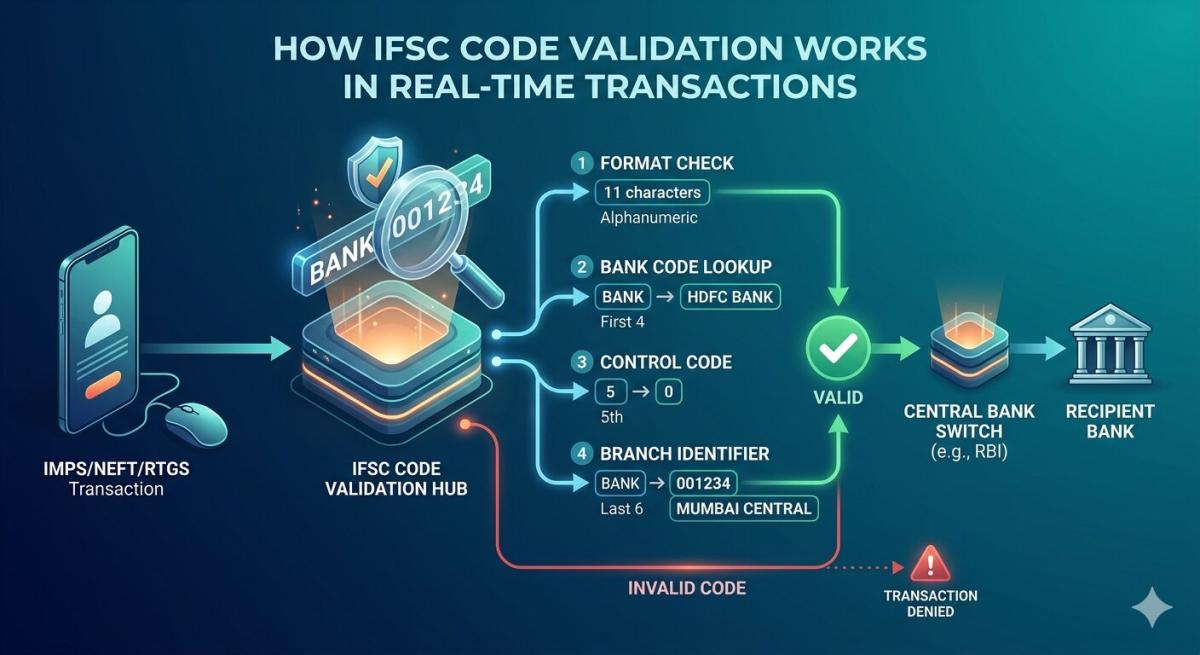

How IFSC Code Validation Works in Real-Time Transactions

Learn how IFSC code validation works in real time across NEFT, RTGS, and IMPS transactions. Discover its role in ensuring accurate, secure, and efficient fund transfers in digital banking.

Arjun Sharma

Content Lead – Banking & Payments

Published on Apr 28, 2026

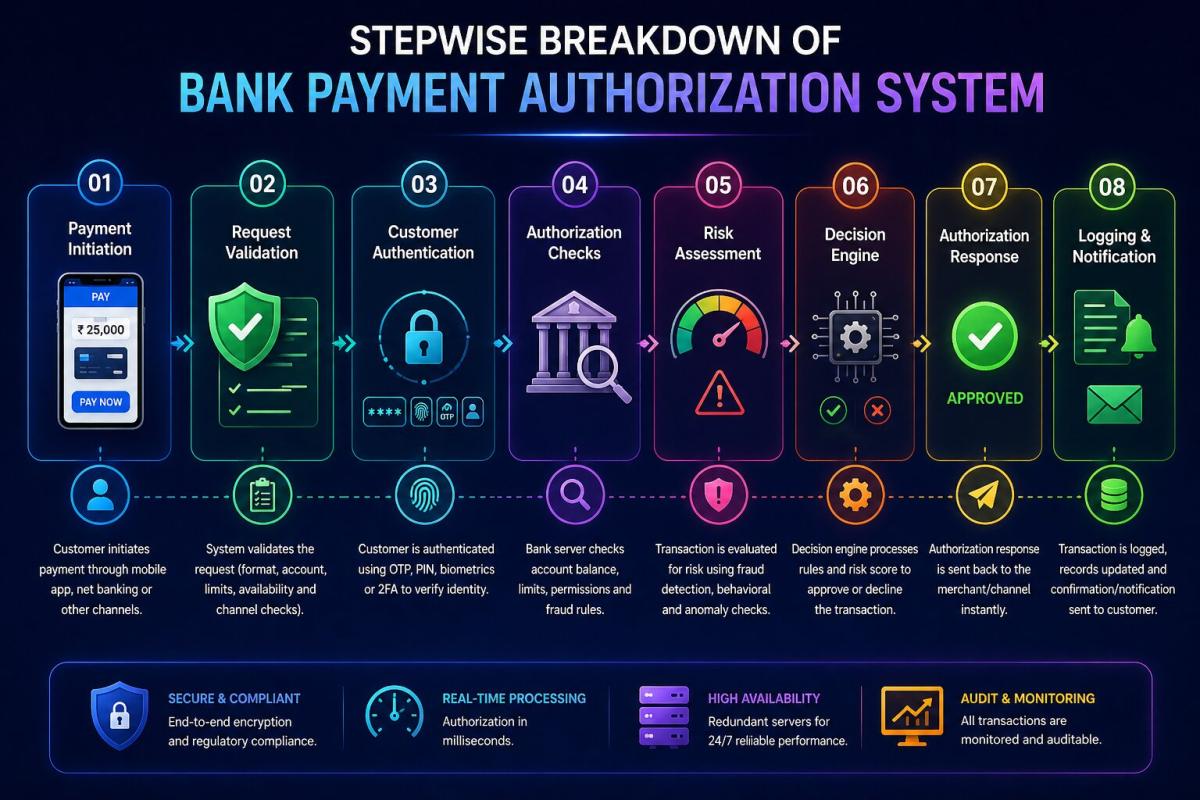

Stepwise Breakdown of Bank Payment Authorization System

Understand the step-by-step bank payment authorization process, including encryption, routing, verification, and approval mechanisms that ensure secure digital transactions.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ