HRA Exemption: How Salaried Indians Can Claim It and Avoid Common Mistakes

Learn how HRA exemption works, how to calculate it, and common mistakes salaried Indians make. Step-by-step guide with examples for FY 2025-26.

Priya Nair

Senior Compliance Editor at IFSC.co

13 min read

Table of Contents

- What is House Rent Allowance (HRA)?

- Who Can Claim HRA?

- How to Calculate HRA Exemption (Step-by-Step)

- Metro vs Non-Metro Cities (Important Difference)

- Step-by-Step HRA Calculation Example

- How to Claim HRA Exemption While Filing Income Tax Return (ITR)

- Common HRA Mistakes That Can Trigger Tax Notices

- HRA Rules for Special Cases

- HRA - Old Tax Regime vs New Tax Regime?

- HRA Exemption Summary

- Conclusion

- FAQs

If you're a salaried individual living on rental premises and your employer pays you House Rent Allowance (HRA) then you should know that it can reduce your tax liability. But the rules of HRA are sometimes often misunderstood and difficult to apply in real life. That’s why many individuals who receive HRA either fail to claim it correctly or end up claiming less than what they are eligible for.

In this blog, we’ll understand HRA in a simple and practical way, covering how it is calculated, how you can claim it correctly, and the common mistakes you should avoid in the process.

What is House Rent Allowance (HRA)?

House Rent Allowance also known as HRA is actually a component of your salary that employers provide to its employees for helping them cover the cost of rented accommodation. Don’t think it’s just another part of your payslip, it actually plays a significant role in reducing your taxable income if you understand how to use it correctly.

This HRA you receive can be claimed as a tax exemption under Section 10(13A) of the Income Tax Act, which means you do not have to pay tax on this part of your income making it one of the most accessible and practical tax-saving tools available to salaried individuals in India.

Who Can Claim HRA?

If you’re receiving HRA then you cannot by default claim HRA exemption, only you can claim if you satisfy all the following key conditions of HRA:

- HRA must be part of your salary structure: In case, if your salary does not include any HRA component then unfortunately you cannot claim this exemption even if you are paying rent

- You must be paying rent regularly: Second requirement is you must be living in a rented house and this is not enough you also have to make and maintain clear record of rent payment

- You cannot claim HRA for your own house: It’s usual that if you are living in a house that you own meaning that you are not paying any rent thus this exemption is not applicable

- Rent payment should be reasonable and justifiable: If you are paying unreasonable or Inflated or did fake rent arrangements then you should know this that it can lead to scrutiny or notices from the tax department

How to Calculate HRA Exemption (Step-by-Step)

One thing to note here is that HRA you have received is not fully allowed as exemption, instead there is a specific formula given by the Income Tax Department for calculating allowed exemption out of total HRA received.

The HRA Calculation Formula

Your HRA exemption is the minimum of these three:

- Actual HRA you got the employer

- 50% of salary* (for metro cities) or 40% (for non-metro cities)

- Rent paid minus 10% of salary*

*What Counts as Salary for HRA?

For the purpose of HRA here “salary” does not mean your actual total salary is what you received which is not correct and can lead to wrong calculations.

Here salary includes:

- Basic salary

- Dearness allowance (only if it forms part of retirement benefits)

- Commission as a percentage of turnover

Note: this salary does not include any kind of bonuses, incentives, or other allowances

Metro vs Non-Metro Cities (Important Difference)

Where you live on a rental basis is also important in HRA calculation because the salary percentage changes depending on the city, which is especially relevant for people living in Tier 2 and Tier 3 cities

|

Category |

Cities Included |

Salary Consideration |

|

Metro Cities |

Mumbai, Delhi, Chennai, Kolkata |

50% of salary |

|

Non-Metro Cities |

All other cities |

40% of salary |

Step-by-Step HRA Calculation Example

Let’s understand this with a realistic example so that the formula becomes easier to apply in your own case without confusion

Assumptions:

- Basic Salary = ₹50,000/month

- HRA Received = ₹20,000/month

- Rent Paid = ₹18,000/month

- City = Mumbai (Metro)

Step 1: Calculate all three components

- Actual HRA received = ₹20,000

- 50% of salary (metro city)

→ 50% of ₹50,000 = ₹25,000 - Rent paid – 10% of salary

→ ₹18,000 – ₹5,000 = ₹13,000

Step 2: Find the lowest value

- ₹20,000

- ₹25,000

- ₹13,000

Lowest = ₹13,000

Since the lowest value is ₹13,000 this will be exempted from the taxes, and the remaining HRA will be taxed as usual like your taxable income.

→ Refer to this HRA calculator provided by the Income tax Dept. for calculating your own HRA.

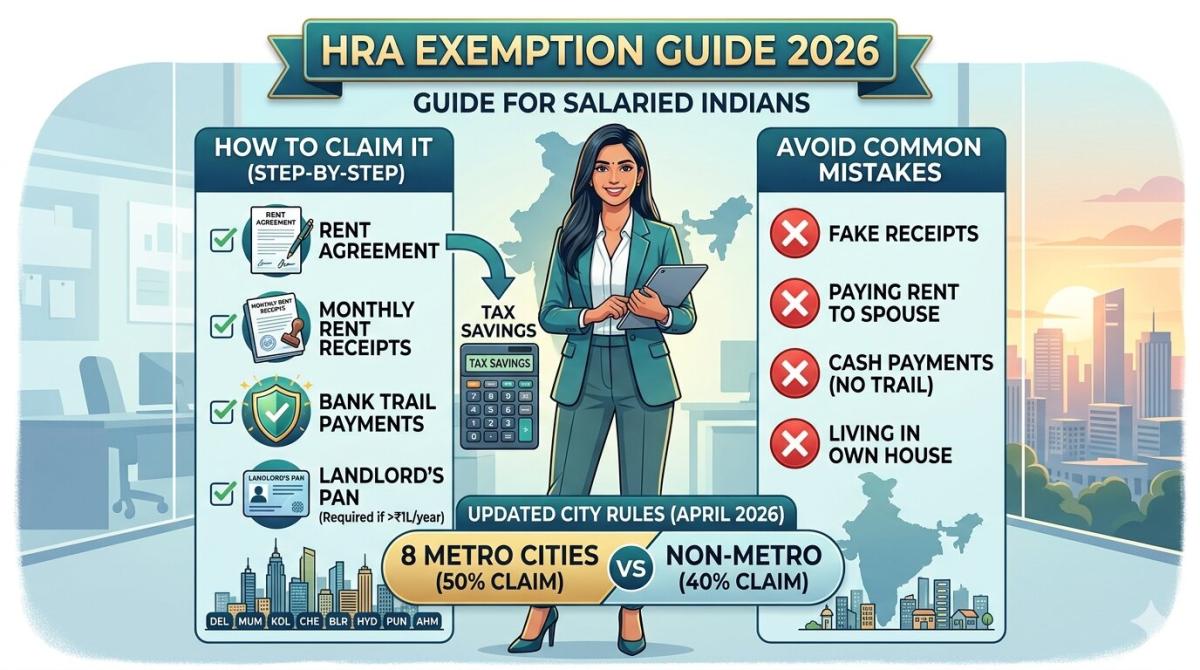

How to Claim HRA Exemption While Filing Income Tax Return (ITR)

Understanding the calculation is only half the job, because even if your HRA is correctly structured in your salary, you still need to follow the proper process while submitting documents and filing your ITR.

To make things simple, here’s how the process typically works from salary stage to ITR filing:

- Submit rent details to your employer: During the financial year, you need to declare your rent payments and provide basic details so that your employer can consider HRA exemption while calculating TDS.

- Provide rent receipts: Employers usually ask for rent receipts as proof, especially towards the end of the financial year, and these should include details like amount, duration, and landlord’s name.

- Submit landlord’s PAN (if required): If your annual rent exceeds ₹1,00,000, you must provide your landlord’s PAN, otherwise your employer may not allow full exemption.

- Check Form 16 carefully: Once your employer issues Form 16, verify whether the HRA exemption has been correctly calculated and reflected.

- Report correctly while filing ITR: While filing your income tax return, ensure that the HRA exemption matches your Form 16 or is corrected if something was missed earlier.

Common HRA Mistakes That Can Trigger Tax Notices

These are mistakes often made by many taxpayers and sometimes these errors not only reduce your tax savings but in some cases can even attract scrutiny from the Income Tax Department if the claim looks incorrect or unsupported.

Thus, understanding these mistakes in advance can help you avoid unnecessary trouble and ensure that your HRA claim remains clean, valid, and fully compliant.

1. Claiming HRA Without Actually Paying Rent

One of the most common mistakes is claiming HRA exemption without actually paying rent, which may seem harmless to some people but can become a serious issue if your claim is ever reviewed because there will be no proof to support it.

Thus, remember, if there is no real rent transaction, the exemption is not valid.

2. Paying Rent in Cash Without Proper Proof

Many people pay rent in cash and do not maintain proper receipts or documentation, which creates a problem later because without evidence, it becomes difficult to justify your claim if questioned.

Therefore, always keep signed rent receipts and preferably use bank transfers to maintain a clear record.

3. Not Providing Landlord’s PAN

If your annual rent exceeds ₹1,00,000 and you fail to provide your landlord’s PAN then your employer may restrict your exemption, and even during ITR filing, this can create inconsistencies.

4. Claiming HRA and Home Loan Incorrectly

Some taxpayers assume they cannot claim both HRA and home loan benefits together, while others claim both without proper justification, and both approaches can lead to incorrect tax filing.

You can claim both, but only under valid conditions such as living in a rented house in a different city.

5. Wrong Metro vs Non-Metro Classification

Using the wrong city category while calculating HRA can lead to an incorrect exemption amount, especially because metro cities allow 50% of salary while non-metro cities allow only 40%.

HRA Rules for Special Cases

These are some special cases related to HRA such as you’re owning a house in one city while working in another or you’re trying to claim benefits even though you’re not getting any HRA in your salary.

Case-1: HRA + Home Loan Together

A very common myth is that you cannot claim HRA if you already have a home loan, but in reality, both benefits can be claimed together if certain conditions are met and your situation justifies it logically.

You can claim both HRA and home loan benefits if:

- your own house is in a different city from where you are currently working

- your workplace is far from your owned house

- which makes it reasonable to live on rent

- you have rented accommodation due to practical reasons like commute or job location

In such cases, HRA is claimed for rent and home loan benefits are claimed under other sections like interest and principal repayment.

Case-2: Section 80GG – The Alternative to HRA

Under Section 80GG of the Income Tax Act, individuals who do not receive HRA can still claim a deduction for rent paid, although the benefit is more limited and comes with stricter conditions.

To claim under 80GG:

- you should not receive HRA in your salary

- you, your spouse, or minor child should not own a house in the same location

- you must be paying rent for your accommodation

Under this deduction amount is subject to limits which is generally lower than HRA benefits.

Case-3: Living with Parents – Can You Claim HRA?

Yes, you can claim HRA while living with your parents, but it must be a genuine rental arrangement where you actually pay rent and maintain proper documentation.

To make this valid:

- must transfer rent regularly (try to prefer bank transaction)

- create a simple rental agreement

- ensure your parents actually declare this rent amount in their income tax return

Also note that without any proper documentation or any actual payment this claim may not hold up if the tax officer issued notice.

HRA - Old Tax Regime vs New Tax Regime?

Another point to note for us is that HRA exemption is not available under the New Tax Regime of Income Tax Act which means we have no tax benefit for the rent we will actually pay if we decided to opt for the new regime while filing the income tax return.

Here’s a brief comparison:

|

Feature |

Old Tax Regime |

New Tax Regime |

|

HRA Exemption |

Allowed |

Not allowed |

|

Other Deductions (80C, 80D, etc.) |

Allowed |

Mostly not allowed |

|

Tax Rates |

Higher |

Lower |

|

Best For |

People with deductions |

People with fewer deductions |

Should You Choose an Old or New Regime?

So the choice depends, if your rent is high and HRA exemption is significant then the old regime would be more beneficial because it will allow you to reduce your taxable income through multiple deductions.

Otherwise if you have minimal deductions and prefer simplicity then the only option is the new regime which might result in lower tax due to reduced tax rates.

The right choice will get to know after comparing both options before filing your return.

HRA Exemption Summary

- It reduces overall taxable income only if we’re paying rent and meeting the eligibility.

- Under this exemption is calculated by a 3-rule formula and the answer is usually the lowest value.

- For a valid claim proper documents like rent receipts and landlord PAN are must.

- Benefit of HRA as per income tax act is available only under the old tax regime.

Conclusion

At the end, it can be concluded that there is no doubt that when we first look at HRA exemption it feels complicated, but once we try to simplify by breaking it into multiple snippets like basic rules, how the calculation works and etc., then it becomes understandable that it is one of the easiest ways to legally reduce our tax liability without making any additional investments, especially if we’re already paying significant rent as part of our monthly expenses.

FAQs

1. Is the HRA I receive fully tax-free or just part of it?

Yes, exemption under HRA is not full ; only a certain portion which is calculated using the prescribed formula of section 10(13A) of income tax act is exempt and the remaining amount is added to the taxable income.

2. Due to some reasons I don’t have rent receipts. Does that mean I can’t claim HRA?

Rent receipts are generally required as proof of rent payment while your employer may accept basic declarations in some cases but it's good to keep proper receipts or payment records because they may be needed if your claim is reviewed later.

3. Can both husband and wife claim HRA?

Yes. Both husband and wife can freely claim HRA condition is if they are both salaried and receiving HRA as part of their salary also living rentally, but the arrangement should be genuine and properly documented to avoid any issues.

4. What happens if I don’t submit HRA proof to my employer?

If we’re not submitting any proof to the employer then initially they may not consider the HRA exemption in calculation of TDS deduction which means that more tax will be deducted from our salary but you should not worry because we can still claim the exemption later while filing the income tax return.

5. Due to my job I had to change the cities during a year, so, can I still claim HRA?

Yes, there is no such major impact you can claim HRA without worry even if you change cities during the financial year but calculation may vary depending on whether you lived in a metro or non-metro city during different periods so you may need to calculate it accordingly.

6. Can I claim HRA and 80GG together?

Unfortunately it is not possible to claim both HRA and Section 80GG at the same time because the benefit of 80GG is specifically for those individuals who are not getting any HRA that’s why you can only choose one based on your eligibility.

7. Instead of parents I want to pay rent to my relatives so can I still claim HRA?

Yes, if we want to we can do so but the transaction must be genuine with actual money transfer and proper documentation and most importantly the relative receiving the rent should report it as income in their tax return.

8. I’ve asked my landlord for a PAN but he refused. So, how will it affect the HRA exemption?

In case if the amount of annual rent is exceeding ₹1,00,000 then the PAN of the landlord is required but if he is not giving then your employer may restrict the exemption so it is better to request it or keep a written declaration, although this may still affect your claim.

Disclaimer: -

"This article is for informational purposes only and does not constitute financial advice. Please consult a qualified financial advisor for personalised guidance."

Related Blogs

Published on Mar 26, 2026

Section 80C Investments: Full List, ₹1.5 Lakh Limit, and Which Option Wins

Save tax with Section 80C investments. Explore the full list, ₹1.5 lakh limit, and compare options to choose the best tax-saving investment for you.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 25, 2026

How to File ITR-1 (Sahaj) Online in 2026: Step-by-Step Guide for Salaried Employees

Learn how to file ITR-1 (Sahaj) online in 2026 with this simple step-by-step guide for salaried employees. Avoid errors, claim deductions, and file easily.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Mar 09, 2026

New Tax Regime vs Old Tax Regime: A Real-Numbers Comparison for Salaried Indians (FY 2025-26)

New vs old tax regime FY 2025-26 — compare real tax on ₹6L, ₹10L & ₹15L salaries. See who pays zero tax and find your break-even point.

Arjun Sharma

Content Lead – Banking & Payments

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ