Active vs. Inactive IFSC Codes: What’s the Difference?

Is your IFSC code still valid? Learn the difference between active and inactive IFSC codes, why they change in 2026, and how to verify them to avoid failed payments.

Table of Contents

I remember a frantic afternoon just a few years ago, trying to transfer funds for an urgent medical bill. I had the account number, the beneficiary’s name, and what I thought was the correct IFSC code. Hit ‘send,’ and… nothing. The transaction failed repeatedly. It turned out the branch had recently merged, and the IFSC I was using was no longer valid. This frustrating experience highlighted a critical, yet often overlooked, aspect of digital banking: the difference between active and inactive IFSC codes. Understanding this distinction isn’t just about avoiding transaction failures; it’s about ensuring your financial operations run smoothly and securely in an increasingly interconnected world.

The Core Purpose of an IFSC Code

At its heart, the Indian Financial System Code (IFSC) is an eleven-character alphanumeric code uniquely identifying every bank branch participating in India’s online money transfer systems. Think of it as a digital address for your bank branch, essential for facilitating NEFT, RTGS, and IMPS transactions. Without a correct and active IFSC, funds simply cannot be routed to their intended destination. It acts as a crucial identifier, ensuring that when you send money, it reaches the exact branch and account, rather than getting lost in the vast network of Indian banking.

Each character within the IFSC holds significance: the first four identify the bank, the fifth character is always zero (reserved for future use), and the last six characters pinpoint the specific branch. This structured format provides an unparalleled level of precision, preventing misdirected payments and enhancing the overall security of digital transactions. The Reserve Bank of India (RBI) mandates its use, underpinning its importance in the nation’s financial infrastructure. For instance, if you’re planning a major financial transfer in early 2026, verifying the IFSC will be your first critical step.

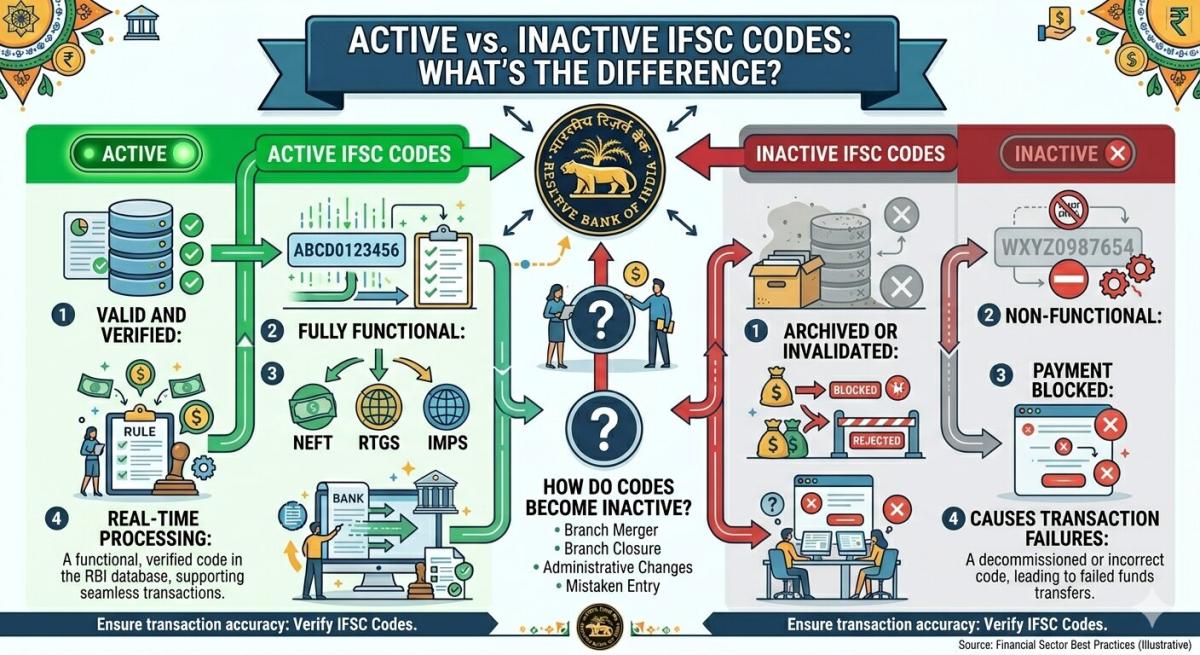

Understanding an Active IFSC Code

An active IFSC code signifies that the associated bank branch is fully operational and participating in the RBI’s electronic funds transfer systems. When you use an active IFSC, your NEFT, RTGS, or IMPS transactions will process without a hitch, assuming all other details like account number and beneficiary name are also correct. This is the state you want your recipient’s IFSC to be in. It means the branch is open for business, its systems are integrated with the central clearing house, and it’s ready to receive or disburse funds digitally.

The status of an IFSC code being active is dynamic and maintained by the respective banks in conjunction with the RBI. Banks regularly update their branch information, including IFSC codes, especially when branches open, close, merge, or relocate. For the average user, an active IFSC means reliability and immediate transaction processing. It’s the standard, expected state for any bank branch you intend to interact with financially, ensuring that your digital payments are handled efficiently and effectively, reaching their target account in real-time or near real-time.

The Inactive IFSC: A Digital Dead End

An inactive IFSC code, on the other hand, indicates that the corresponding bank branch is no longer participating in electronic funds transfer systems under that specific code. This could be due to several reasons: the branch might have closed down, merged with another branch, or relocated, acquiring a new IFSC. Attempting to use an inactive IFSC for any digital transaction will invariably lead to failure. The payment will bounce back, often with a message indicating an invalid or incorrect IFSC, causing delays and frustration.

The implications of an inactive IFSC are significant. Beyond failed transactions, it can lead to missed deadlines, penalties for late payments, and even reputational damage for businesses. Imagine trying to pay a supplier or disburse employee salaries using an outdated code; the ripple effects can be substantial. It’s a digital roadblock that highlights the critical need for vigilance in verifying financial details, especially when dealing with new beneficiaries or branches that might have undergone recent changes. Always confirm the IFSC code, particularly if you haven’t transacted with that specific branch recently.

Why IFSC Status Matters for You

The difference between active and inactive IFSC codes is far more than a technicality; it directly impacts your ability to conduct seamless financial transactions. Using an active IFSC ensures your payments are processed efficiently, reaching their destination without delays. This is crucial for time-sensitive transactions like loan EMIs, bill payments, or urgent transfers to family. An active code provides peace of mind, knowing your money is moving through established, verified channels as intended, maintaining the flow of your personal or business finances.

Conversely, encountering an inactive IFSC can trigger a cascade of problems. Beyond the immediate inconvenience of a failed transaction, it can lead to financial penalties for late payments, missed business opportunities, and considerable stress. For instance, if you’re a small business owner relying on timely payments from clients, an incorrect IFSC could hold up crucial revenue. It underscores the importance of not just having an IFSC, but having the correct and active IFSC, a detail that can make or break the success of your digital money transfers.

Common Reasons for Inactivation

IFSC codes can become inactive for several reasons, primarily driven by structural changes within the banking sector. Bank mergers and acquisitions are major culprits; when two banks combine, their branches may be rationalized, leading to some branches closing or being absorbed, thus rendering their original IFSC codes obsolete. Similarly, branch relocations almost always result in a new IFSC being assigned. Sometimes, a bank might reorganize its internal branch network, consolidating operations, which also triggers changes. The RBI maintains an updated list of banks and their branches, which can be a useful resource for verification. For example, the official RBI website (RBI.org.in) often provides circulars on such changes.

How IFSC Status Changes and Verification

The process of an IFSC code becoming inactive is usually initiated by the bank itself, often following a branch merger, closure, or relocation. Once the change is implemented, the bank updates its records and informs the RBI, which then updates its central database. This information eventually propagates to payment systems. For example, if a branch closes down in late 2025, its IFSC will likely be marked inactive by early 2026, and any attempts to use it will fail. This systematic update ensures the integrity of the national payment infrastructure.

Verifying an IFSC code’s status is crucial before initiating any transaction. There are several reliable methods: checking the official bank website, using the bank’s mobile app, or consulting third-party financial portals that pull data directly from the RBI. Many banking apps now offer an IFSC lookup feature. If you have any doubt, contacting the beneficiary’s bank directly is the most definitive way to confirm. Always err on the side of caution; a few moments spent verifying can save hours of troubleshooting and potential financial loss.

Key Takeaways

- IFSC as a Digital Address: An IFSC is a unique 11-character code identifying bank branches for electronic fund transfers like NEFT, RTGS, and IMPS.

- Active vs. Inactive: An active IFSC means the branch is operational and participating in digital transactions; an inactive one means it’s no longer valid, leading to failed transfers.

- Causes of Inactivation: IFSC codes become inactive primarily due to bank mergers, branch closures, relocations, or internal restructuring.

- Verification is Key: Always verify the IFSC code through official bank channels or reliable third-party sites before initiating any transaction to avoid delays and financial inconvenience.

Frequently Asked Questions

Can an inactive IFSC code ever become active again?

Generally, no. Once an IFSC code is marked inactive, it is typically permanently retired. If a branch reopens or a new branch is established, it will usually be assigned a completely new IFSC code, rather than reactivating an old one. The banking system prioritizes unique identifiers for clarity and security.

What happens if I use an inactive IFSC code for a transaction?

If you use an inactive IFSC code, your transaction will almost certainly fail. The funds will not be debited from your account or, if debited, will be reversed and credited back to your account within a few hours to a few business days. You will typically receive an error message indicating an invalid or incorrect IFSC.

How can I find the correct and active IFSC code for a beneficiary?

The most reliable ways to find a correct and active IFSC code are to ask the beneficiary directly, check the beneficiary’s bank passbook or cheque leaf, use the official bank website’s branch locator, or utilize reliable third-party financial aggregators that source data from the RBI. Many bank mobile apps also offer an IFSC lookup feature.

Are all bank branches assigned an IFSC code?

Yes, every bank branch in India that participates in electronic funds transfer systems (NEFT, RTGS, IMPS) is assigned a unique IFSC code. This ensures that every digital transaction has a precise destination, maintaining the efficiency and accuracy of the national payment infrastructure.

Conclusion

The seemingly minor detail of an IFSC code’s active or inactive status holds immense power over your financial fluidity. My own experience taught me that vigilance is paramount. By understanding the critical difference between active and inactive codes, you empower yourself to navigate the digital banking landscape with confidence and efficiency. Always take a moment to verify; it’s a small investment of time that prevents significant headaches and ensures your money moves exactly where it’s intended, every single time, whether it’s today or in 2026.

Related Blogs

Published on May 06, 2026

How Bank Audit Systems Track Every Transaction Step

Discover how bank audit systems track every transaction step using audit trails, real-time logging, and AI monitoring to ensure transparency, fraud detection, and regulatory compliance.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on May 06, 2026

Technical Architecture of Secure Online Banking Systems

Explore the technical architecture of secure online banking systems, including layered security, encryption, authentication, APIs, and fraud detection that protect digital transactions.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

How Banks Verify Account Holder Identity Before Transfer

Learn how banks verify account holder identity before transfers using KYC, OTP, biometrics, and real-time fraud detection to ensure secure and compliant digital transactions.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

What Causes Silent Bank Transaction Failures Without Alert

Discover the key causes of silent bank transaction failures, including network timeouts, API issues, system delays, and how banks resolve these hidden payment errors.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

Real Time Bank Transaction Authentication Process Explained

Understand how real-time bank transaction authentication works using OTP, biometrics, encryption, and AI-driven fraud detection to secure digital payments instantly.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ