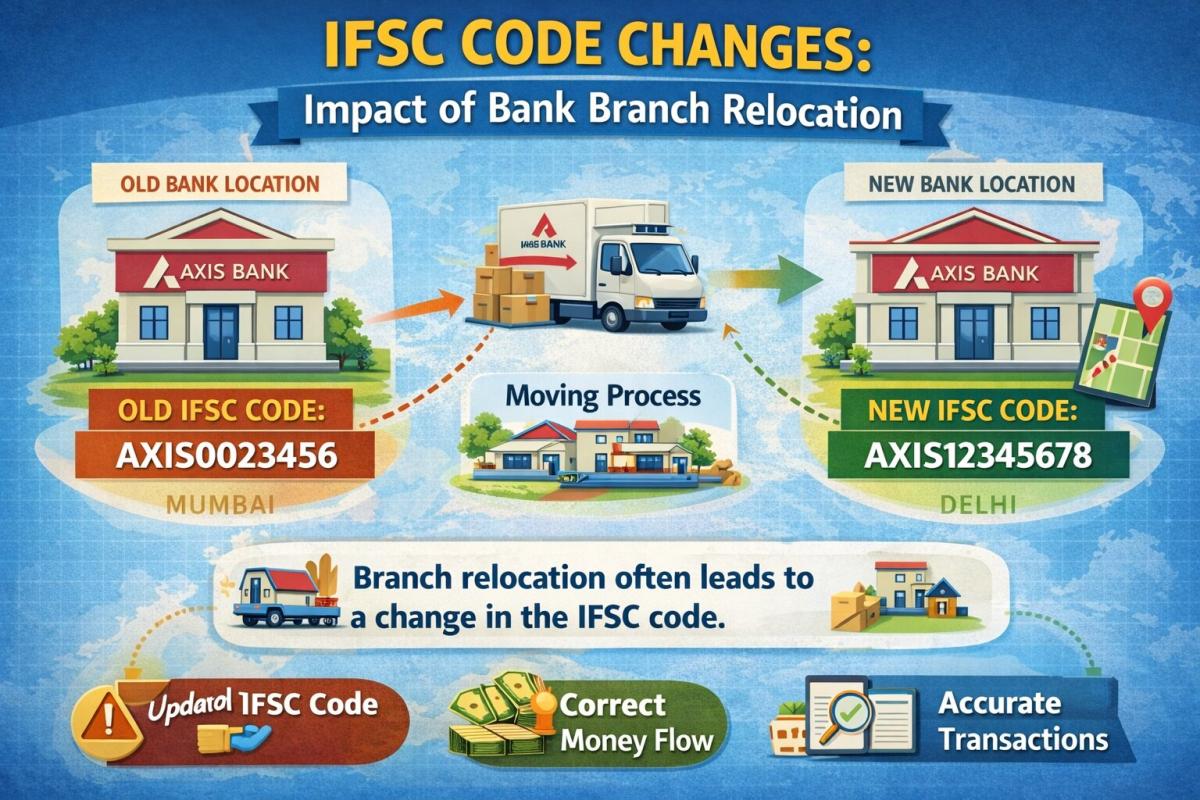

IFSC Code Changes: Impact of Bank Branch Relocation

Does your IFSC code change when your bank branch moves? Discover why relocation impacts your NEFT/IMPS and how to update recurring payments in 2026.

Table of Contents

I remember a frantic call from a friend last year, utterly baffled why a critical payment to a vendor kept failing. After much head-scratching, we discovered their bank branch had quietly relocated, and with it, the all-important IFSC code had changed. This seemingly minor event highlighted a significant, often overlooked issue: the impact of bank branch relocation on IFSC code. It’s a chain reaction that can ripple through personal finances, business operations, and the entire digital payment ecosystem. As someone who’s navigated the complexities of financial systems for over a decade, I can tell you this isn’t just a technicality; it’s a real-world challenge requiring awareness and proactive management. Understanding this dynamic is crucial for seamless financial transactions in an increasingly digital world.

Understanding IFSC Codes and Relocation

The Indian Financial System Code (IFSC) is a unique 11-character alphanumeric code that identifies every bank branch participating in online money transfers like NEFT, RTGS, and IMPS. It comprises the first four characters representing the bank name, the fifth character always a zero for future use, and the last six characters identifying the specific branch. When a bank branch relocates, even if it’s just a few blocks away, its unique identifier, the IFSC, often needs to change. This isn’t a whimsical decision but a necessity driven by regulatory compliance and internal system architecture. Each branch is a distinct entity within the banking network, and its physical address is intrinsically linked to its digital identity.

The decision to change an IFSC upon relocation stems from the need to maintain accurate and unambiguous routing information for funds transfer. Imagine a postal service where two different addresses shared the same zip code; chaos would ensue. Similarly, in the financial world, precision is paramount. While some banks might retain the same IFSC for minor, intra-locality shifts, it’s generally prudent to anticipate a change. The Reserve Bank of India (RBI) mandates stringent guidelines for such changes, ensuring the integrity and efficiency of the payment systems. Banks must meticulously update their records and inform customers, though the effectiveness of this communication varies widely.

Operational Hurdles for Banks

For banks, a branch relocation isn’t merely about moving furniture; it’s a massive logistical and technical undertaking, especially concerning the IFSC code. Internally, core banking systems, payment gateways, and reconciliation engines must be updated with the new branch details and the corresponding IFSC. This requires meticulous planning, testing, and execution to avoid service interruptions. Any error in updating these crucial systems can lead to failed transactions, reconciliation nightmares, and significant reputational damage. The sheer volume of internal systems linked to a branch’s IFSC makes this a high-stakes operation for financial institutions.

Beyond technical updates, banks face the challenge of communicating these changes effectively to their vast customer base. This involves updating websites, mobile apps, physical signage, and informing third-party aggregators and bill payment services. The transition period can be particularly tricky, as some customers might continue using the old IFSC while others adopt the new one. Managing this duality requires robust systems and clear communication strategies. Banks often dedicate significant resources to ensure a smooth transition, but the inherent complexity means hiccups are almost inevitable, particularly for larger networks with numerous branches.

The Domino Effect on Recurring Payments

One of the most insidious impacts of an IFSC change, especially for customers, is its domino effect on recurring payments. Many individuals and businesses set up standing instructions, EMI payments, utility bill payments, and salary disbursements using the old IFSC. When the branch relocates and the code changes, these automated payments can silently fail. It’s not always immediately apparent, leading to missed deadlines, late fees, and potential damage to credit scores. The responsibility often falls on the customer to update every single recurring mandate, a task easily overlooked amidst busy schedules. This highlights a critical vulnerability in our increasingly automated financial lives.

Customer Impact: From Annoyance to Disruption

From a customer’s perspective, the impact of bank branch relocation on IFSC code can range from a minor annoyance to a significant financial disruption. The most common immediate effect is the confusion surrounding online transactions. If you’ve saved the old IFSC in your payment apps or beneficiary lists, transfers will simply fail. For individuals, this might mean a delayed bill payment; for businesses, it could mean payroll delays or missed vendor payments, impacting cash flow and relationships. I’ve personally seen businesses grapple with this, needing to re-educate their entire client base on updated bank details.

The inconvenience extends beyond just updating IFSC codes in digital platforms. Customers might need to update their bank details with employers, insurance providers, investment firms, and government agencies for direct deposits or withdrawals. Imagine the hassle of updating dozens of entities just because your bank branch moved down the street. While banks endeavor to inform customers through SMS, email, and in-branch notices, these often get lost in the noise. It’s a classic example where a seemingly small administrative change can create a disproportionately large burden on the end-user, underscoring the need for greater transparency and proactive assistance from banks.

Digital Transactions and System Updates

The digital payment ecosystem relies heavily on the accuracy of IFSC codes. Every NEFT, RTGS, or IMPS transaction routes funds based on this unique identifier. When a branch relocates and its IFSC changes, every system that holds this information – from individual banking apps to large corporate ERPs and payment gateways – must be updated. This isn’t an instantaneous process. There’s often a lag between the bank’s internal update and the propagation of this information across all connected financial platforms. This lag is precisely where transaction failures occur, leading to frustrating “beneficiary not found” errors.

Consider the broader implications for payment aggregators and fintech companies. They maintain vast databases of bank branch details and IFSC codes. A single bank branch relocation can trigger a cascade of updates across their systems. While these entities have sophisticated mechanisms for data synchronization, real-time changes are challenging to manage without glitches. It’s a testament to the robustness of our financial infrastructure that such changes are absorbed with relatively few widespread issues, but the underlying work is immense. By 2026, with an even greater reliance on digital payments, seamless IFSC updates will be more critical than ever.

Mitigating Risks and Best Practices

For individuals and businesses, the best practice is to always verify the IFSC code, especially for significant or recurring transactions. If you hear whispers of your branch relocating, proactively contact your bank for confirmation. Modern banking apps usually provide the correct IFSC code for your branch, which is a reliable source. For businesses, it’s prudent to communicate any changes to clients and vendors well in advance, providing clear instructions on updating bank details. This proactive approach can save considerable time, stress, and potential financial penalties in the long run.

Banks, on their part, should implement robust communication strategies that go beyond generic notifications. Personalized alerts, dedicated helplines for IFSC-related queries, and clear advisories on their websites and apps can significantly ease the customer burden. Furthermore, exploring technical solutions like temporary redirects for old IFSC codes or a grace period where both old and new codes are valid could minimize disruptions. As we move towards 2026, the emphasis should be on leveraging technology not just for relocation but also for seamless, customer-centric transitions, perhaps by integrating IFSC updates directly into recurring payment mandates.

Key Takeaways

- IFSC Codes are Dynamic: A bank branch relocation often, though not always, results in a change to its unique 11-character IFSC code, essential for digital money transfers.

- Widespread Customer Impact: Individuals and businesses must update their bank details with employers, billers, and payment beneficiaries, as old IFSC codes will lead to failed transactions and potential financial penalties.

- Operational Challenges for Banks: Banks face significant logistical and technical hurdles in updating internal systems, payment gateways, and communicating changes effectively to prevent service disruptions and maintain regulatory compliance.

- Proactive Verification is Crucial: Always verify the correct IFSC code for your branch, especially before initiating new payments or if your branch has relocated, to avoid transaction failures and maintain financial continuity.

Frequently Asked Questions

Does an IFSC code always change when a bank branch relocates?

Not always, but very frequently. While minor intra-locality shifts might sometimes retain the same IFSC, it’s generally best to assume a change will occur. The bank will typically issue an official notification if the IFSC is being updated due to relocation.

How can I find the new IFSC code for my relocated bank branch?

The most reliable ways are through your bank’s official website, their mobile banking app, your new cheque book (if issued), or by directly contacting the branch or customer service. Avoid relying on third-party websites without cross-referencing with official bank sources.

What happens if I use the old IFSC code for a transaction after relocation?

Most likely, the transaction will fail. The payment system will be unable to route the funds to the correct branch, resulting in an error message. In some rare cases, if the old code is temporarily mapped, the transaction might go through, but this is not guaranteed and shouldn’t be relied upon.

When does the new IFSC code become effective after a branch relocation?

The effective date for the new IFSC code is usually communicated by the bank well in advance of the relocation. There might be a short transition period where both codes are technically valid, but it’s always safest to use the new code from the stated effective date to prevent any issues.

Conclusion

The impact of bank branch relocation on IFSC code is a nuanced yet critical aspect of modern banking that often goes unnoticed until a transaction fails. It’s a powerful reminder that even in our increasingly digital world, physical infrastructure changes have tangible digital consequences. As customers, staying informed and proactive is our best defense against potential disruptions. For banks, the imperative is clear: robust communication and seamless transition mechanisms are paramount to maintaining customer trust and ensuring the smooth flow of finances in an economy increasingly reliant on instant digital payments. Let’s all strive for greater awareness and preparedness in this evolving financial landscape.

Related Blogs

Published on May 06, 2026

How Bank Audit Systems Track Every Transaction Step

Discover how bank audit systems track every transaction step using audit trails, real-time logging, and AI monitoring to ensure transparency, fraud detection, and regulatory compliance.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on May 06, 2026

Technical Architecture of Secure Online Banking Systems

Explore the technical architecture of secure online banking systems, including layered security, encryption, authentication, APIs, and fraud detection that protect digital transactions.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

How Banks Verify Account Holder Identity Before Transfer

Learn how banks verify account holder identity before transfers using KYC, OTP, biometrics, and real-time fraud detection to ensure secure and compliant digital transactions.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

What Causes Silent Bank Transaction Failures Without Alert

Discover the key causes of silent bank transaction failures, including network timeouts, API issues, system delays, and how banks resolve these hidden payment errors.

Priya Nair

Senior Compliance Editor at IFSC.co

Published on Apr 28, 2026

Real Time Bank Transaction Authentication Process Explained

Understand how real-time bank transaction authentication works using OTP, biometrics, encryption, and AI-driven fraud detection to secure digital payments instantly.

Priya Nair

Senior Compliance Editor at IFSC.co

calculate Financial Calculators

EMI Calculator

FD Calculator

GST Calculator

Lumpsum Calculator

Mutual Fund Returns Calculator

PPF Calculator

RD Calculator

SIP Calculator

SWP Calculator

article Latest Blog Posts

ELSS vs PPF vs NPS: Which Tax-Saving Investment Gives the Best Returns?

Compare ELSS vs PPF vs NPS to find the best tax-saving investment. Understand returns, lock-in periods, and features to choose what suits your goals.

SIP & Investing • 11 MINS READ

How to Start SIP with ₹500 Per Month: Beginner's Guide to Mutual Funds

Learn how to start a SIP with ₹500 per month in mutual funds. Simple beginner’s guide to investing, building wealth, and growing money with small steps.

SIP & Investing • 13 MINS READ

Senior Citizen FD Rates 2026: Which Banks Offer the Highest Interest?

Compare senior citizen FD rates in 2026 and find which banks offer the highest interest. Learn about returns, tenures, and tips to choose the best FD.

FD, PPF & Savings • 12 MINS READ

Sukanya Samriddhi Yojana (SSY): Interest Rate, Rules & Calculator Guide 2026

Learn about Sukanya Samriddhi Yojana (SSY) including eligibility criteria, required documentation, step by step application process, tax benefits explanation and comparison b/w SSY, PPF and FD

FD, PPF & Savings • 11 MINS READ

2 reasons why online banking is important in today’s COVID-19 situation

Discover why online banking became essential during COVID-19. Learn how digital banking ensured safety, convenience, and uninterrupted financial services.

Digital Banking • 4 MINS READ