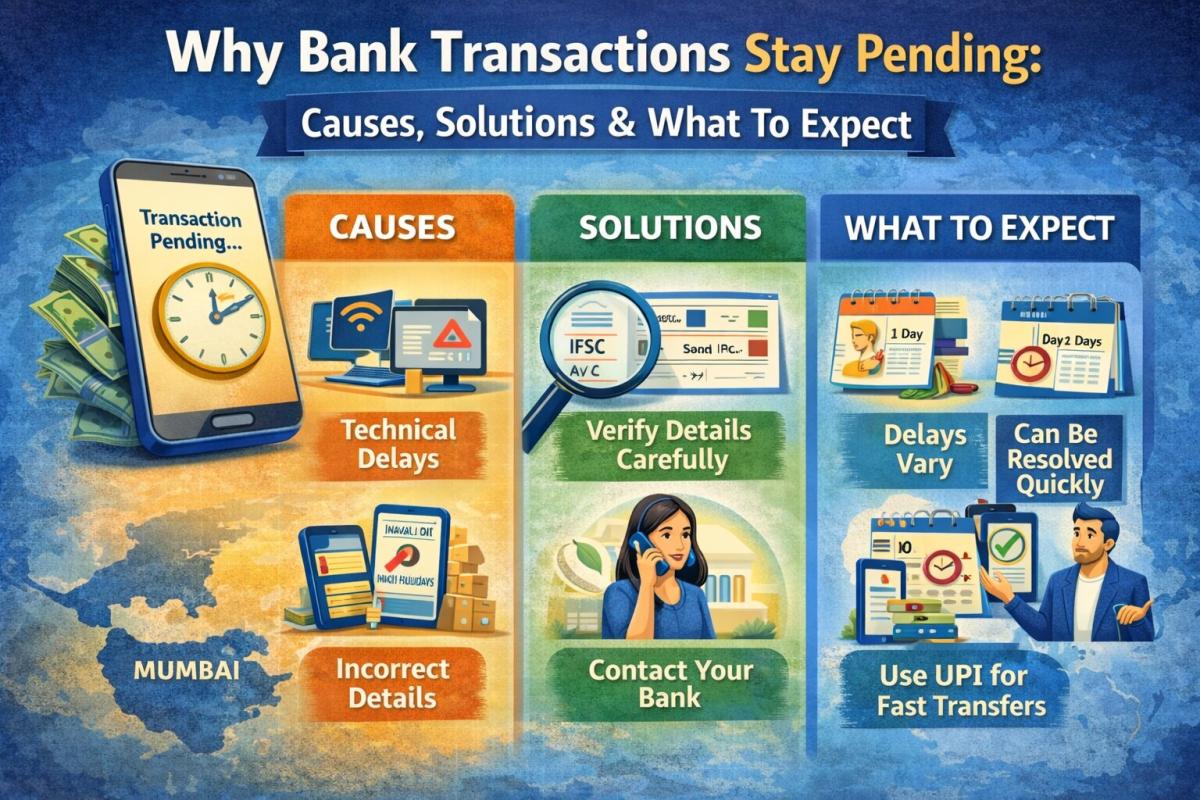

Why Bank Transactions Stay Pending: Causes, Solutions & What To Expect

Frustrated by a "pending" status? Learn the top reasons for transaction delays in 2026, from fraud checks to merchant settlement cycles and international hurdles.

Priya Nair

Senior Compliance Editor at IFSC.co

10 min read

Table of Contents

- Security Protocols and Fraud Prevention

- Enhanced Verification for High-Value Transactions

- Bank Processing Timelines and Cut-Offs

- Merchant Delays and Settlement Cycles

- Insufficient Funds and Authorization Holds

- International Transactions and Regulatory Hurdles

- Key Takeaways

- Frequently Asked Questions

- Conclusion

Imagine the frustration: you’ve just made a crucial payment, maybe for a flight, a new gadget, or even your rent, and you check your banking app only to see that familiar, unsettling phrase: “transaction pending.” It hangs there, a digital limbo, leaving you wondering if your money has truly left your account, when it will arrive, or if something has gone wrong entirely. As someone who’s navigated the labyrinthine world of financial transactions for years, I can tell you that understanding why bank transactions sometimes stay in a pending state isn’t just about curiosity; it’s about financial peace of mind. Let’s peel back the layers of this common banking mystery, because while it often feels like a glitch, it’s usually a perfectly normal, albeit sometimes annoying, part of the process.

Security Protocols and Fraud Prevention

One of the primary reasons transactions find themselves in a pending state is the diligent work of your bank’s security and fraud prevention systems. In an increasingly digital world, financial institutions are under constant threat from sophisticated scams and unauthorized access attempts. When you initiate a transaction, particularly one that deviates from your usual spending patterns – say, a large purchase in a new location, or multiple quick transactions – automated systems flag it for closer inspection. This isn’t an accusation; it’s a protective measure designed to safeguard your funds and identity against potential compromise, ensuring that your money is truly going where you intend it to.

These robust security checks are more crucial than ever in 2026, with artificial intelligence and machine learning algorithms constantly evolving to detect anomalies. Banks employ complex algorithms that analyze hundreds of data points in real-time, from transaction amount and location to merchant type and your historical spending behavior. If a transaction triggers a certain risk threshold, it might be temporarily held pending further verification. While it can be inconvenient to wait, this pause is a testament to the bank’s commitment to preventing financial crime, a necessary evil that protects both you and the broader financial ecosystem from significant losses. Sometimes, a quick call from your bank’s fraud department can swiftly resolve the hold.

Enhanced Verification for High-Value Transactions

Transactions exceeding a certain monetary threshold are almost always subject to enhanced scrutiny, leading directly to a pending status. This isn’t just about preventing fraud; it’s also about compliance with anti-money laundering (AML) regulations and other financial oversight requirements. Banks have a legal obligation to monitor and report large or suspicious transactions to regulatory bodies. For instance, a transfer of tens of thousands of dollars, even to a familiar recipient, will likely enter a pending state as the bank verifies the source of funds and the legitimacy of the transaction, sometimes requiring additional documentation from you. This meticulous approach ensures financial integrity and prevents illicit activities from flowing through the banking system.

Bank Processing Timelines and Cut-Offs

Another significant factor contributing to pending transactions involves the internal processing timelines and daily cut-off times set by financial institutions. While our digital world often gives the illusion of instant transfers, the backend processing of funds still operates on a structured schedule. When you make a transaction late in the day, especially after the bank’s designated cut-off time (which can vary but is often late afternoon), it typically won’t begin processing until the next business day. This can mean a transaction initiated on a Friday evening might not even start its journey until Monday morning, leading to a prolonged pending period.

Furthermore, weekends and public holidays play a substantial role in these delays. Banks, like most businesses, operate on a Monday-to-Friday schedule, and while ATMs and online banking are available 24/7, the actual movement and settlement of funds only occur on business days. If you send money or make a payment on a Saturday, it will likely remain pending until the next available business day for processing. This is particularly noticeable with interbank transfers, where funds need to move between different institutions, each with its own processing cycles. Understanding these fundamental operational realities can help manage expectations and reduce anxiety when you see that pending status.

Merchant Delays and Settlement Cycles

It’s not always your bank causing the hold-up; sometimes, the merchant on the other end is the source of the delay. When you swipe your card or make an online purchase, your bank typically places an authorization hold on the funds. This hold confirms that you have sufficient funds and essentially reserves that money. However, the merchant then needs to officially “settle” the transaction, meaning they send a batch of authorized transactions to their own bank for processing. This settlement process doesn’t always happen instantaneously; many businesses batch their transactions once a day, or even less frequently, particularly smaller establishments.

Until the merchant initiates this settlement and their bank communicates with your bank, your transaction will remain in a pending state. This is a common occurrence, for example, with gas station pre-authorizations or hotel bookings where a larger amount might be held initially, then adjusted to the actual charge upon completion of service. This delay is part of the standard operating procedure for many businesses to manage their finances efficiently, consolidate transactions, and reduce processing fees. It’s a dance between multiple financial players, and sometimes one partner is just a little slower to move.

Insufficient Funds and Authorization Holds

While often overlooked, issues related to your account’s balance or existing authorization holds can directly cause transactions to remain pending. If you attempt a purchase or transfer and your account has insufficient funds to cover the full amount, your bank might initially approve an authorization hold for a smaller sum or keep the transaction pending while attempting to secure the full amount. This is particularly true for debit card transactions where funds are deducted directly. Unlike credit cards that offer a line of credit, debit cards require the funds to be immediately available.

Moreover, sometimes a transaction is pending because there’s an existing authorization hold from a previous purchase that hasn’t fully cleared yet, even if you’ve been charged for it. For instance, if you rented a car, the rental agency might place a significant hold on your card for potential damages. Even if the actual rental fee is smaller, that initial hold reduces your available balance, potentially causing subsequent transactions to pend if they push you over your actual available funds. This can be particularly frustrating in 2026, where instant gratification is the norm, but the underlying financial mechanics still require careful balancing of debits and credits. For a deeper understanding of authorization holds, you might find valuable information on the Consumer Financial Protection Bureau website.

International Transactions and Regulatory Hurdles

When your money crosses borders, the complexity of transaction processing escalates significantly, almost guaranteeing a pending state for a period. International transactions involve multiple banks, different currencies, and a myriad of regulatory frameworks, each designed to prevent illicit financial flows and comply with global standards. Each country has its own banking holidays, processing cut-off times, and compliance requirements, which can add layers of delay. Currency conversion itself is a process that requires verification and can fluctuate, sometimes leading to a hold until the exact exchange rate is settled for the transaction.

Furthermore, international transactions are subject to rigorous anti-money laundering (AML) and counter-terrorist financing (CTF) checks. Banks must verify the identities of both senders and recipients, screen against international sanctions lists, and ensure that the transaction adheres to the financial regulations of all involved countries. This due diligence can take anywhere from a few hours to several business days, especially for large sums or transfers to less common destinations. It’s a critical, albeit time-consuming, process that ensures global financial stability and prevents nefarious actors from exploiting the system. For more details on global financial regulations, the Bank for International Settlements offers extensive resources.

Key Takeaways

- Pending Status is Often Normal: Don’t panic immediately. A pending transaction is a common part of the banking process, indicating that the transaction is in various stages of verification and settlement, not necessarily a problem.

- Security and Fraud Prevention are Key: Banks actively use pending states to protect your accounts from fraud, especially with unusual or high-value transactions. This protective measure is for your benefit, even if it causes a slight delay.

- Timelines Vary by Factor: The duration of a pending state depends on multiple factors including bank processing cut-off times, weekends/holidays, merchant settlement cycles, and the complexities of international transfers.

- Monitor Your Account and Communicate: Keep an eye on your account balance and transaction status. If a transaction remains pending for an unusually long time (beyond a few business days), don’t hesitate to contact your bank or the merchant for clarification.

Frequently Asked Questions

How long do pending transactions usually last?

Most pending transactions, particularly domestic ones, resolve within 1 to 5 business days. However, factors like weekends, holidays, the merchant’s settlement schedule, or international transfers can extend this period. Some pre-authorizations, like those for hotels or rental cars, might linger for up to 10 business days before dropping off or being finalized.

Can I cancel a pending transaction?

Generally, no. Once a transaction is in a pending state, it means the funds have been authorized or reserved, and the process is already in motion. You usually cannot unilaterally cancel it from your end. You would need to contact the merchant directly to request a cancellation, or wait for the transaction to finalize and then initiate a return or dispute process if necessary.

What if my transaction is pending for too long?

If a transaction remains pending for longer than the expected timeframe (e.g., more than 5-7 business days for a domestic purchase, or 10+ for an international one), it’s advisable to first contact the merchant to inquire about their settlement process. If the merchant cannot provide a satisfactory answer, then reach out to your bank’s customer service for assistance and investigation.

Does a pending transaction mean the money is gone from my account?

Not entirely. A pending transaction means the funds have been put on hold or authorized, reducing your available balance. The money hasn’t officially been transferred and settled into the merchant’s account yet. If the transaction eventually fails or is canceled by the merchant, the hold will be released, and the funds will become available in your account again.

Conclusion

Understanding why bank transactions sometimes stay in a pending state transforms a common frustration into a manageable expectation. It’s a complex interplay of security, processing schedules, merchant practices, and regulatory compliance, all designed to safeguard your financial well-being. By recognizing these underlying mechanisms, you can approach your banking with greater confidence and less anxiety. While instant gratification is often desired, the brief pause of a pending transaction is usually just the system working exactly as it should, ensuring accuracy and security in every financial move you make.

Related Blogs

Published on May 06, 2026

How Bank Audit Systems Track Every Transaction Step

Discover how bank audit systems track every transaction step using audit trails, real-time logging, and AI monitoring to ensure transparency, fraud detection, and regulatory compliance.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on May 06, 2026

Technical Architecture of Secure Online Banking Systems

Explore the technical architecture of secure online banking systems, including layered security, encryption, authentication, APIs, and fraud detection that protect digital transactions.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

How Banks Verify Account Holder Identity Before Transfer

Learn how banks verify account holder identity before transfers using KYC, OTP, biometrics, and real-time fraud detection to ensure secure and compliant digital transactions.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

What Causes Silent Bank Transaction Failures Without Alert

Discover the key causes of silent bank transaction failures, including network timeouts, API issues, system delays, and how banks resolve these hidden payment errors.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

Real Time Bank Transaction Authentication Process Explained

Understand how real-time bank transaction authentication works using OTP, biometrics, encryption, and AI-driven fraud detection to secure digital payments instantly.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ