Why IFSC Code Is Mandatory For Secure Digital Payments

Discover why the IFSC code is essential for NEFT, RTGS, and IMPS. Learn how it prevents fraud, ensures routing accuracy, and acts as a digital fingerprint for banks.

Priya Nair

Senior Compliance Editor at IFSC.co

10 min read

Table of Contents

Have you ever paused to consider the silent guardians that ensure your digital money transfers land precisely where they’re intended? I recall a time, years ago, when a friend nearly lost a significant sum due to a simple digit error in an account number. It was a stark reminder of the complexities inherent in moving money digitally. This experience, among many others, solidified my understanding of why the IFSC code is mandatory in digital payment systems. It’s not just a random string of characters; it’s a critical piece of the financial puzzle, a unique identifier that acts as a digital fingerprint for every bank branch in India. Without it, the vast network of interbank transactions would descend into chaos, making secure and accurate transfers virtually impossible in our increasingly digital world.

The Core Problem: Identifying Banks Uniquely

Imagine a scenario where millions of transactions flow through a vast network of banks and their branches every single day. How do these systems ensure that funds from, say, your State Bank of India account in Mumbai reach a specific HDFC Bank account in Bangalore? Relying solely on account numbers isn’t enough; account numbers are unique within a bank, but not necessarily across the entire banking ecosystem. This fundamental challenge of precise bank and branch identification across diverse financial institutions is precisely what the IFSC code was designed to solve. It provides an unambiguous address, much like a postal code for financial transactions, guiding your money to the correct destination bank and branch.

Before the widespread adoption of IFSC codes, interbank transfers were a much more cumbersome and error-prone process. The sheer volume of transactions processed daily, especially with the rise of instant payment systems, demands an infallible method of identification. Without a standardized, globally unique identifier for each branch, the potential for misrouted funds, delays, and fraudulent activities would skyrocket. The IFSC code streamlines this by offering a consistent format that both humans and automated systems can easily interpret, making it an indispensable component for maintaining the integrity and efficiency of India’s robust digital payment infrastructure.

How IFSC Codes Work: A Deep Dive

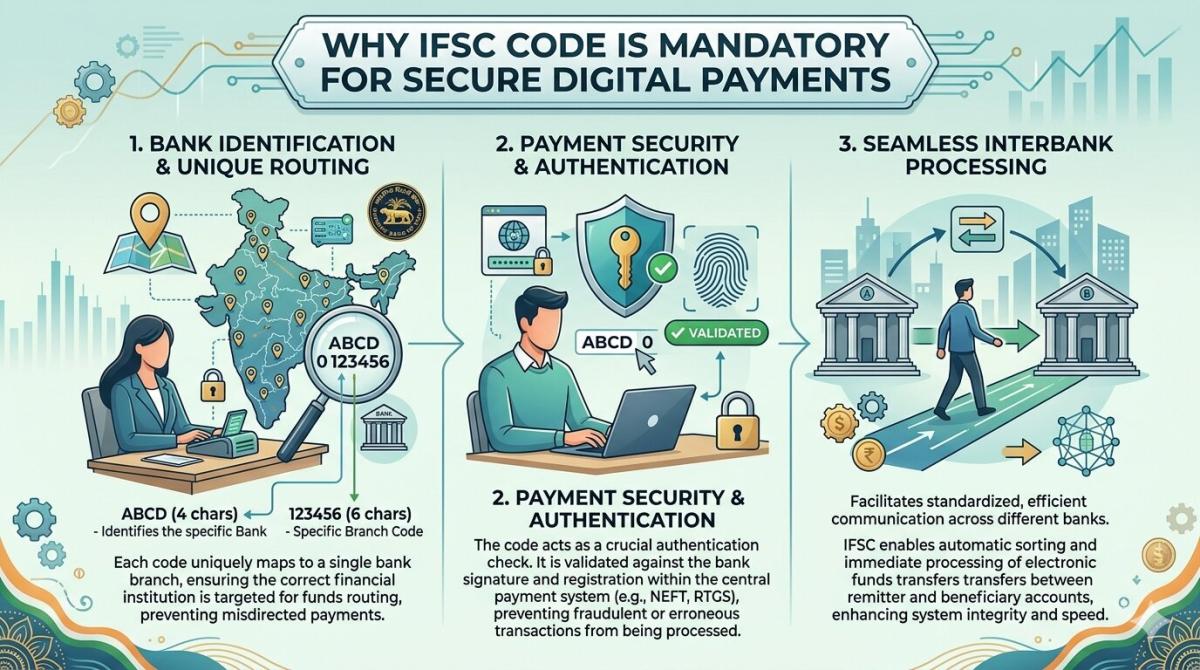

The Indian Financial System Code (IFSC) is an 11-character alphanumeric code, a carefully structured identifier that reveals crucial information about the recipient’s bank branch. The first four characters always represent the bank name, such as “SBIN” for State Bank of India or “HDFC” for HDFC Bank. The fifth character is always zero, reserved for future use, acting as a control character to maintain system integrity. The final six characters are unique to the specific bank branch. This systematic breakdown ensures that every single branch across the country has its own distinct digital address, leaving no room for ambiguity.

Understanding this structure is key to appreciating its utility. When you initiate a digital payment, whether through NEFT, RTGS, or IMPS, your bank’s system uses the provided IFSC code to route the transaction to the correct recipient bank and branch. It acts as a routing number, directing the funds through the appropriate channels within the vast banking network. This granular level of identification is what makes real-time gross settlement (RTGS) and immediate payment service (IMPS) possible, enabling near-instantaneous transfers by accurately pinpointing the exact destination from the outset. Without this precise mapping, such speed and accuracy would be unattainable.

Ensuring Transaction Security and Accuracy

In the realm of digital payments, security and accuracy are paramount. The IFSC code plays a pivotal role in safeguarding transactions against errors and potential fraud. By requiring this specific code, the system introduces an additional layer of verification. It ensures that the combination of the account number and the IFSC code points to a legitimate and correct destination. This dual-factor identification for the recipient’s financial institution significantly reduces the chances of funds being mistakenly transferred to the wrong bank or branch, even if there’s a minor typo in the account number itself.

Moreover, the mandatory nature of the IFSC code contributes to a more secure environment by making it harder for malicious actors to exploit vulnerabilities. When banks process transactions, they can cross-reference the provided IFSC code with their internal databases to confirm its validity and association with the given account number. This validation process is a critical checkpoint, enhancing the overall security framework of digital payments. For consumers, it offers peace of mind, knowing that their hard-earned money is being directed with precision and robust checks in place. The entire system benefits from this enforced clarity, especially as transaction volumes continue to soar.

Regulatory Oversight and Compliance

The Reserve Bank of India (RBI) mandates the use of IFSC codes for all electronic fund transfers, underscoring its importance for regulatory oversight and compliance. This requirement isn’t merely a suggestion; it’s a fundamental pillar of India’s financial regulatory framework. The RBI, as the central banking authority, established and maintains the standardized list of IFSC codes, ensuring uniformity and authenticity across all participating banks. This centralized control prevents the creation of arbitrary or duplicate codes, thereby maintaining the integrity of the entire payment ecosystem.

By enforcing the use of IFSC codes, the RBI ensures that every digital transaction can be accurately tracked and monitored. This is crucial for purposes like anti-money laundering (AML) and combating the financing of terrorism (CFT), as it provides a clear audit trail for funds moving between different financial institutions. Banks are legally obligated to use and validate these codes, making them accountable for the accuracy of the information they process. This stringent regulatory environment, with the IFSC code at its heart, fosters trust and stability within the digital payment landscape, protecting both financial institutions and their customers.

Facilitating Interbank Transfers Seamlessly

The true genius of the IFSC code lies in its ability to enable seamless interbank transfers, acting as the backbone for popular payment systems like NEFT (National Electronic Funds Transfer), RTGS (Real-Time Gross Settlement), and IMPS (Immediate Payment Service). Without a standardized way to identify each bank branch, these systems, which process billions of rupees daily, simply wouldn’t function efficiently. When you initiate a NEFT transaction, the IFSC code ensures your money is routed correctly through the central clearing system to the precise destination branch, regardless of where your bank is located relative to the recipient’s. This eliminates geographical barriers entirely.

For RTGS, which handles large-value transactions in real-time, the accuracy provided by the IFSC code is even more critical. There’s no batch processing; each transaction is settled individually and immediately. The system relies on the IFSC to instantly identify and connect with the correct recipient bank for settlement. Similarly, IMPS, offering 24/7 instant transfers, thrives on the precision and speed that the IFSC code guarantees. These innovative payment mechanisms, which have transformed how we manage our finances, would be fraught with errors and delays without the unique and reliable identification that the IFSC code provides. It’s truly an unsung hero of modern banking.

The Future of Digital Payments in 2026

As we look towards 2026 and beyond, the digital payment landscape is poised for even greater innovation and expansion. The underlying infrastructure, including the mandatory use of IFSC codes, will continue to be fundamental to this evolution. With the proliferation of new payment interfaces and technologies, such as advanced UPI features and potentially new blockchain-based systems for interbank settlements, the need for robust, unambiguous bank and branch identification will only intensify. IFSC codes provide a stable anchor in a rapidly changing environment, ensuring that even the most cutting-edge payment solutions remain grounded in accuracy and reliability. Its utility is set to grow, not diminish.

I believe that the IFSC code will remain a cornerstone of India’s financial system, adapting to new challenges and opportunities. While we might see technological advancements that abstract its direct entry from the user interface, its role in the backend will be indispensable. As digital payments become even more ingrained in daily life for everything from micro-payments to large commercial transactions, the IFSC code will continue to facilitate the secure and efficient flow of funds. Its foundational importance ensures that India’s digital economy can scale responsibly, maintaining trust and operational excellence well into 2026 and for decades to come, providing a reliable backbone for financial inclusion and innovation. You can explore more about India’s digital payment ecosystem on the NPCI website.

Key Takeaways

- The IFSC code is an 11-character alphanumeric identifier crucial for uniquely identifying every bank branch in India, ensuring precise routing of digital funds.

- It acts as a mandatory second layer of verification beyond the account number, significantly enhancing transaction security, accuracy, and reducing the risk of misdirected payments.

- The Reserve Bank of India (RBI) mandates its use for all electronic fund transfers (NEFT, RTGS, IMPS), providing regulatory oversight and a clear audit trail for compliance and anti-fraud measures.

- IFSC codes are the backbone of India’s modern digital payment systems, enabling seamless and efficient interbank transfers that are essential for the country’s rapidly growing digital economy.

Frequently Asked Questions

What does IFSC stand for?

IFSC stands for Indian Financial System Code. It is an 11-character alphanumeric code used to uniquely identify all bank branches participating in electronic funds transfer systems in India.

Is the IFSC code unique for every bank?

No, the IFSC code is unique for every bank branch, not just every bank. Different branches of the same bank will have different IFSC codes, ensuring precise identification of the specific location where an account is held.

Can I transfer money without an IFSC code?

For electronic fund transfers like NEFT, RTGS, or IMPS within India, providing the correct IFSC code is mandatory. Some digital wallets or UPI transactions might abstract the direct entry of the IFSC code, but it is still used in the backend for interbank settlements.

Where can I find my bank’s IFSC code?

You can typically find your bank’s IFSC code on your chequebook, bank passbook, or your bank’s official website. Many online banking portals and mobile banking apps also display the IFSC code for your branch. You can also use online IFSC code search tools provided by various financial platforms.

Conclusion

In closing, the IFSC code is far more than just a string of letters and numbers; it’s the bedrock of India’s robust and efficient digital payment ecosystem. Its mandatory nature ensures the precision, security, and speed that we’ve come to expect from modern banking. As digital transactions continue to proliferate and evolve into 2026, the IFSC code will remain an indispensable component, silently safeguarding our financial transfers and fostering confidence in the system. It’s a testament to thoughtful financial infrastructure design, making complex interbank operations feel effortlessly simple for the end-user.

Related Blogs

Published on May 06, 2026

How Bank Audit Systems Track Every Transaction Step

Discover how bank audit systems track every transaction step using audit trails, real-time logging, and AI monitoring to ensure transparency, fraud detection, and regulatory compliance.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on May 06, 2026

Technical Architecture of Secure Online Banking Systems

Explore the technical architecture of secure online banking systems, including layered security, encryption, authentication, APIs, and fraud detection that protect digital transactions.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

How Banks Verify Account Holder Identity Before Transfer

Learn how banks verify account holder identity before transfers using KYC, OTP, biometrics, and real-time fraud detection to ensure secure and compliant digital transactions.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

What Causes Silent Bank Transaction Failures Without Alert

Discover the key causes of silent bank transaction failures, including network timeouts, API issues, system delays, and how banks resolve these hidden payment errors.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

Real Time Bank Transaction Authentication Process Explained

Understand how real-time bank transaction authentication works using OTP, biometrics, encryption, and AI-driven fraud detection to secure digital payments instantly.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ