Monthly EMI Calculation Explained: Everything You Must Know

Understand how monthly EMI calculation works with formulas and examples. Use EMI calculators to plan loans better and manage repayments efficiently.

Table of Contents

The credit market has been growing gradually in India over the years. This market is ranked as the 4th largest credit industry in the world with a year-on-year compounded annual growth rate greater than 11%. Loans have become a necessity in everyone’s life because of the current fast pace of life.

Whether it is for a house, a car or education, loans enable us to realize our dreams without having to save for years. Another important factor that defines a loan is the Equated Monthly Installment (EMI), which represents a fixed amount paid by debtors to lenders on a specific date of each calendar month. Discover the usage of loan EMI calculators and how to use them.

What is EMI?

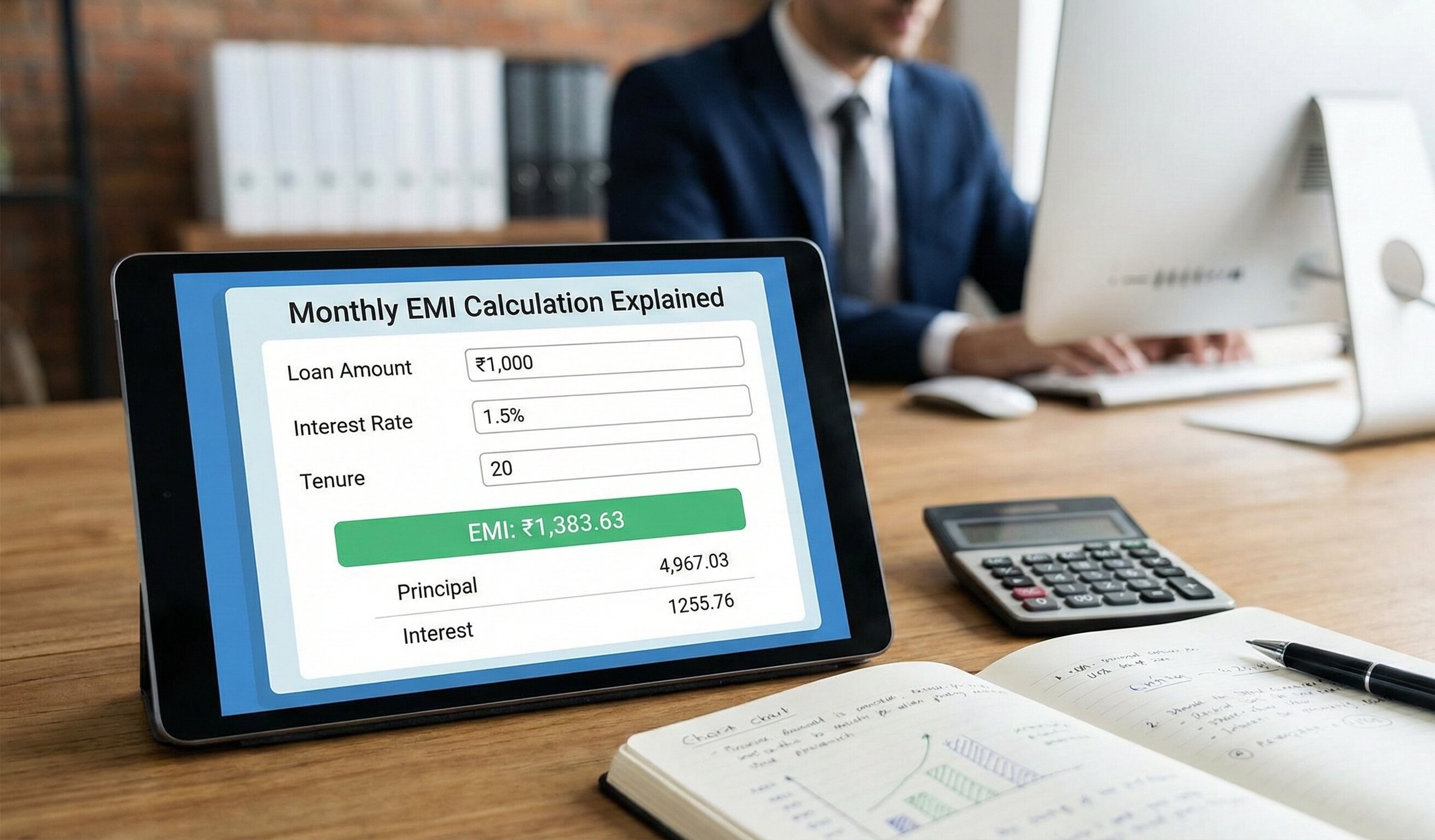

Monthly EMI is a periodic and fixed repayment done by a borrower to the lender on a particular date every month. It is used to reduce both the principal sum and interest on a loan, progressively. The EMI calculation considers three main factors: loan amount, interest rate, and loan period. These variables are used when determining the EMI in a complex formula used by the lenders.

EMI calculation is important for borrowers to determine their ability to repay and choose between different loans. Even if EMI looks complicated in terms of math, online resources such as monthly EMI calculators help you approximate your monthly installments before going for a loan.

How does EMI calculation work?

EMIs are different from variable payment plans where the borrower is free to pay a higher amount as per his choice. In EMI plans, borrowers are usually allowed only one fixed installment each month.

The advantage of an EMI to borrowers is that they are fully aware of how much they would be expected to pay on their loan every month hence making personal planning easier. The advantage to lenders (or the investor who buys the loan) is that they receive a predictable, regular stream of income from the interest paid on the loan.

The EMI can be computed using the flat rate method or the reducing-balance method, also known as the reduce-balance method.

Monthly EMI Calculation Formula

The EMI flat-rate formula is calculated by summing up the principal loan amount and the interest on the principal and then dividing the sum by the number of periods multiplied by several months.

EMI = P * [( r * (1 + r)^n)) / ((1 + r)^n – 1)]

where:

- P refers to the principal amount borrowed

- r refers to the periodic monthly interest rate

- n refers to the total number of monthly payments

EMI = P * [( r * (1 + r)^n ) / ((1 + r)^n - 1)]

Monthly EMI Calculation Example

Let's assume:

- P = ₹10,00,000 (10 lakh rupees)

- Annual interest rate = 9%

- Loan tenure = 5 years (60 months)

Step 1: Determine the monthly interest rate (r)

r = (9. 6 / 12) / 100 = 0.008

Step 2: Determine the number of installments (n)

n = 5 * 12 = 60 months

Step 3: Use the formula

EMI = 10,00,000 * [(0. 008 * (1 + 0. 008)^60) / ((1 + 0. 008)^60 – 1)]

= 10,00,000 * [0. 0128 / 0. 6151]

= 10,00,000 * 0. 0208

= 20,800

Thus, the EMI would be ₹20,800 (rounded to the nearest rupee). This means the borrower would need to pay ₹20,800 per month for 60 months to repay the loan of ₹10,00,000 at 9%. Compound interest of 6% per year for 5 years.

Factors that Affect Monthly EMI Calculation

During monthly EMI calculation, you must consider all these factors that greatly influence the EMIs:

- Loan Amount (Principal): It's the actual sum of money that has been borrowed out in the form of a loan. As a rule, loans with greater amounts mean greater EMIs.

- Interest Rate: This is the percentage of interest charged on the particular loan advanced to the borrower. A higher rate of interest increases the EMI amount. This means that interest can be fixed or can float and this impacts the EMIs in various ways over time.

- Loan Tenure: It's the time frame within which the borrowed amount is to be paid back. Longer tenure leads to a lower EMI but a higher amount of interest to be paid throughout the loan period, while a short tenure leads to a higher EMI but lower interest to be paid for the same period.

- Fixed Interest Rate: It stays fixed for the entire period of the loan, so the EMI remains the same.

- Floating Interest Rate: It frequently changes with the market interest rates to adjust the EMI.

- Down Payment: It's the first payment that was made at the beginning of the transaction. A higher down payment means that the amount of loan required is lower and therefore leads to lower EMIs.

- Prepayments and Part-Payments: Bills that are settled before the expected date of payment. Prepayments help in recovering the principal amount and this has the effect of either shortening the tenure of the loan or reducing the EMI as per the lender’s guidelines.

How Do Online Monthly EMI Calculators Help?

In either a secured or an unsecured loan, you must have an idea of how much installment you have to pay per month before you apply for it. It is at this juncture that a monthly EMI calculator in India can be of immense help.

- It assists you in estimating the right EMI amount that you need to pay for the loan so that you can budget accordingly. To increase your chances of loan approval, be sure that your debt-to-income ratio is below 50%.

- A calculator also assists in saving your precious time. There is no need to perform long calculations by hand, which is very tiresome, especially for big numbers.

- It eliminates the possibility of a wrong calculation, and you are given a correct estimation each time.

- The monthly EMI calculators are highly specific for each type of loan. The process of breaking up a home loan EMI, for instance, is not the same as that of a personal loan EMI.

Conclusion

It is important that you calculate the monthly EMI when it comes to repaying loans. With knowledge of the formula and the factors that constitute it, debtors can manage their finances efficiently. Correct EMI estimations assist in comparing various loan options and make the lending more affordable and non-stressful.

This can be easily done with the help of currently available tools such as EMI calculators or simple formulas in the spreadsheet showing clear repayment tables and interest payments. Therefore, understanding EMI calculations enables people to be wise while borrowing money and to manage their finances while repaying the loan.

Related Blogs

Published on Mar 25, 2026

CIBIL Score Explained: What It Is, How It Is Calculated, and How to Improve It

Learn how Credit Information Bureau (India) Limited scores impact your loans. Discover how CIBIL is calculated, why it matters, and tips to improve your credit.

Arjun Sharma

Content Lead – Banking & Payments

Published on May 18, 2025

Tips on How to Calculate Monthly EMI for Any Loan

Struggling to understand your EMI amount? This blog covers all the necessary tips on how to calculate your monthly EMI to help you stay ahead of your finances.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 25, 2025

Monthly EMI Calculators: A Detailed Overview

Monthly EMI calculators allow you to get a pre-hand idea of the EMI you must pay monthly. In return, an EMI calculator per month helps manage monthly finances better.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 02, 2025

Buying a Car? Here's How to Use a Vehicle EMI Calculator the Smart Way

Plan your car or bike loan with ease. Learn how to use a vehicle EMI calculator, input values correctly, and get accurate monthly EMI instantly.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Feb 17, 2025

Master EMI Calculators: How to Estimate Your Monthly Payments with Ease

Learn how EMI calculators work to estimate monthly payments accurately. Explore EMI formulas, examples, and factors to make smart financial decisions.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ